Summary

■ The simplest argument for the oil price decline is for once correct. A wave of new U.S.fracking oil could be seen to be overtaking the modestly growing global oil demand.

■ It became clear that OPEC, mainly Saudi Arabia, must cut back production if the price were to stay around $100 a barrel, which many, including me, believe is necessary to justify continued heavy spending to find traditional oil.

■ The Saudis declined to pull back their production and the oil market entered into glut mode, in which storage is full and production continues above demand.

■ Under glut conditions, oil (and natural gas) is uniquely sensitive to declines toward marginal cost (ignoring sunk costs), which can approach a few dollars a barrel – the cost of just pumping the oil.

■ Oil demand is notoriously insensitive to price in the short term but cumulatively and substantially sensitive as a few years pass.

■ The Saudis are obviously expecting that these low prices will turn off U.S. fracking, and I’m sure they are right. Almost no new drilling programs will be initiated at current prices except by the financially desperate and the irrationally impatient, and in three years over 80% of all production from current wells will be gone!

■ Thus, in a few months (six to nine?) I believe oil supply is likely to drop to a new equilibrium, probably in the $30 to $50 per barrel range.

■ For the following few years, U.S. fracking costs will determine the global oil balance. At each level, as prices rise more, fracking production will gear up. U.S. fracking is unique in oil industry history in the speed with which it can turn on and off.

■ In five to eight years, depending on global GDP growth and how quickly prices recover, U.S. fracking production will start to peak out and the full cost of an incremental barrel of traditional oil will become, once again, the main input into price. This is believed to be about $80 today and rising. In five to eight years it is likely to be $100 to $150 in my opinion.

■ U.S. fracking reserves that are available up to $120 a barrel are probably only equal to about one year of current global demand. This is absolutely not another Saudi Arabia. Saudi Arabia has probably made the wrong decision for two reasons:

First, unintended consequences: a price decline of this magnitude has generated a real increase in global risk. For example, an oil producing country under extreme financial pressure may make some rash move. Oil company bankruptcy might also destabilize the financial world. Perversely, the Saudis particularly value stability.

Second, the Saudis could probably have absorbed all U.S. fracking increases in output (from today’s four million barrels a day to seven or eight) and never have been worse off than producing half of their current production for twice the current price … not a bad deal.

■ Only if U.S. fracking reserves are cheaper to produce and much larger than generally thought would the Saudis be right. It is a possibility, but I believe it is not probable.

■ The arguments that this is a demand-driven bust do not seem to tally with the data, although longer term the lack of cheap oil will be a real threat if we have not pushed ahead with renewables.

■ Most likely though, beyond 10 years electric cars and alternative energy will begin to eat into potential oil demand, threatening longer-term oil prices.

What Is Going On?

It is an unusual and dramatic event when oil halves in price in a few months. Indeed, except for the crash of 2008 it has never happened before since 1900. (It dropped by two-thirds from the end of WWI until the depths of the Depression in 1932 and it dropped 75% after the 1980 peak caused by the Iran-Iraq war and other factors, but in both cases it took several years.) This time, there we were, muddling through quietly, minding our own business, when, Bang!, it happened. Or that is how it felt to most people and most economic commentators. So what was going on? And how unexpected should it have been?

Demand- or Supply-driven Bust?

Oil is recognized as being central to our economy, yet, if anything, its historical role has been underestimated. I argued last quarter that without it our modern economy would not exist and its replacement would be unrecognizably less advanced. Given the complexity of the oil and energy industries, it is probably not surprising that the analyses available for this unique decline differ so widely. The reasons given range from the ingenious to the brutally simple. I usually have a soft spot for ingenious arguments, but for once I believe the simplest case is the right one this time: that it was not unexpectedly weak demand but relentlessly increasing U.S. oil supply that broke the market. There is little that is dramatic about recent GDP growth or oil efficiency. Global GDP growth has been a little disappointing continuously for several years and I believe is likely to continue to be so until official expectations become more realistic. (The official estimates two years ago for trend line U.S. GDP growth were as high as 3%, an extrapolation of earlier growth despite a recent and probably permanent 1% reduction in labor growth. Estimates are now close to 2%, but until they reach 1.5% they are likely to continue to cause mild but steady disappointment in delivered growth in the U.S. and the developed world.) But this disappointment has been slow and steady from the 2009 economic low and many oil experts, I am sure, learned to adjust for it. Increases in the efficiency of oil usage have also been steady but unsurprising. The end result for oil usage in any case was a very boring series of small increases.

