With a modest schedule of data releases, we can expect more analysis of last week’s news. Trading in several markets changed course rather abruptly. With traders poised to spot any change in trend, the question will be whether this shift is for real.

Is it finally time for “Risk On”?

Prior Theme Recap

In last week’s WTWA I predicted that the deluge of economic data would be closely examined for signs of weakness. Put another way, would the economic releases confirm the story of the markets in commodities and bonds? The question was a good one, and the answer was “no.” Friday’s employment report was the final element, changing the terms of the debate from deflation concerns to that old standby, worrying about the Fed.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

The quirks of the calendar sometimes result in a quiet week following one crammed with data releases. Such is the case in the week ahead, but there is plenty of food for thought. Strength in oil, commodities, and stocks combined with weakness in bonds, utilities and even the dollar. It was the first 2015 sign of a change in market tone. Traders were asking: Is it time for “Risk On?”

Background

Over the last two months I have carefully raised and explored the “message” from various markets.

- Oil Prices (12/13/14)

- The bond market (1/11/15)

- Earnings (1/18/15)

- Europe (1/25/15)

These themes all gave due respect to the approach of seeking a “message from the market.” This is a favorite for most traders and pundits, but it often serves to explain the past. Few seem to find predictive edge from this approach, although it sounds good on TV.

The alternative is to use economic data and corporate earnings to discover where markets may not be efficient. This helps to identify sectors and stocks that are mispriced. Last week I suggested that it might be time to start with the economic data rather than market prices. This advice echoed my 2015 Annual Preview.

The Viewpoints

Here are the main contenders:

- Trader perspective – markets lead. Brett Steenbarger started the week with his explanation of weakness in five macro themes. In the old days when he lived in Naperville, we would have a cup of coffee to argue it out. I miss those conversations. By week’s endhe acknowledged that a “savvy trader” had to be alive to changes in market themes.

- Trader perspective – agility. Charles Kirk’s indispensable weekly chart show (small subscription price required, and well worth it) notes that markets held support, “safety” trades could be quickly abandoned, and there was still a search for reasons to sell. Well put!

- Improving economy. Check out the weekly analysis below. Also “Oil Near a Bottom?” And New Deal Democrat. NDD also has his valuable comprehensive summary of factors.

- There is no hope. Some pundits cannot even discuss good news for a few minutes before turning to what this means for the Fed. You know it is politically charged commentary when it says the Fed is “running out of excuses.” A small change in the timing for the very first increase in short-term rates is heralded as a market disaster. This theme finds its way into the mainstream media, even including non-financial sources like the PBS Newshour.

The tone change was apparent in oil, bonds, utilities, and other markets. The trading in TNX is typical. This is a CBOE product that tracks the ten-year yield. Just divide by ten. Pick your own upside target for the first move.

And here is the same story told in utility trading – last year’s big winner and last week’s big loser.

As always, I have some additional ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

Despite the market reaction, there was plenty of good news last week.

- Rail traffic was strong. See Steven Hansen at GEI. Also note Bob Dieli in the quant corner on truck traffic. Skeptics of government data should be paying attention to verification from private sources.

- Weekly jobless claims remained low. The 278K reading confirmed last week’s holiday data. Bespoke has the story and this chart:

- Earnings reports have been positive. It may not seem like it, but 78% of reporting S&P companies have beaten on earnings and 58% on sales. (FactSet). Some readers objected last week that these results reflected success against lowered expectations. Of course. I have frequently written about this phenomenon. The question right now is whether estimates have fallen enough, and apparently they have. Brian Gilmartin has a more upbeat take, emphasizing the results outside of energy. If energy were to stabilize, potential would be even stronger. This is why it is right to take note of results, especially in the energy sector, where the news was pretty good this week.

- Auto sales were strong versus easy comparisons from last winter. A feature was the rebound in the Ford F150 indicator. This has some correlation with small business and construction activity, but has recently been distorted by the model changeover. See Bespoke for the story and charts.

- ISM services registered a slight beat of expectations at 56.7, maintaining former strong levels. (Doug Short).

