The Bureau of Labor Statistics (BLS) of the U.S. Department of Labor will release its Employment Situation report for January 2015 on Friday, February 6, 2015. The market is expecting the economy to add 235,000 net new jobs in January 2015, following the 252,000 gain in December 2014, and for the unemployment rate to remain at 5.6%. Average hourly earnings--the best proxy for wages in this report--are expected to accelerate to 1.9% year over year, from the 1.7% year-over-year gain posted in December 2014.

job growth improving, but wage inflation still below “normal”

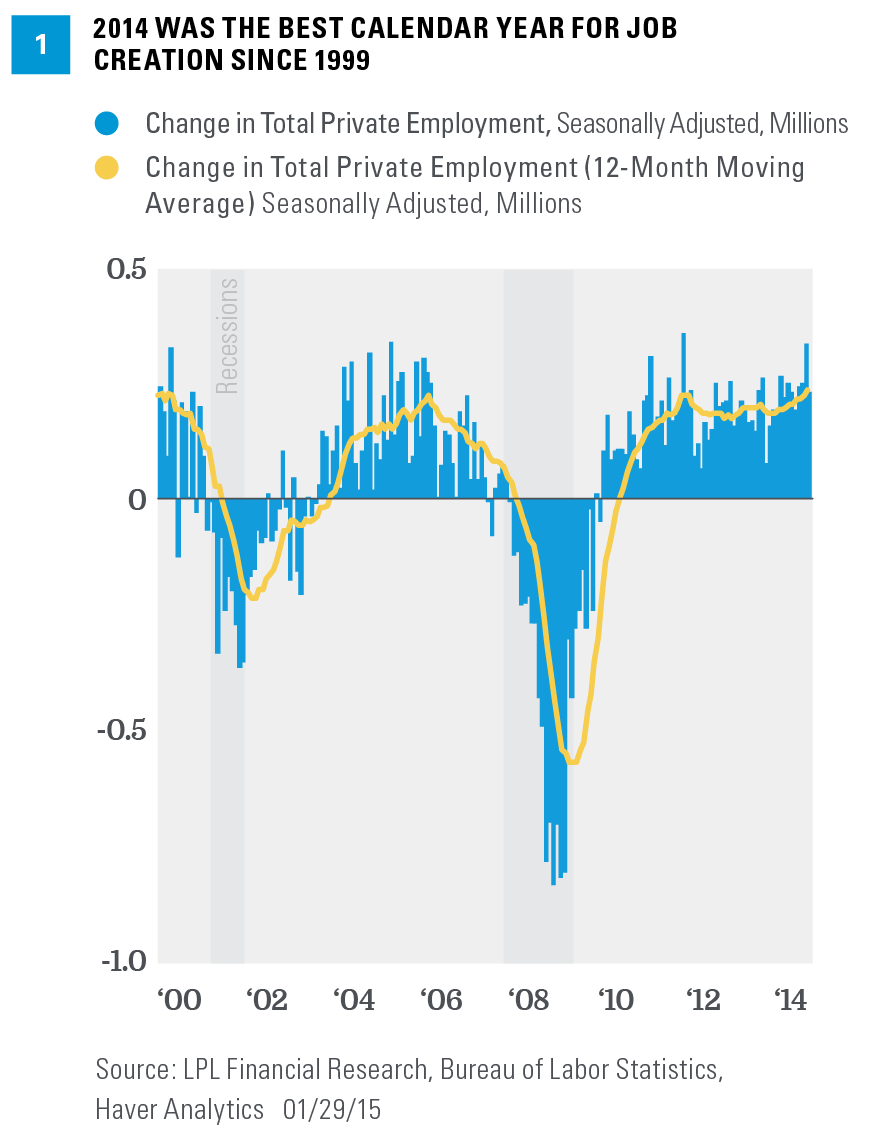

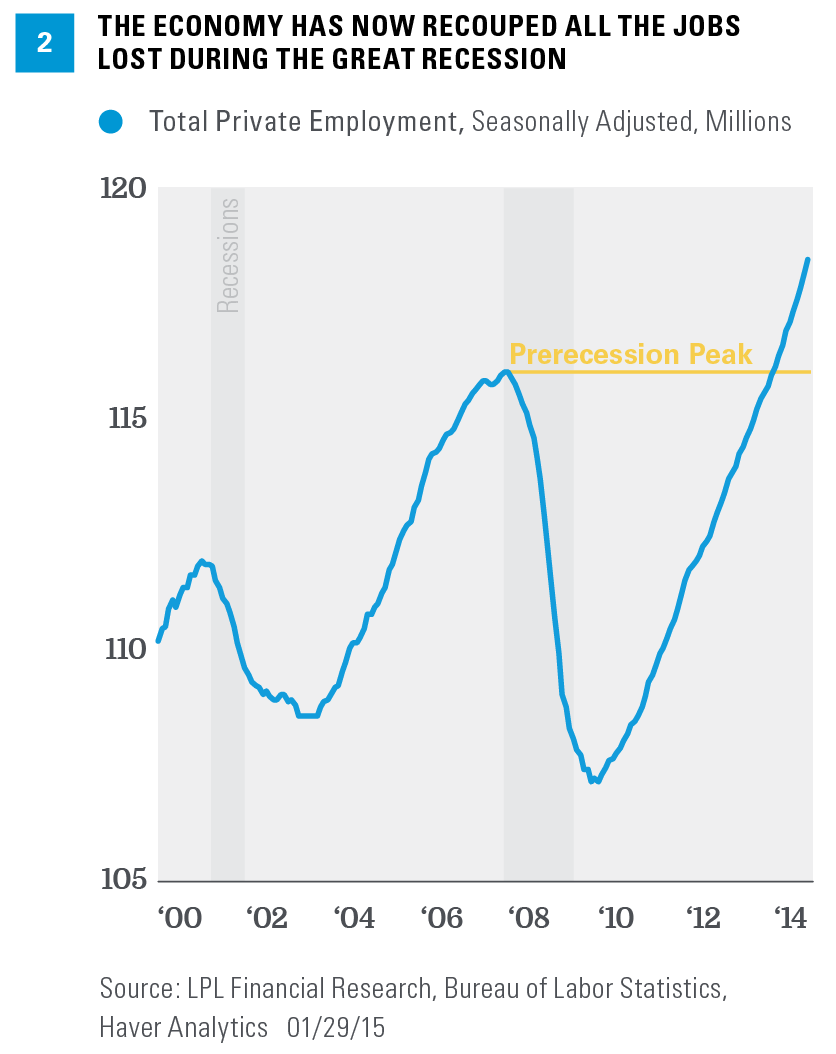

In the 12 months ending in December 2014, the economy created 3 million jobs (246,000 per month) [Figure 1], making it the best calendar year for job creation since 1999. The unemployment rate dropped from 6.7% to 5.6% between December 2013 and December 2014, even as wage growth--measured by the year-over-year gain in average hourly earnings--decelerated from 1.9% in December 2013 to 1.7% in December 2014. Although the economy has now recouped all the jobs lost during the Great Recession [Figure 2], and the pace of job creation over the past year has now surpassed its pre-Great-Recession pace, the unemployment rate is still more than 2 full percentage points above its pre-Great-Recession low, and the pace of wage inflation remains well below the 3.5 - 4.0% seen prior to the onset of the Great Recession. That 3.5 - 4.0% range on wage inflation has been cited by Federal Reserve (Fed) officials as “normal.”

The labor market, and in particular, wages, are among the key factors the Fed considers in deciding when (and by how much) to begin raising interest rates. As we have written in prior commentaries, although the labor market has improved markedly over the past year or so, it still has a long way to go to get back to “normal,” and the Fed may be unlikely to begin raising rates until more labor market indicators are back to normal or on track to get back to normal.

The labor market, and in particular, wages, are among the key factors the Fed considers in deciding when (and by how much) to begin raising interest rates. As we have written in prior commentaries, although the labor market has improved markedly over the past year or so, it still has a long way to go to get back to “normal,” and the Fed may be unlikely to begin raising rates until more labor market indicators are back to normal or on track to get back to normal.