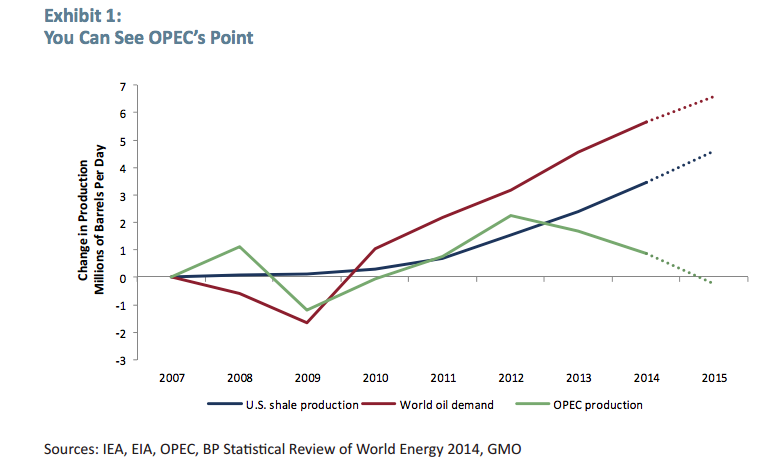

Exhibit 1 shows the change in oil production from the U.S. and OPEC. In great contrast to the picture for oil usage and efficiency, we now see some drama. Such large increases from one source – U.S. fracking, which accounted for over 100% of the U.S. increase, went from about 0% to 4% of global production in only five years – have not been seen since the early glory days in Texas, Pennsylvania, and Baku in the 19th century and in the Middle East in the 1950s and 1960s. Exhibit 1 also shows that in 2013 and 2014 increases in U.S. fracking production equaled 100% of the increase in global oil demand. Worse yet for OPEC, the estimate by June 2014, with the price still around $100, was for U.S. fracking production in 2015 to be even higher than the estimated total increase in global demand this year! More importantly, the increasing surge from U.S. fracking had absolutely not been expected as recently as 2009.

A more complicated argument that this is indeed a demand-driven crisis makes the case that we have had a sudden downgrading of long-term future oil demand. However, this does not seem to relate to recent oil consumption or future GDP forecasts. It has more to do with rationalizing the recent collapse in prices in a demonstration of touching faith in Mr. Market’s foresight: “the oil price has dropped dramatically and, because the market must know what it’s doing, then it must mean that there will be a future collapse in demand.” This is perhaps even more misguided than faith in the stock market’s efficiency. The stock market, as we’ve all discovered at least twice in the last 15 years, is capable of being gloriously inefficient but, compared to most commodities and oil in particular, the stock market is very efficient indeed.

Dire Demand-driven Arguments

Are there other arguments that this was a demand-driven bust? Well, I belong to the group that believes: a) in the extreme importance of oil to our past economic success; and b) that the much higher prices after 2000 were helping to steadily weaken the vitality of the growth in developed countries. But some very smart members of this group argue that so much damage has already been done by higher oil prices (and the underlying cause – depleting supplies of cheap oil resources) that total global consumer demand, squeezed by higher resource prices since 2000, is ready to implode, or indeed may have already started to implode. According to this theory, the growing weakness in global economic strength is what is driving down the price of oil and other commodities: we simply cannot afford the much higher prices of recent years, they argue. My view is that these pessimists (or “realists” if they turn out to be correct) may well be right in the next 10 to 20 years unless we get serious about developing cheap alternatives, as discussed last quarter, and that we should be very worried about this possibility. But, in my opinion, no economic implosion is likely just yet and, even if the pessimists are right eventually, that crunch era will be ushered in by very volatile and rising oil prices, not three years of abnormal stability followed by a sudden bust! Right now the mad rush to produce fracking oil in the U.S. (one might reasonably say “overproduce”) has given us a global timeout from the inevitable oil squeeze, which in my opinion is now likely to arrive in about five years but which, without U.S. fracking, was already upon us. (Please see my last quarter’s letter section, “U.S. Fracking, the Largest Red Herring in the History of Oil,” which argues that in a few years the global oil industry will be as if U.S. fracking had never existed.)

Marginal Pricing and Volatility in Commodities

Mr. Market for commodities is a very wild dude indeed. Prices can move between the marginal cost of providing the cheapest next unit, in a glut, to whatever the most desperate marginal user is willing to pay in a shortage. There is no moral equivalency to that in the stock market. Stock experts may say “greed and fear” (or greed and outright panic), and it’s true that these impulses have impressively influenced the stock market on occasion, but these passions can also apply to commodities, exacerbating their unique sensitivities to imbalances in supply and demand. Commodities can also involve storage of the asset and attempts to corner the market – rather archaic these days in stocks. Most critically, politics, both local and global, can play a much bigger role in commodities, especially oil, than for stocks as we are seeing once again.

