Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

Almost a year ago we identified the late cycle symptoms in sector rotations, leading indicators and US treasuries term structure. We briefly review where we stand and conclude that it does not look pretty.

We first identified the late cycle symptoms and analyzed them in details almost a year ago.[1][2] Let us revisit some of the most striking and ongoing developments.

Sector Rotation

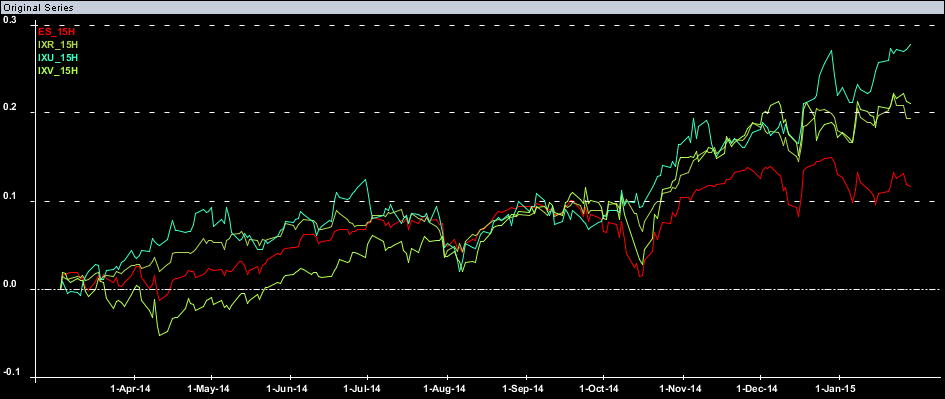

First let us cast a glance at the sector performance since our spring 2014 call. In a typical late cycle transforming into recession environment the best performing sectors are utilities, consumer staples and healthcare.[3]

Indeed this is what we see in the market with healthcare (IXV), consumer staples (IXR) and especially utilities (IXU) drastically outperforming the SPX (ES). Also, two of the three usual underperformance suspects underperformed indeed (consumer discretionary and industrials, but not technology).

Now let us look at the sector rotations. According to our research[4] at the level of sectors US equity market is essentially driven by four factors:

- Market itself (SPX)

- Late/early cycle sector rotation (energy vs discretionary)

- Recession sector rotation (staples+utilities vs technology+industrials)

- Growth/value sector rotation (growth vs value)

Late/early sector rotation factor (long energy and materials, short technology and consumer discretionary) has thrown a strange fit rising this spring (late cycle symptom) and falling since (early cycle symptom). It was driven by oil price of course and more intertwined with global developments. Nonetheless the movements were drastic and clearly directional.

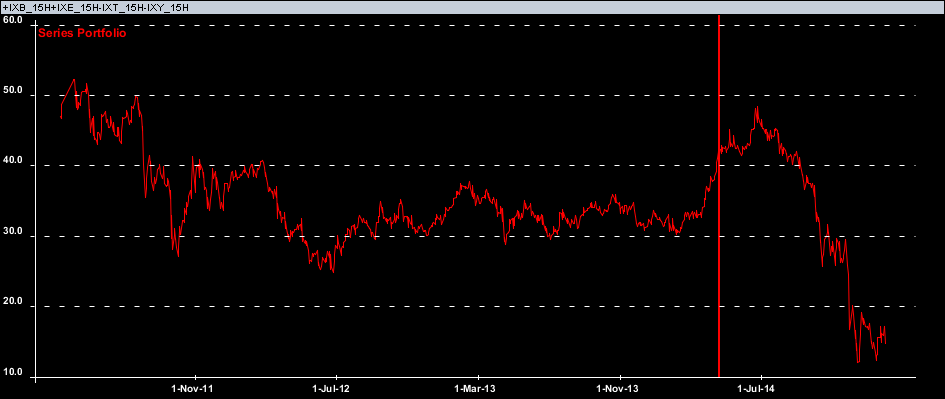

Recession sector rotation factor (long utilities and consumer staples, short technology and industrials) is on the rise (though sporadic) since its bottom in January 2014.