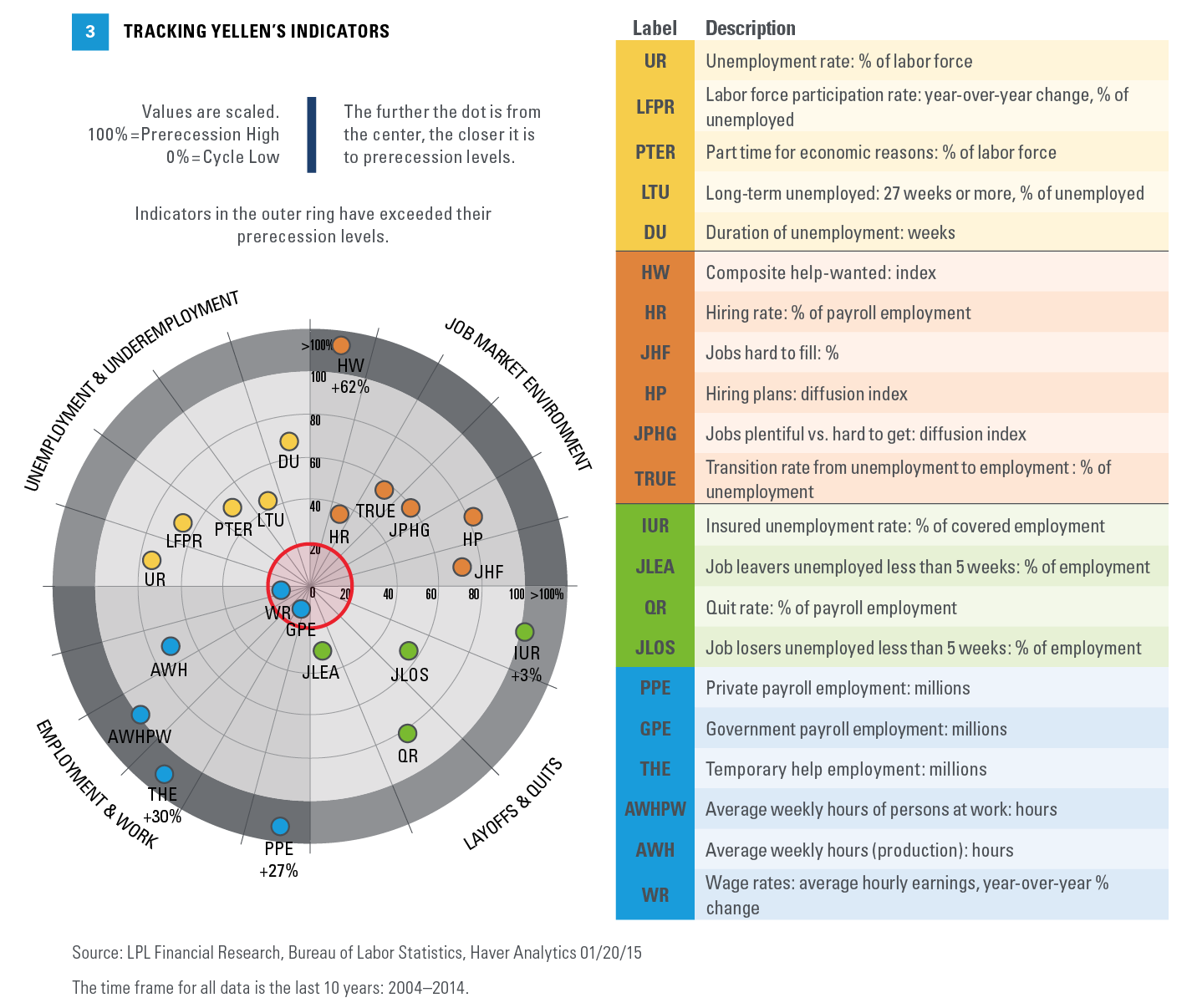

In our Outlook 2015: In Transit, we noted Fed Chair Janet Yellen and the other members of the Federal Open Market Committee (FOMC) are tracking a “broad range” of labor market indicators [Figure 3]. Although market participants and the financial media are likely to focus on the payroll job count, the unemployment rate, and wage inflation in this week’s report, 11 of these so-called “Yellen indicators” will be updated for January 2015, when the BLS releases the January Employment Situation report this Friday, and also bear watching.

oil’s impact on the labor market

While the broad labor market continues to heal, the recent precipitous drop in oil prices has raised concerns about the health of the overall U.S. economy, wages, and in particular, the labor market. (See our Weekly Economic Commentary, “Before and After: Monitoring the Effects of Falling Oil Prices,” December 22, 2014, for more details.) Our view is that although mining jobs (where oil production jobs are counted) have increased more than four times as fast as overall private sector jobs since 2009--and pay 30% more per hour--the size of the mining economy relative to the size of the entire U.S. economy is just not big enough to make a meaningful difference economy-wide. However, in certain states, where the mining economy and mining employment is large enough, the expected drop in mining-related employment and economic output may have an impact. (Please see our Weekly Economic Commentary, “Drilling into the Labor Market,” January 12, 2015, for more details on the impact of the drop in oil prices on the labor market.)

CONCLUSION

We continue to expect the broad economy could potentially create between 225,000 and 250,000 net new jobs per month in 2015, which should further tighten the labor market and push wage inflation higher in the second half of 2015. We also continue to expect the Fed may begin raising rates in late 2015. But other measures of labor market health--hiring rates, the quit rate, the unemployment rate, and most importantly, wages--still show the labor market is not yet back to normal, and argue against the Fed taking aggressive action to raise rates anytime soon.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.