After seven years of uneven growth trends following the 2008 financial crisis, we believe the global economy is likely to see a moderate acceleration in 2015. While several risks remain, we are reasonably confident that there are now enough growth drivers in place to help most major economies advance. First, the U.S. economy is now expanding at its fastest pace in several years and is likely to lift aggregate global demand appreciably. Second, fears of a sharp slowdown in China have faded as the country’s economy appears to have stabilized. Other large emerging countries such as India are likely to grow faster, though oil and commodity exporting countries are expected to see a decline. Third, the European Central Bank is likely to significantly expand its quantitative easing program while the Bank of Japan is expected to sustain its current policies. Finally, the sharp fall in oil prices should boost consumer demand across the world and improve the current account balances of large oil importers.

The Chinese government appears to have successfully stabilized the country’s economic growth at its target of around 7.5 percent. The recent rate cut by the central bank followed a moderate fiscal stimulus program in early 2014 and both of these measures were helpful to domestic demand. The stronger U.S. consumer demand favors exports from China and also exports from other Asian countries, such as Korea and Taiwan. In India, businesses and consumers are more optimistic after a pro-business federal government took office in June 2014. Lower inflation should allow the Indian central bank to cut interest rates in 2015. Similarly, Indonesia also has a new government that has promised reform measures to sustain long-term growth. On the other hand, we expect commodity exporters such as Brazil and South Africa to see subdued economic activity. Overall, we expect the economies of emerging market countries to grow faster than they have in recent years.

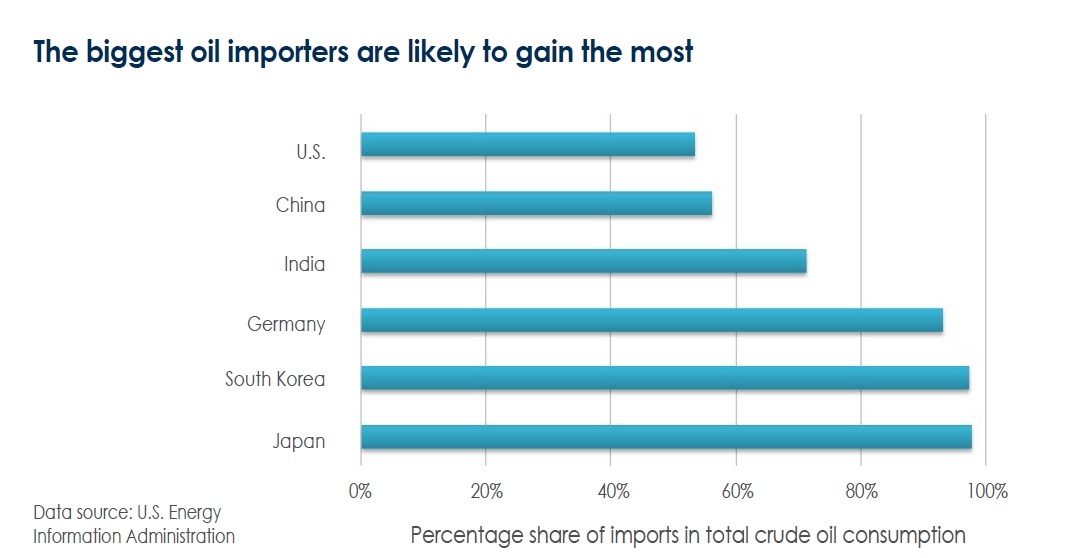

Cheaper Oil to Hurt Some, but Benefit Many More

The unexpected slide in oil prices since last September could be one of the major global growth drivers in 2015, if prices stabilize below $70 per barrel for the Brent benchmark. Lower pump prices should help ease household budgets in the U.S., Europe and China, and lift demand for other consumer products and services. This increase in consumption could trigger a virtuous cycle, and enable additional hiring and capacity expansions by businesses. Countries that are net energy importers would likely see their trade balances improve. Conversely, the major oil exporters such as Russia may feel the pain and see their economies weaken appreciably. But, on balance, we believe the global economy would likely gain from the drop in oil prices.

The United States and the United Kingdom

It took seven long years of aggressive bond buying and running ever larger fiscal deficits for the U.S. and the U.K. to regain their mojo, and both countries are now experiencing above average Gross Domestic Product (GDP) growth rates. Interestingly, this 2008 to 2015 recovery period was similar in length (eight years) to the time it took to restore normal growth during the Great Depression. It started on March 6, 1933 after President Roosevelt closed the country’s banks and continued until the Pearl Harbor attack on December 7, 1941. Now, the successful recovery of these two major economies has put a stamp of approval on the use of massive quantitative easing and increased government spending during deep recessions.

Japan

We believe that Japan could be the next major developed country to achieve sustainable growth. The decrease in consumer demand after the tax increase in April 2014 to a large extent negated the fiscal and monetary measures announced since the beginning of 2013. Policymakers have recently increased their stimulus by having the Bank of Japan raise its level of monthly bond buying and delay its second sales tax increase, which has the effect of raising the government’s deficit spending. Prime Minister Abe has retained power after the elections in December, which likely means continuation of the policy approach famously known as ‘Abenomics.’ Though the economic benefits of these measures may take a while to reveal, they have been highly favorable to Japanese equity prices since 2013.

