The economy

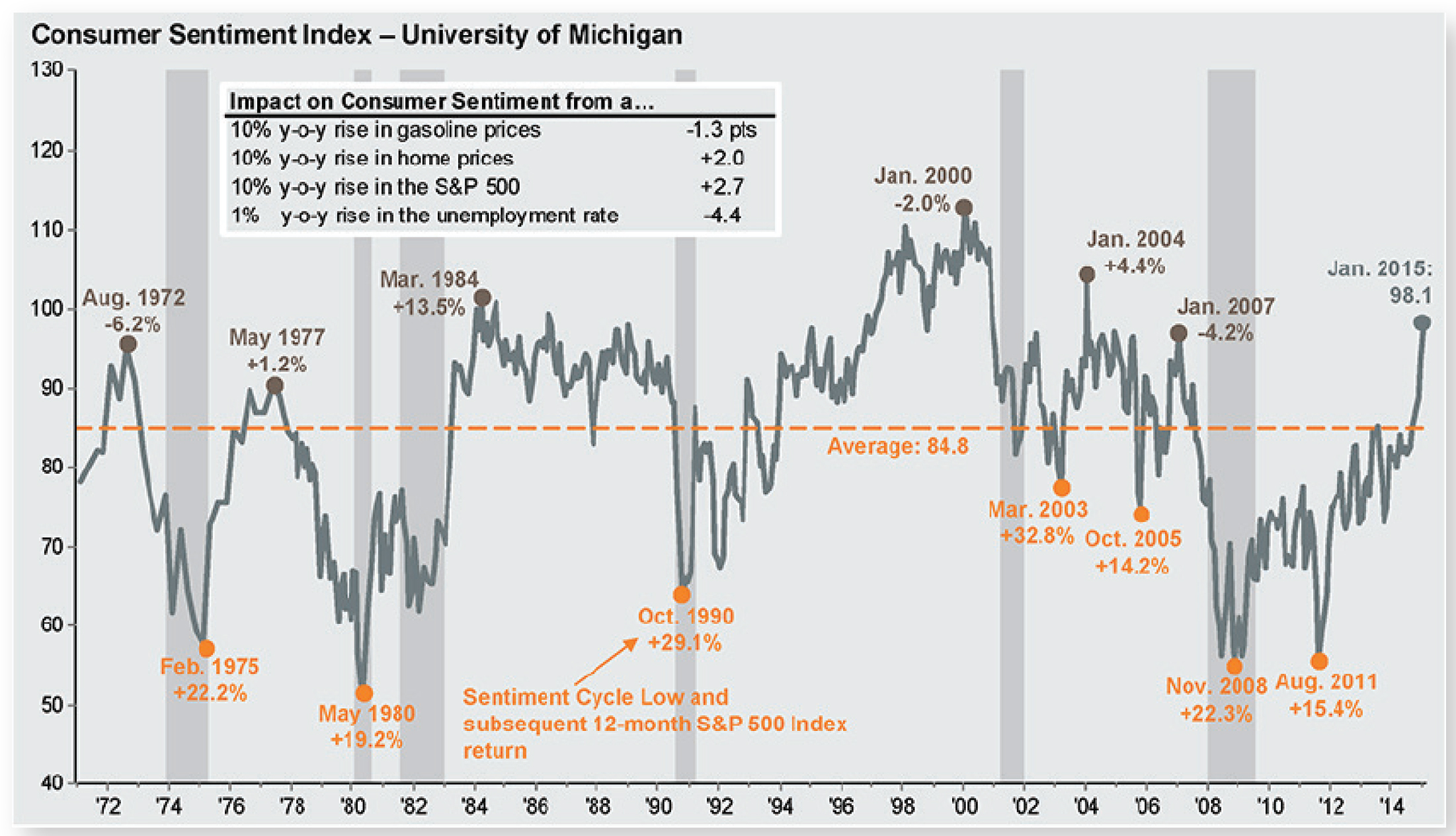

Confidence remains high for consumers

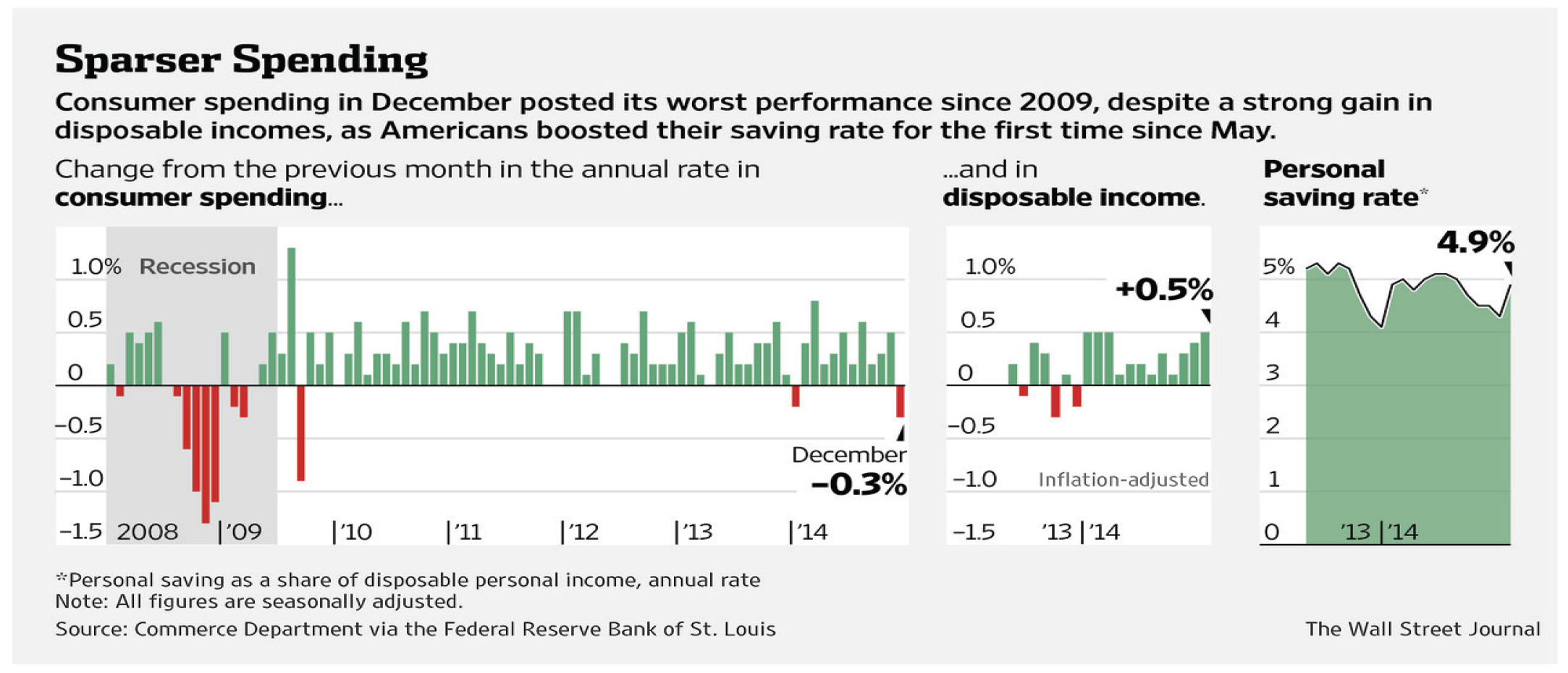

Consumers in the U.S. are showing their optimism by pushing a key consumer sentiment indicator to its highest level in over a decade. Despite a drop-off in Q4 GDP to a 2.6% annualized growth rate and three consecutive months of slowing manufacturing expansion, the U.S. economy still seems to be on strong footing. An interesting data point that many times gets bypassed is the consumer savings rate. Sitting at 4.9%, this rate rose about a half percent during the month as consumers decide to save the extra cash in their budgets resulting from lower gas prices. With wage growth continuing to be slow and inflation minimal, the increased savings rate could be taken as a sign that perhaps everyone is not as optimistic about the economy as more general reports on the health of the consumer indicate.