- Oil prices firmed. The long-term economic effects remain a subject for debate. Meanwhile, the short-term “risk on” correlation remains. James Stafford at Oilprice.com summarizes the economic and geopolitical factors behind this week’s trading.

- Employment strengthened. Net payroll jobs increased as did wages and hours. Labor force participation was stronger. Prior months were revised higher. You had to look hard to find something wrong with this report, mostly factors that were improving less than the headline numbers. The WSJ has a full chart pack. Jon Hilsenrath goes quickly to the possible implications for Fed policy.

The Bad

The bad news included some significant economic reports.

- Ukraine. There were European meetings without apparent progress, addressing the question of whether Ukraine supporters should provide more deadly weapons (as requested). A peaceful resolution and the winding down of sanctions would be a major plus for the world economy and also for equity markets. Since the negative impact has built up gradually, it is much greater than most realize. To be fully informed, you could start with the interesting Brookings debate.

- The ISM index declined to 53.5 from 55.1, missing expectations. Some key internal factors also looked weak. Steven Hansen at GEIhas a full account. I like his analysis since it includes detail on the component breakdown. As he notes, this is still expansion territory. The official ISM commentary has several references to the West Coast port issues and also notes that the data imply a GDP increase of 3.3%.

- Greece. No real progress and signs of intransigence. Philip Atticus has a stern criticism of the Greek position. Stephen Fidler explores the possible policy links to Russia.

The Ugly

Measles? Libya again? Medical records hacking? Discussion welcome!

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are welcome. I am seeing plenty of bad charts, but little refutation.

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.” This week’s report covers a range of important issues beyond the headlines, including interesting sections on part-time employment as well as important sectors. An example of important information you do not see elsewhere is the analysis of job growth in trucking, “…if there is nothing to put in the trailer, you don’t put anyone in the tractor.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s Big Four summary of key indicators.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. Georg continues to develop new tools for market analysis and timing. Some investors will be interested in his recommendations for dynamic asset allocation of Vanguard funds and TIAA-CREF asset allocation. He has added a method for Vanguard Dividend Growth Funds. I am following his results and methods with great interest. You should, too. Georg’s update this week is a relative value bond indicator. Georg asks, “When Will the Panic Buying End“? Read the entire piece for the full interpretation behind this interesting chart:

The Week Ahead

It is a modest week for economic data.

The “A List” includes the following:

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Retail sales (Th). What will happen to the gasoline savings?

- Michigan sentiment (F). Remains important for jobs and spending.

The “B List” includes the following:

- JOLTs report (T). Most still do not understand the significance of this series – labor market slack. This is the factor watched by the Fed, not a backdoor method for estimating overall job creation.

- Wholesale inventories (T). December data, but relevant for Q4 GDP.

- Business inventories (Th). Same as wholesale data.

- Crude oil inventories (W). Maintains recent interest and importance.

There is a little FedSpeak as well as appearances and meetings featuring world leaders. Important corporate earnings continue.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

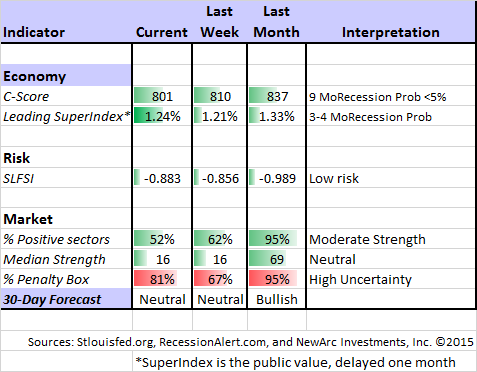

Felix continues a “neutral” posture for the three-week market forecast, but it continues to be a close call. The data have improved a bit, but are still marginally neutral. There is still plenty of uncertainty reflected by the high percentage of sectors in the penalty box. Our current position is still fully invested in three leading sectors, and we have gotten more aggressive. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com.

Brett Steenbarger has typically wise advice for traders – thinking about trading as an entrepreneur would a new business. Great stuff.