The Need for Price Management in Commodities

In a perfectly competitive commodity market, given the sensitivity of price to the change of a few units of demand or supply combined, particularly in earlier times, with the unpredictability of new discoveries, there would be a near permanent hell of huge price moves leading to wasted investments and horribly inefficient long-term plans. Oil and natural gas are particular problems because when all of the vast expense of finding and developing new reserves and writing off dry holes are past and have become sunk costs, the marginal price can fall as low as the cost of turning on the tap for gas or merely paying for the electricity to run the oil pump. That is why people today talk of the possibility of going to $20 a barrel in a sustained glut. Fortunately for all of us, we have lived in a perfectly competitive commodity market for only a few years here and there as a result of accident or incompetence. In the early days, the Rockefellers put together a group (or trust) that controlled 80% of refining capacity and had by dint of its scale the biggest discounts on shipping – seems reasonable in a free market – that often gave it the influence to push the market into being sensible for a while. Later, the Texas Railroad Commission would tell producers what they could produce in the next month, which resulted in mostly reasonably smooth markets until 1972-73, when OPEC took over the job. OPEC, viewed with hindsight, functioned surprisingly well most of the time and unsurprisingly badly some of the time when stresses became too much to handle.

The Stress on OPEC and the Saudis

This time the stress came not from obstreperous OPEC members but from the U.S. fracking cowboys, each attempting to produce as fast as utterly possible even if they had to borrow more than their cash flow to do so. This was an avenue previously closed to most OPEC and non-OPEC producers alike, engineered in the U.S. by a Fed-manipulated era of low interest rates and, for frackers anyway, available debt. Faced with the reality of the rapid rise of U.S. fracking production and the declining share for OPEC, and confronted with the possibility that at over $100 a barrel the U.S. increases might continue at around an incremental one million barrels a day for another two or even three years, OPEC, especially the Saudis, had to do some unusual calculations. The trade-offs they faced had never arisen before. This is the first time that fracking has played a major role in global production, and fracking, particularly in the U.S., has a feature totally unlike other oil: its production can be turned on and off far more rapidly than conventional oil. It is easy to understand the Saudi’s reluctance to cede market share to the U.S. frackers for several years into the future, perhaps down to half of their usual production. They may believe that: a) lower prices can be maintained for a long time, if not forever; and b) that at such lower prices much of U.S. fracking oil will never be produced.

The Current Bust

A sudden drop in oil price because of extensive overproduction has not occurred in recent decades because OPEC operated a reasonably effective cartel, and was often in control of a big enough fraction of supply on the margin. The Saudis also made effective unofficial leaders because they were always conservative and usually sensible and because they had the largest production, the most spare capacity, and the most discipline. The pre-conditions for a sudden oil surplus today required that: a) OPEC would step away from attempting to control the price, especially Saudi Arabia; and b) that a new sustained and unexpected source of major oil supply would come on line. Obviously, U.S. fracking supply meets the second requirement. In the past, a major increment from a non-OPEC source – and one million barrels a day in a market that has recently changed by only one million or so barrels a year – would cause a little cat fighting in OPEC but in one or two years it would be dealt with, or absorbed. What was extra painful for OPEC this time was the relentless pressure each year from increased production of fracking oil building up, in a world with slowing GDP growth, to over 4% of total supply, with no end in sight! Nothing of this persistence and scale of increase had happened since the good old days of major Middle Eastern giant fields back in the distant past of the 1940s and 1950s. The Saudis could this time have backed off their production as they had done several times in the past, or, better for them, persuaded some other OPEC members to share in the reduction. In that event the oil price would have stayed at $100 or so. And what would have been the consequences of sustained $100 a barrel oil? This year, 2015, would have produced another incremental one million barrels a day from U.S. fracking; next year, 2016, probably would have done so again and possibly 2017 as well (i.e., for each of the next three years). “Ouch!” you can hear a Saudi prince say. In the longer run it is probably not the optimal decision for them to force a showdown by refusing to reduce production but it is an understandable decision.

Where Were We Analysts?

I believe the reason for the glut is not complicated: an unprecedented and largely unexpected series of increases in U.S. fracking production combined with a refusal on the part of OPEC to cut back. The alternative reasons that are given are, in my opinion, over-engineered. The problem I have is in understanding why this oil glut came as such a shock. The month-to-month gains in output from fracking could be studied. Yearly productivity increases per well were substantial – over five years, output from new wells in their first year more than doubled in the Bakken – but productivity moved up pretty smoothly month-to-month. The number of rigs being used could be followed. The steady increases after mid 2012 were thus in a sense unremarkable, just a continuation of trends in play.

