The European Central Bank (ECB) is likely to announce a quantitative easing (QE) program involving European sovereign bond purchases at its upcoming policy meeting on January 22, 2015. Recall back in September of 2014, in our two-part Weekly Market Commentary “Don’t Fight the ECB?” we highlighted several reasons for favoring U.S. equities and largely avoiding European equities, despite the ECB’s prior stimulus efforts and potential for outright QE. With QE likely forthcoming, we revisit the opportunity in Europe, which we believe may be setting the stage for a head fake.

WHAT WE ARE WATCHING

As we evaluate the opportunity in European equities, here is what we

are watching:

· Economic growth

· Inflation

· Earnings

· Valuations

· Loan growth

· Relative strength

Economic growth gap between the U.S. and Europe is widening. The U.S. economy has been growing faster than Europe in recent years based on real gross domestic product (GDP). Based on the Bloomberg-tracked consensus of economists’ forecasts for the fourth quarter, Eurozone GDP grew 0.9% during 2014, compared with 2.3% for the U.S. We expect that gap may widen in 2015, as our forecast for U.S. GDP growth (discussed in our Outlook 2015: In Transit publication) is at least 3%.* Even with QE, we do not expect growth in Europe to accelerate in the near term, and as a result we expect this growth gap may widen — although the gap in the third quarter of 2014 of more than 4% (5.0% in the U.S. versus 0.6% in the Eurozone) is not expected to be sustained.

*As noted in the Outlook 2015, LPL Financial Research expects GDP to expand at a rate of 3% or higher, which matches the average growth rate of the past 50 years. This is based on contributions from consumer spending, business capital spending, and housing, which are poised to advance at historically average or better growth rates in 2015. Net exports and the government sector should trail behind.

Deflation risk remains high. Sluggish growth and structural challenges (more on that to come) have led to deflation in Europe, which could result in delayed purchases and investment, further slowing the economy. December 2014 annual inflation in the Eurozone was just -0.2%, or 0.8% excluding food and energy (Eurostat data), not anywhere close to the ECB’s 2% target. Meanwhile, inflation expectations have continued to fall. QE could help a bit in this regard, but we do not expect it to be enough to drive a sustained gain in prices, especially when considering the lack of economic growth.

Earnings mirage. Earnings are expected to increase by 25% in Europe, year over year, in the fourth quarter of 2014. But the gain is all due to depressed financial sector earnings a year ago, which are propping up earnings growth for that sector, while revenue growth is nonexistent. Just three Euro Stoxx 600 sectors are expected to grow earnings based on Thomson Reuters estimates, while eight S&P 500 sectors are expected to grow earnings year over year (for an overall expected mid-single-digit gain). Although S&P 500 revenue is only expected to grow about 1% during the fourth quarter of 2014 (despite the 15% expected drop in energy revenue), that looks good compared with the 2.1% revenue drop expected for Europe. We expect slow growth and extremely low inflation to continue to weigh on European earnings, despite the export benefit of the weak euro.

European valuations look cheaper than they are. European stock valuations (excluding the United Kingdom) are lower than those in the United States based on price-to-earnings ratios (PE) [Figure 1], and they have gotten cheaper since we last wrote on the subject. The discount is currently 12% on a trailing PE basis and 17% on a forward basis. Adjusting for sector mix (the S&P 500 is much more growth oriented, which carries higher valuations), these discounts close significantly. For example, technology makes up about 17% of the S&P 500, compared with just 4% of the MSCI Europe Index, while the MSCI Europe has about triple the weight of the S&P 500 in telecoms and utilities (11% versus 4%). Given the economic growth gap and sector mix, we currently do not find the valuation discount to the U.S. particularly attractive.

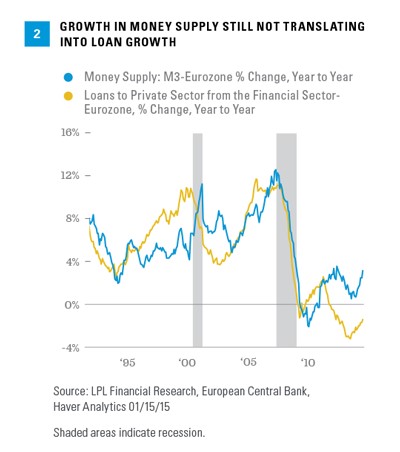

Credit still not flowing. The fractured banking system may mute the effectiveness of QE, because increases in the money supply have not translated into loan growth [Figure 2]. Banks are still undercapitalized and some of the region’s banks still have problems with bad loans, which, when combined with economic uncertainty, is constraining lending. Credit is the fuel for economic growth and European private sector lending — though falling more slowly — is still down 1.1%, year over year, in the latest reported period (November 2014).

Relative strength trend still negative. Since the start of the current bull market in March 2009, European stocks have struggled mightily, relative to the U.S. In 2014, Europe’s loss (based on the MSCI Europe Index) trailed the S&P 500’s 13.7% gain (total return) by more than 19 percentage points, and Europe has slightly underperformed the U.S. so far this year through January 15, 2015 [Figure 3]. From a technical perspective, we have not yet seen enough sustained relative momentum to signal an attractive opportunity relative to the U.S (we should note we are getting closer in emerging markets [EM]).

CONCLUSION

Although we would view a potentially bold QE program from the ECB as an incremental positive, the ongoing growth and deflation challenges in Europe leave us still with a strong preference for the U.S. and a belief that any short-term rally may be short lived. For overseas opportunities, we would first look to EM with a focus on Asia. European valuations have become a bit more attractive and the weak euro may help drive more exports, but we would like to see more fundamental and technical improvement — and get past the risk that the ECB disappoints — before considering a possible Europe trade.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a nondiversified portfolio. Diversification does not ensure against market risk.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Europe Index captures large and mid cap representation across 15 developed markets (DM) countries in Europe.

The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid, and small capitalization companies across 18 countries of the European region.

DEFINITIONS

Eurostat is the statistical office of the European Union situated in Luxembourg. Its task is to provide the European Union with statistics at European level that enable comparisons between countries and regions.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

The money supply is an economic term for the total amount of currency and other liquid assets available in an economy at a point in time. There are several ways to define this number. M1 includes physical money such as coins and currency, checking accounts (demand deposits), and Negotiable Order of Withdrawal (NOW) accounts. M2 includes all of M1, plus time-related deposits, savings deposits, and non-institutional money-market funds. M3 includes all of M2, as well as large time deposits, institutional money-market funds, short-term repurchase agreements and other larger liquid assets. M3 is considered the broadest measure of an economy’s money supply.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-346125 (Exp. 01/16)