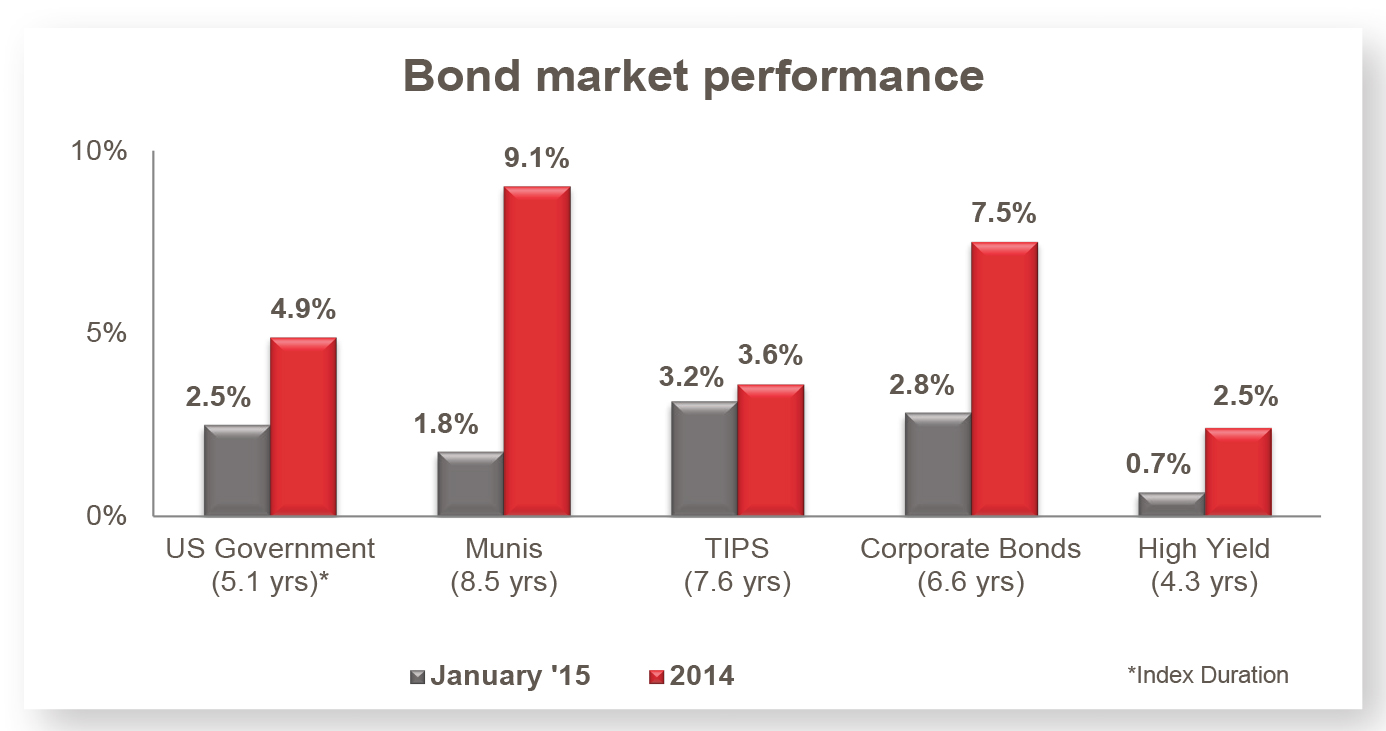

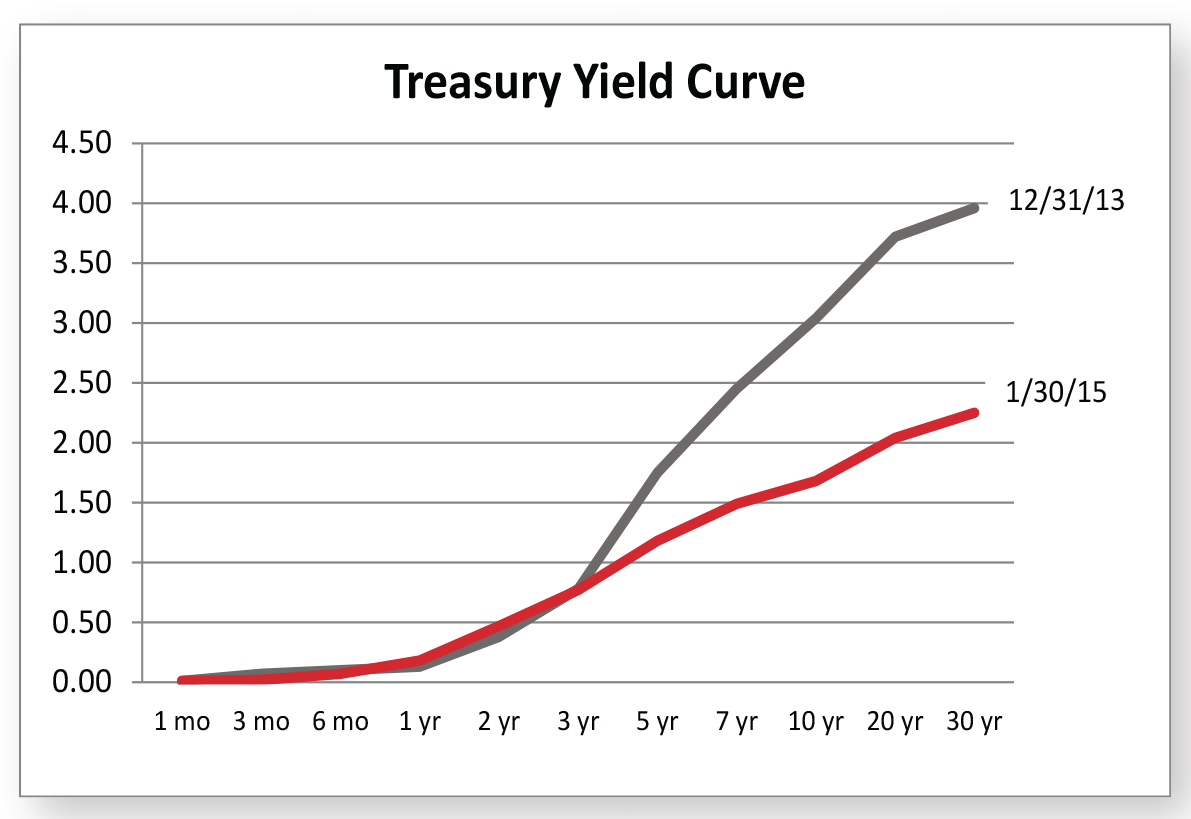

The bond market

Yield curve continues to flatten

In what amounted to yet another strong month for fixed income, the yield on a 30-year U.S. Treasury bond reached a record low of 2.25%. It was only a month ago that a 10-year note offered the same interest rate, showing the continued flattening effect of the yield curve and highlighting the recent volatility in interest rates. U.S. bonds continue to see strong demand due to higher interest rates relative to international markets. Some