We are in a dynamic period of growth in the technology sector driven by the waves of innovation in areas like cloud computing, mobile Internet, the “Internet of Things” and next-generation security.

Dynamic Period of Innovation and Disruption

These are most interesting times to be involved in the technology sector. We are in a dynamic period of innovation and disruption that comes around once a decade and is radically changing how both consumers and businesses utilize technology. Imagine a day now without Facebook, smartphones or Wi-Fi. Over the last several years, numerous technologies have advanced and converged in the areas of computing, mobility, connectivity, digital media and e-commerce to create a more seamless integration of technology and new business models.

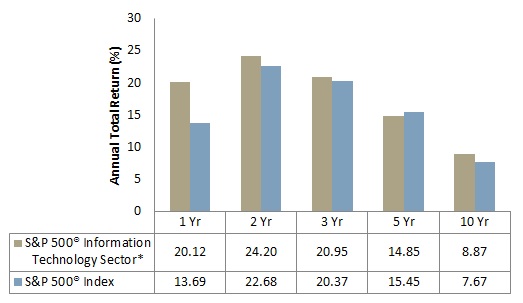

At Rainier, we believe the pace of innovation is accelerating and providing attractive growth opportunities for many technology stocks even in a mixed global macro environment. The technology sector continues to represent one of the larger allocations in each of our investment strategies, as well as in most of the major indices. As Exhibit 1 shows, the technology sector has outperformed the broader market – in most periods – because of this value creation from innovation and faster growth.

Exhibit 1: Benchmark Index vs. Technology Sector Performance

Data as of 12/31/14. Source: FactSet, S&P.

*Based on GICS® sectors. Past performance is not a guarantee of future returns.

While there have been some concerns about “bubble-like” valuations recently, we believe that it is isolated to a small handful of stocks in the public markets and more so in the private markets, which are a bit more inefficient and flush with capital. Corporate balance sheets in the technology sector are also much stronger than in 1999-2000 and many business models are now more proven. At Rainier, we believe the overall technology sector is reasonably priced relative to its earnings growth potential and market opportunity.

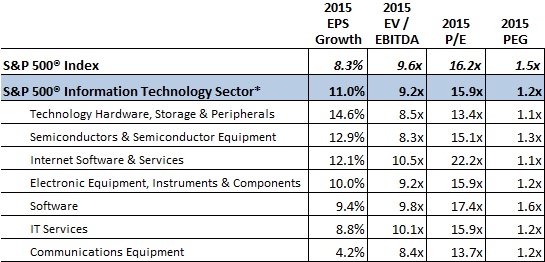

Exhibit 2: Information Technology Sector by Industry

Data as of 12/31/14. Source: FactSet, S&P.

*Based on GICS® sectors. Past performance is not a guarantee of future returns.

EPS Growth is not a measure of future performance.

Based on 2015 consensus estimates, the S&P 500® Index currently trades at a P/E of 16.2x on 8.3% earnings growth, while the S&P 500® Information Technology sector trades at 15.9x on 11.0% earnings growth with a P/E to Growth ratio at a modest 1.2x (See Exhibit 2). Looking a level deeper, only a few subsectors like Internet Software & Services are trading at a premium to the S&P 500. While valuations look expensive for some high-growth stocks in this subsector, the majority of these companies are highly disruptive, attacking new markets, and heavily investing at an early stage of growth. Valuations for growth companies can be volatile at times, but longer-term earnings do eventually reward patient investors, in our experience. As we look into 2015 and beyond, there are several key trends in technology that we believe provide a solid foundation for growth and many compelling investment opportunities across the major industries in technology.

Mainstream Adoption of Cloud Computing

In a few short years, cloud computing has transformed the way IT services are delivered and managed, and is creating a new generation of services and business models that live in the cloud. Cloud computing is the on-demand delivery of IT resources (compute, storage and networking) and applications via the Internet.