Both the rig count and the increase in productivity rose steadily so that the year-over-year increases remained quite smooth for over two years. If kept up, such large and steady increases would have to break the market price, ex some offsetting reductions, and the rising oil in storage could be measured showing the increasing pressure on the system. Demand was also reasonably predictable, coming in steadily a little less than earlier expected, but not much less. Clearly, though, global oil demand was not growing fast enough to absorb the new U.S. fracking increases indefinitely. We were rapidly approaching a binary choice: either OPEC, particularly Saudi Arabia, would decide to lower its production or the oil price would break. Only those utterly confident in the Saudi’s willingness to cut should not have been nervous about the price, and it is hard to say where such certainty would have come from. The correct strategy for investors in such a situation would probably have been to buy put options. Then if the probability of a major break (over 10%) was more than 1 in 15 you would have made money. My motto in investing is always cry over spilt milk, for analyzing errors is how you learn almost everything. And, yes, my major regret for 2014 is, “How on earth did I miss this!” A combination of laziness and distraction is my lame excuse. What is yours?

Looking Ahead

The unique features of U.S. fracking

So what happens now? We originally heard a brave story of how increased fracking production would cheerfully continue full steam ahead, even at prices below $40 a barrel. This is of course nonsense: it was not clear that the U.S. frackers were making very good money collectively at $100 a barrel. Now, at $32,1 their cash flow drops by $68 a barrel (less taxes, etc.) and we are meant to believe that they are merely winded. Rigs are being rapidly withdrawn as I write. What is not realized yet, although very shortly will be, is how rapidly fracking wells deplete. Even some of the recent impressive improvements in “productivity” have been moving more of the total output into the first year. Up to 65% of all of the available oil is now often delivered in the first year! Even in the heyday last July, 75% to 80% of all new production in the Bakken was needed to offset the decline from existing “legacy” wells. It could be worked out that daily production would start to decline with only a 25% reduction in oil rigs at work, a level we are rapidly approaching. Thus, at current or lower prices, Bakken production should turn down by June and possibly by the end of the first quarter.2 Meanwhile, back at the head office, several of the “majors” are also savaging their capex budgets for regular oil development. Unlike fracking, which takes days to adjust, old-fashioned oil, which is increasingly deep offshore or in countries that we can all agree are more difficult to operate in than, say, North Dakota, can take 5 to 10 years (and occasionally 15) before a planning dollar becomes gas in the tank. Spending cuts, therefore, will echo into the quite distant future as reduced oil production for which there will be no quick fix, for by then any increases from fracking will be distant memories. And this is a key point: U.S. fracking is the only important component of global supply that can turn up almost immediately by bringing in new rigs and drilling wells in under two weeks, adding 20-30% to production in a year as it did for each of the last two years. It is also the only important component that can turn off quickly by depleting almost completely in three years. As with Alice’s Red Queen, if you pause for breath in fracking you go backwards: more wells must be drilled all the time to even stay still as the wall of rapidly depleting wells builds up behind you. Nothing remotely like this has ever been experienced before so drawing wrong conclusions, as if the traditional data applied, is particularly easy.

The New Oil Balance

Lower oil prices and much reduced capex will guarantee that oil from fracking will start decreasing this year and that the supply of traditional oil will be less than it would have been. Indeed, at recent prices very few, if any, new drilling programs will be started, and a mere three years later at current prices, 80% or so of Bakken production would be history. But right now we have a substantial excess of production, and oil demand is notoriously inelastic to price in the short term – people will not be leaping into their cars to celebrate lower gas prices. But with time they may drive an extra 1-2% percent here and elsewhere and the excess will slowly clear: possibly by mid-year and almost certainly by the end of next year. After supply and demand come into balance, the price initially is likely to rise slowly, held in check by the increasing amounts of U.S. fracking oil that can be profitably produced at each new higher price level. It is this rapid response rate that will make the frackers the key marginal suppliers. This is a sensitive and, I believe, unknowable equation as to precise timing, but this phase will likely end only when fracking production, even at much higher prices, tops out, as it most likely will in the next five years. After that, I believe the equation will revert to the relatively more stable and more knowable one of the 2011 to 2013 era, in which the price of oil will be the full cost of finding and developing incremental traditional oil, which by then is likely to be over $100 a barrel. (In the interest of full disclosure I personally have been and will continue to be a moderate buyer of oil futures six to eight years out, for reasons that should be clear from the above. It should also be clear that such a bet can lose easily enough.)