A sadder note for many of us is the end of floor trading in many contracts at the Merc. The several Chicago floors at one time had over 10,000 traders. To be successful required a unique blend of spirit, fast thinking, intelligence, athleticism, integrity, and courage. You also had to be impervious to distractions like people spitting on you, poking you with a pencil, or getting in your face. Trades were cleared at the end of the day. If you did not honor a trade, you were soon gone.

Craig Pirrong has a great account of this change, historic but inevitable. Follow his links to some online video documentaries that provide realistic portrayals.

As I have noted for five weeks, Felix continues to feature selected energy holdings. Felix is not just a momentum trader!

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a new page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

My bold and contrarian prediction for 2015 – that the leading sectors would lose and the laggards would win – looked a lot better this week. If I am correct, there is a very, very long way to run for the cheapest market sectors – energy, technology, cyclicals, and financials.

Other Advice

Here is our collection of great investor advice for this week:

Being Contrarian

If you were going to pick one link to read this week, I recommend this Michael Mauboussin piece. It will take a few minutes, but be worth your time. He explains, using some great examples, why it is not enough to be contrarian. You also must have edge! Sometimes (often?) the crowd is right. Markets may be accurately priced. Can you spot the difference? Will you be patient enough to let your system work? (I confess that part of my love for this work is that it is exactly what I and other value managers try to do).

The Quest for Yield

David Merkel does a great takedown of the new eBonds. We see another version of financial alchemy, turning risky assets into something with an AAA rating. Even if you cannot see a flaw, it might simply mean you need to look farther. Risk must be reflected somewhere, and you need to know whether counter parties can pay.

On the positive side in the quest for yield, Charles Sizemore makes the case for REITs. He explains why this should be a diversification for many and an alternative to bond funds.

Or maybe not! Oliver Renick and Brian Louis explain that REITs are over-valued and poised to fall. Expect bond-like, rate-sensitive performance.

Stock and Sector Ideas

Jeffrey Kleintop warns against being “fooled by currency.” Citing Europe and US multinationals, he notes that a “weaker currency is no substitute for a stronger economy.”

Someone is making a big bearish play in the XLU, the Utilities SPDR. The increase in put buying on Friday was 852%.

Consider using Liquid Alts both for hedging and diversification. Rob Martorana is our go-to expert on this topic. I am less worried than he is about the “aging bull” but I consider his recommendations with great interest and respect.

“Secret” hedge fund picks, leaked from a big-name conference. Including short ideas. (CNBC).

Market Outlook

Nouriel Roubini calls out the doom-and-gloomers. Here is a key quote:

One result of this global monetary-policy activism has been a rebellion among pseudo-economists and market hacks in recent years. This assortment of “Austrian” economists, radical monetarists, gold bugs, and bitcoin fanatics has repeatedly warned that such a massive increase in global liquidity would lead to hyperinflation, the U.S. dollar’s collapse, sky-high gold prices, and the eventual demise of fiat currencies at the hands of digital cryptocurrency counterparts.

None of these dire predictions has been borne out by events.

Mark Hulbert says that Dow Theory is now flashing a “sell signal.”

Final Thought

Risk. Many investors wisely begin by thinking about risk. That is how I start each interview with a potential client. Everyone has the need to protect a portion of the investment portfolio, with the assurance that any losses will be modest.

It is not always easy to identify safety. Last year’s most successful investments were bonds and bond proxies. The quest for safe yield has become a crowded trade. Those celebrating the success of bond mutual funds and their utility payouts should look at this week’s results. It is a very small taste of what will happen when interest rates return to more normal levels.

Reward. And we all need some investment reward, either to keep pace with inflation or to increase the retirement nest egg. There is excessive focus on arguments about the overall market valuation. There are plenty of cheap stocks and sectors.

Take only one example. The energy names that I mentioned in the annual preview – refiners and integrated oil companies that actually can benefit from lower oil prices – are all up about 10% in less than a month. (VLO, MPC, CVX).

Regional banks that allegedly have exposure to energy company loans are another happy hunting ground.