The first wave of cloud computing was about moving low risk workloads to the cloud and getting the benefits of lower costs and economies of scale. The next wave is about leveraging real-time data to provide more advanced analytics and intelligence into new applications and services for each vertical industry. Established companies like Microsoft, IBM and Oracle are now embracing this transformative shift, and adapting their business strategies and products for the cloud. We are encouraged by a number of investment opportunities in the cloud computing market, which is well on its way to being a $100 billion-a-year industry over the next decade.

The category of cloud computing is large and may include:

· Software-as-a-Service (SaaS): businesses subscribe to an application or service (example: Salesforce.com, Workday, ServiceNow, NetSuite);

· Platform-as-a-Service (PaaS) and Infrastructure-as-a-Service (IaaS): software developed and deployed on a common cloud platform or on core infrastructure building blocks (example: Amazon Web Services, Google Cloud Platform, Microsoft Azure, Rackspace, IBM SoftLayer, VMware vCloud);

· Online Services: consumer or business services that provide innovative products built on the cloud (example: Netflix, AirBnB, Dropbox, LendingClub).

Mobile Internet in Our Daily Lives

In the last few years, smartphones and tablets have become one of the fastest adopted platforms in history. Over one billion smartphones shipped in 2014 and penetration rates in the U.S. are now over 70%. Tablet shipments reached over 200 million in 2014 and are close to overtaking PCs in a few years. In international markets, smartphone adoption is much lower as the price points of devices are just now getting to the tipping point and as more 3G/4G networks need to be built out.

The majority of people in the U.S. and other developed markets now have the power of a computer in their hands while on the go, and it’s changing our daily lives in how we find products, shop, interact and socialize. Surfing the web has been replaced with mobile apps that deliver a much richer and more interactive experience. You’ve seen how common using Google, Facebook, Yelp, Netflix and now Uber have become. Millions of people now use their mobile apps each day to keep up with friends, find a restaurant or get a ride.

The time spent on mobile devices continues to grow at a faster rate than any other media and is now estimated to be over 2.5 hours per day among U.S. adults. While time spent on TV viewing still leads at over 4 hours per day, we expect this gap to close over time as digital video proliferates and mobile transactions become more seamless. At Rainier, we believe the mobile Internet will continue to offer many investment opportunities in the areas of Internet advertising, digital entertainment, and mobile commerce and payments.

Internet of Things Driving Smarter Decisions

Each day, more objects are being embedded with sensors and wireless connectivity to collect massive amounts of data. This can range from a smartphone, a thermostat in the home, a sensor in a jet engine, to a GPS receiver on a tractor. The interconnected fabric of devices, machines, processes and people communicating is known as the Internet of Things (“IoT”), and represents one of the next biggest waves in technology that could transform every industry and drive outsized productivity gains over the next decade.

This industrialization of the Internet is creating a new information network that can significantly improve business processes, reduce costs and risks, and create new business models. For example, Monsanto is using soil information, yield data and climate trends gathered by tractors, machines and satellites to help farmers increase crop yields via a mobile application. GE is using sensors inside generators to analyze fuel costs, demand for electricity, and weather forecasts to optimize the mix of electricity on the grid between gas, solar and wind power. In addition to being a Jeopardy champion, IBM's Watson supercomputer is being used in a variety of health-care applications like better matching cancer patients with clinical trials to help battle cancer.

The semiconductor sector is likely one of the biggest beneficiaries of this trend as the amount of digital content gets embedded into almost everything. In today’s car, the number of sensors and cameras are increasing exponentially and enabling new safety and crash avoidance systems. Semiconductor manufacturing is also moving to the next nodes of smaller geometries that will provide even more compute power and memory capacity, while increasing battery life and lowering costs. The mainstream adoption of IoT is likely to take the next decade, but could also open up interesting investment opportunities in traditional industries that embrace and leverage the technology to transform their business.