Probability of a Net Drag on GDP

It is important to remember (as mentioned last quarter) that the global economy benefits dependably only when the real costs of finding oil go down, which is absolutely not happening now. When the costs of finding oil are in a rising trend, then falling prices merely transfer income from the sellers to the buyers. Like all income transfers, there can be a short-term benefit if the buyers have a higher propensity to spend. (An income transfer from the very wealthy to the poor is a much more dependable plus in this respect!) The problem here is that oil companies are receiving such a painful setback that they are cutting back on current spending immediately as well as reducing future spending plans and, because everyone knows about these announced cuts, it hurts the confidence of those affected. The typical recipient, in contrast, may or may not change the way in which he spends his, say, $100 a month, savings from cheaper oil. In addition, some developing countries are quite sensibly taking this opportunity to lower oil subsidies to the general public, which will further dampen the response. There is a completely separate drag on GDP from the oil price drop that has not been widely discussed: deficient GDP accounting. The many comments that predict a substantial net stimulus effect have, not surprisingly, focused on economic reality, in which stimulus and drag seem reasonably equal. But GDP does not measure reality: it measures gross expenses, and the new total value of oil (and natural gas) production has just dropped by an amount equal to a remarkable 3% of GDP! The offsetting beneficiaries, like airlines, will not raise their prices equivalently, but will reluctantly reduce them. On a deficient accounting basis, therefore, there is a substantial drag on stated GDP. So, be prepared.

Why the Saudi’s Decision May Be Wrong

To move back to Saudi Arabia’s decision not to cut back, one thing they may have overlooked, as most of us investors do, is unintended consequences. It is important to recognize in this case that the short-term benefits are spread widely and thinly, but the negatives are concentrated painfully and thus may destabilize the system. The economic pain from the lower oil price on Venezuela, Iran, Nigeria, Libya, Russia, or the Gulf States might set off regional political disturbances or provoke some rash action. Their debt problems combined with those of overleveraged oil sector companies might set off global financial problems. Major shocks like this to the status quo are just plain dangerous, and Saudi Arabia, which loves stability much more than most, may come to regret not having sucked up the pain of selling less for a few years. Cutting back up to half the Saudi oil would have certainly cleared the market for several years and very probably until U.S. fracking supplies peak. Even at its worst for the Saudis, in four or five years isn’t selling half the oil at twice the price a real bargain? All of the fracking oil that can be produced for under $100 a barrel will almost certainly be produced eventually anyway. Current events are very probably merely postponing the production for a while. And the same goes for the bankruptcy of some U.S. oil companies, whose properties will just be taken over by stronger players. Neither of these events appears to be of any longer-term benefit to Saudi Arabia or OPEC in general. Would it not have been better for the Saudis (and OPEC) to let the U.S. fracking industry unload its easy production as fast as possible, peak out in three to six years, and then leave the Saudis firmly in the saddle as the marginal producer once again? If I were on the Saudi long-term planning committee that would definitely have been my vote anyway, especially with the recent passing of King Abdullah, whose successor might not be as careful, generally successful, or as lucky as his predecessor.

Caveat Lector

My analysis is based mostly on official data. The Saudis, however, may believe that U.S. fracking production will be substantially longer-lived and have a higher peak production of, say, 9 or 10 million barrels a day in seven or eight years. At such levels the Saudis would realize that they could not absorb it all. If such a view turned out to be correct, then the Saudis have probably made the right decision. Holding back their production for so long would also have run a high risk beyond eight years that electric cars will have begun to really change the game. The good news is that most of these details will be revealed in time. I can’t wait. In the meantime, I think the odds are with me.

P.S.

Daniel Yergin covers much of this material in a January 23, 2015 New York Times article entitled “Who Will Rule the Oil Market?” He expects that there will be more fracking oil at low prices than most. Interestingly, he provides a perspective that justifies the Saudi’s action facilitating global overproduction while pointing out that “it was assumed that OPEC would step in and cut production.” His argument suggests, at least, that this assumption should have been qualified as probable but far from certain. (Disagreeing with experts should not be intimidating if we remind ourselves how many expert bankers nailed the financial crash!)

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending February 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

1Price per barrel for North Dakota Williston Basin Sweet Crude was $31.94 on January 28, 2015. Plains Marketing, “Crude Oil Price Production,” (2015-018).

2There is one technical complication in the Bakken. The specialist “completion” teams who bring the new wells online have been left behind by last year’s feverish drilling rate and 750 wells are awaiting completion. If completed quickly, they will give an extra kick for a month or two, but why would you “complete” at $32 a barrel when 65% of your total will receive low first-year prices and miss a rebound? That is, unless you absolutely have to. Probably many will wait. We will soon know. It is a wonderfully complicated and interesting business!

© GMO