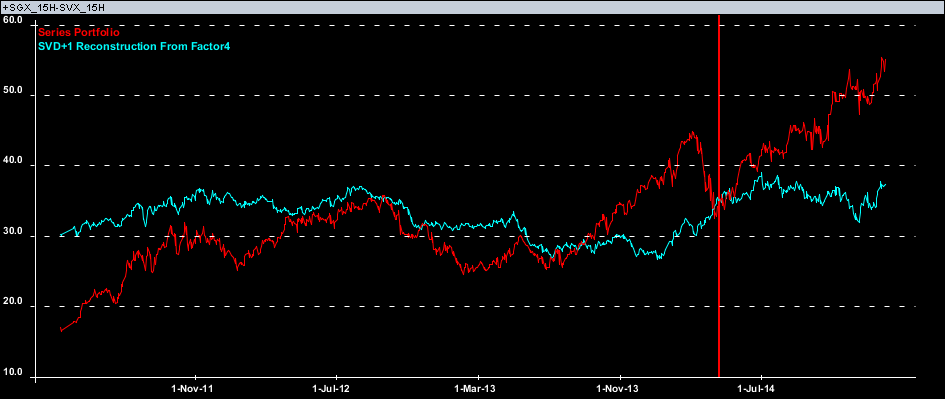

Growth vs Value sector rotation factor (as exemplied by the Citigroup Growth minus Citigroup Value combo) is actually on the rise (red line on the chart below).

But when adjusted for SPX and late/ealy sector rotation factor it turns out to be stagnant since the beginning of the summer (aquamarine line on the chart above).

Yield Curve

We mentioned possible yield curve flattening and level downslide about a year ago.[5] It has been ongoing since then. Here is the level (red) and steepening (green) factor.

Both are sliding since December 2013 as well as cumulative factor for TIPS forward rates shown below

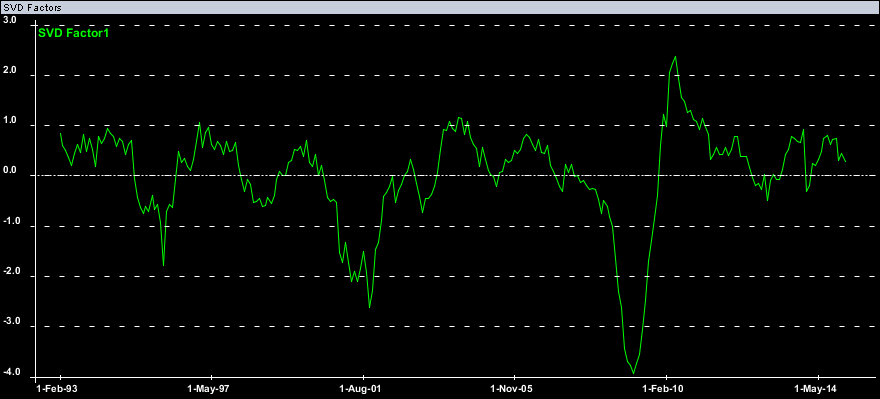

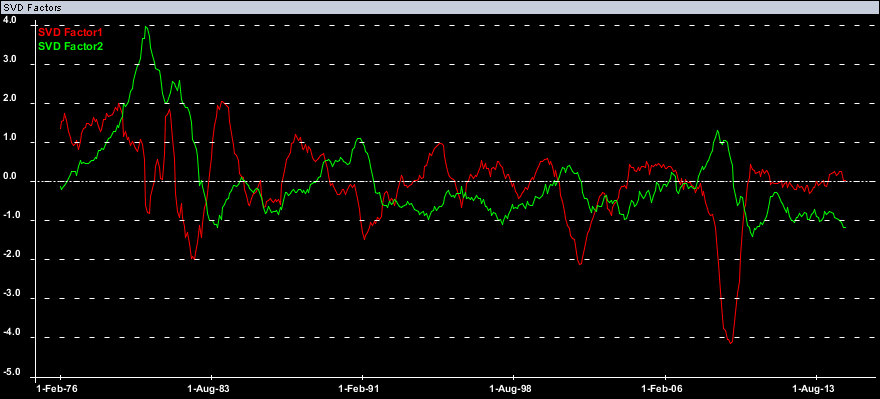

Leading Indicators

We reviewed global leading indicators in great details recently[6] so below we will just briefly review the conventional leading indicator (which we comprise of manufacturers new orders for non-defense capital goods, 4-week moving average of initial claims, PMI new orders, average weekly hours of production and non-supervisory employess in manufacturing).

Conclusion

Here are the overall US growth (red) and inflation (green) factors constructed from the large US dataset. Clearly due to oil the inflation factor is losing bottom.

The conclusion is not obvious though yield curve term structure is telling. Supposedly it all depends now on how serious the FED ongoing commitment to raise short term rates is.

As usually, let us watch the developments carefully and risk manage accordingly.

[1] Dynamika Commentary, “Watch out for the late cycle symptoms”, 30 March 2014

[2] Dynamika Commentary, “Monitoring the late cycle symptoms”, 1 June 2014

[3] Dynamika Commentary, “Where are we in the business cycle?”, 17 November 2013

[4] Dynamika Commentary, “Sector Rotations”, 3 October 2014

[5] Dynamika Commentary, “Where do the leading indicators lead?”, 28 February 2014

[6] Dynamika Commentary, “Unsettling interplay of leading indicators”, 24 December 2014