The European Union

While there is a fair amount of pessimism about the current economic trends in the Euro-zone economy, we believe the outlook is gradually improving. Unlike the U.S. and Japan, the Euro-zone did not implement a monetary stimulus program that was meaningful in scale. Though the European Central Bank (ECB) did come up with modest quantitative easing measures and liquidity support to the banks, political differences within the ECB’s governing council have so far prevented a more aggressive approach. However, this may change as economic growth remains anemic and inflation remains well below the ECB’s target. Recent statements from the ECB president and other members of the council suggest that they are preparing for a significant expansion of quantitative stimulus if the previous measures do not deliver the desired results. Though more bond buying by the ECB may not do much for domestic demand in the short term, it could lift business and consumer sentiment. Also, as we have seen in the U.S. and Japan, aggressive quantitative easing is likely to be beneficial for equity prices. The wealth effect for households and lower capital costs for businesses that result from higher equity valuations could gradually lead to improved consumption and capital investments.

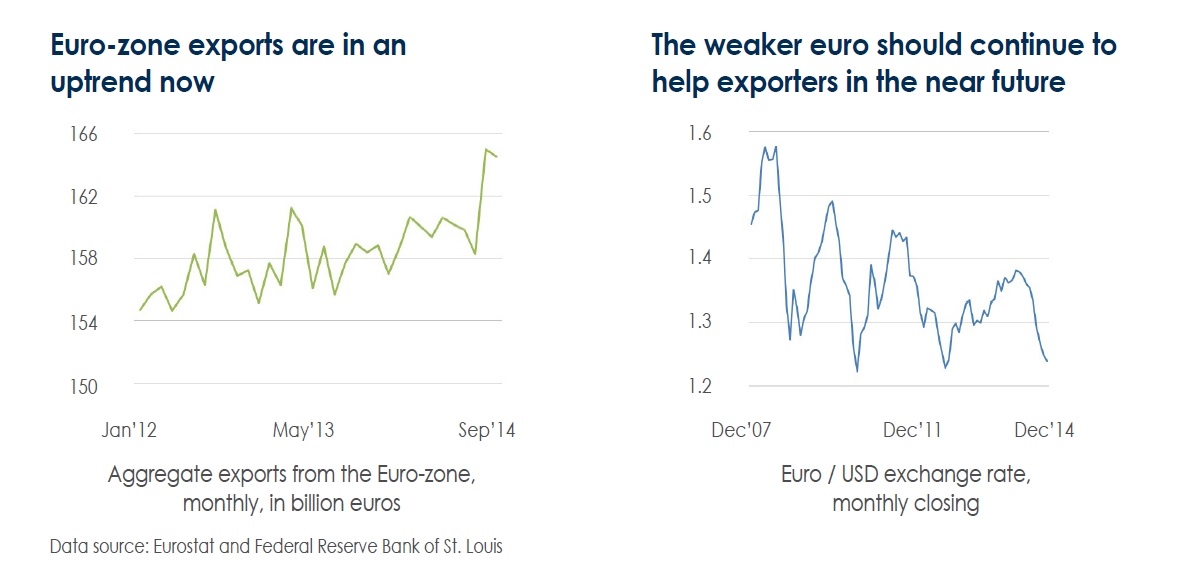

Another factor that has so far prevented a sustainable Euro-zone recovery is the uneven export trends for the region. In the recent past, European exporters have been hurt by subdued global demand as the U.S. growth was below normal and the emerging economies were slowing down. In addition, the relative strength of the euro against other major currencies hurt the region’s export competitiveness. These two headwinds are now easing for the Euro-zone. The U.S. economy is now expanding at the fastest pace in recent years, while growth in China and several other emerging markets appears to have stabilized. The euro depreciated all through 2014 and could fall further if the ECB rolls out additional monetary measures, making Euro-zone exporters more price competitive in foreign markets.

To conclude, differences in growth rates at the country and regional levels are likely to remain wide in 2015. These divergences will be most acute between the major energy exporters and importers. Nevertheless, 2015 is likely to see the beginning of an upswing for the global economy that could be sustained if the major countries initiate or maintain the necessary policy measures.

This article is for informational purposes only. This article is not intended to provide tax, legal, insurance or other investment advice. Unless otherwise specified, you are solely responsible for determining whether any investment, security or other product or service is appropriate for you based on your personal investment objectives and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation. The information contained in this article does not, in any way, constitute investment advice and should not be considered a recommendation to buy or sell any security discussed herein. It should not be assumed that any investment will be profitable or will equal the performance of any security mentioned herein. Thomas White International, Ltd, may, from time to time, have a position or interest in, or may buy, sell or otherwise transact in, or with respect to, a particular security, issuer or market on our own behalf or on behalf of a client account.

FORWARD LOOKING STATEMENTS

Certain statements made in this article may be forward looking. Actual future results or occurrences may differ significantly from those anticipated in any forward looking statements due to numerous factors. Thomas White International, Ltd. undertakes no responsibility to update publicly or revise any forward looking statements.

(c) Thomas White International