Security is More Critical than Ever

The recent security breaches at Target, JPMorgan, Sony, etc. have highlighted the vulnerability of networks and growing importance of better cybersecurity to protect our information and infrastructure. Thousands of attacks occur each day and traditional IT security products like firewalls, gateways, anti-virus software, and tokens are no longer enough. As more data and transactions move online, the onslaught of attacks will only increase, while businesses and governments will likely have to continuously invest in new security solutions to fight back.

In the enterprise market, this new security threat landscape is creating a wave of new products in the areas of next-generation firewalls and endpoints, advanced threat protection, virtual sandboxing, cloud-based predictive monitoring, etc. On the consumer side, we are seeing biometric fingerprint technologies starting to proliferate on mobile devices, EMV chips on debit/credit cards, and other multi-factor authentication techniques. As we look into 2015, security remains one of the top IT spending priorities in many recent CIO surveys and we believe growth rates could accelerate as this never-ending battle with cybercriminals continues.

Technology Sector Outlook for 2015

The global macroeconomic volatility in the market is likely to continue for the foreseeable future, however, we maintain our positive view on the technology sector given the significant impact that these key trends can have on growth. There are many compelling investment opportunities across the major industries in technology – Internet, software and services, hardware and networking, semiconductors, and financial technologies.

We are disciplined in our approach to investing in the sector and look for companies that have key technologies or advantages, are gaining market share within their respective industry, and have substantial room for growth. At times, the innovative and disruptive nature of technology means we have to be willing to look farther out in time and assess a company’s longer-term growth prospects as these may become big growth stocks and maybe even the next Apple, Google or Facebook.

*CIO: Chief Information Officer

About Rainier Investment Management, LLC

The Rainier philosophy is simple. We invest in quality growth companies at prices that make sense. At Rainier, we believe that rewarding stock performance comes from companies with superior growth, attractive relative valuations, competitive strength, and financial integrity. Our decisions are based on fundamental analysis, which emphasizes bottom-up stock selection by sector specialists. We invest in all major market sectors because we believe that investment opportunities are found in industries that are frequently overlooked. Rainier remains focused on providing international equity, domestic equity, and fixed income portfolio management to financial advisors, institutional investors, and individual investors.

Opinions are subject to change at any time, are not guaranteed, and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible.

The S&P 500® Index is an unmanaged index composed of 500 industrial, utility, transportation and financial companies of the U.S. markets. Index vendor sources may vary, resulting in slight variations in the index returns that are displayed in performance reporting for the Rainier Funds. The Indices are not available for investment and do not incur charges or expenses.

Fund holdings and sector weightings are subject to change at any time due to ongoing portfolio management. References to specific investments should not be construed as a recommendation of the Fund or the Adviser to buy or sell securities and these investments do not represent all, and may represent a small percentage of, the Fund’s holdings. There is no assurance that the securities purchased remain strategy investments or that securities sold have not been repurchased. Current and future Fund holdings are subject to risk.

The Price to Earnings (P/E) Ratio reflects the multiple of earnings at which a stock sells. Earnings per share (EPS) is total earnings divided by the number of shares outstanding. The EV/EBITDA ratio, also known as the enterprise multiple, is the ratio of a company’s enterprise value to its earnings before non-cash items and is commonly used to value possible takeover targets. The PEG ratio (price/earnings to growth ratio) is a valuation metric for determining the relative trade-off between the price of a stock, the earnings generated per share (EPS), and the company’s expected growth. Forward earnings is a company’s forecasted, or estimated, earnings made by analysts or by the company itself.

The Fund’s investment objectives, risk, charges, and expenses must be considered carefully before investing. The statutory and summary prospectus contain this and other important information about the investment company, and may be obtained by calling 1-800-280-6111 or by visiting www.rainierfunds.com. Please read it carefully before investing.

The Rainier Funds are distributed by Quasar Distributors, LLC.

(c) Rainer Investment Management