investors may also be attempting to hedge currency risk by staying domestic. In a much-anticipated move, the European Central Bank announced its own form of quantitative easing in January. The amount of €60 billion per month was more than expected, highlighting the commitment by ECB president Mario Draghi to counter deflation and stimulate the Eurozone economy. With new foreign monetary policies arising and a “patient” Federal Reserve, interest rates in the U.S. are likely to stay low through at least the first half of 2015.

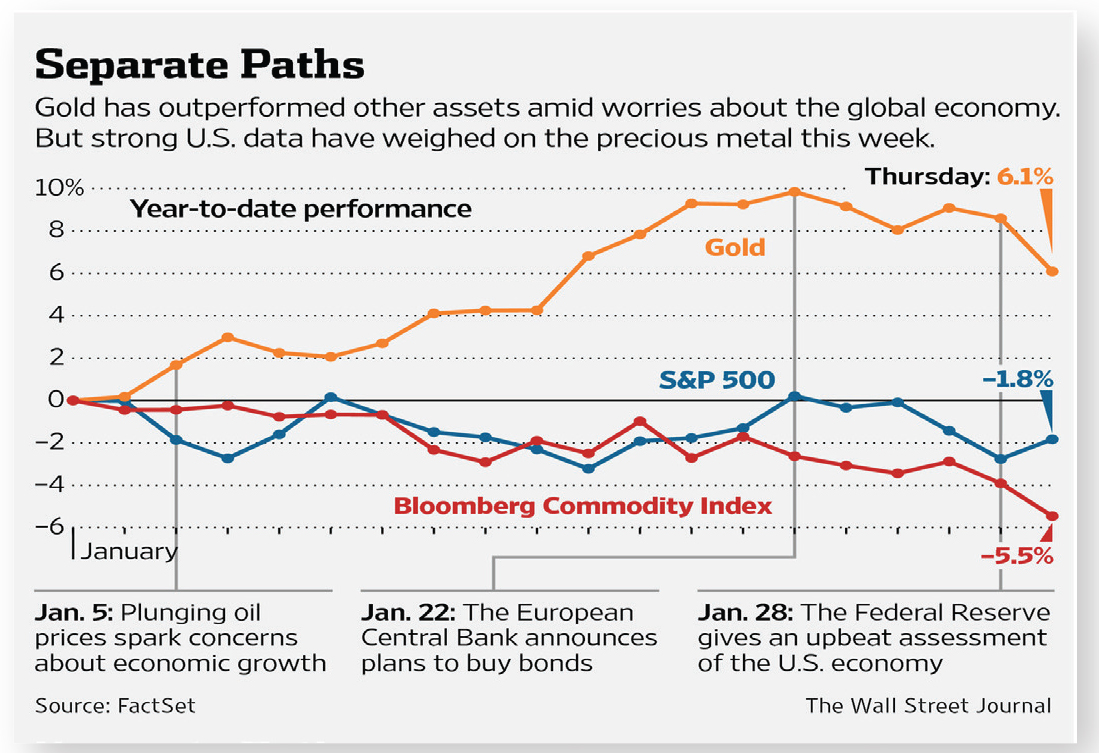

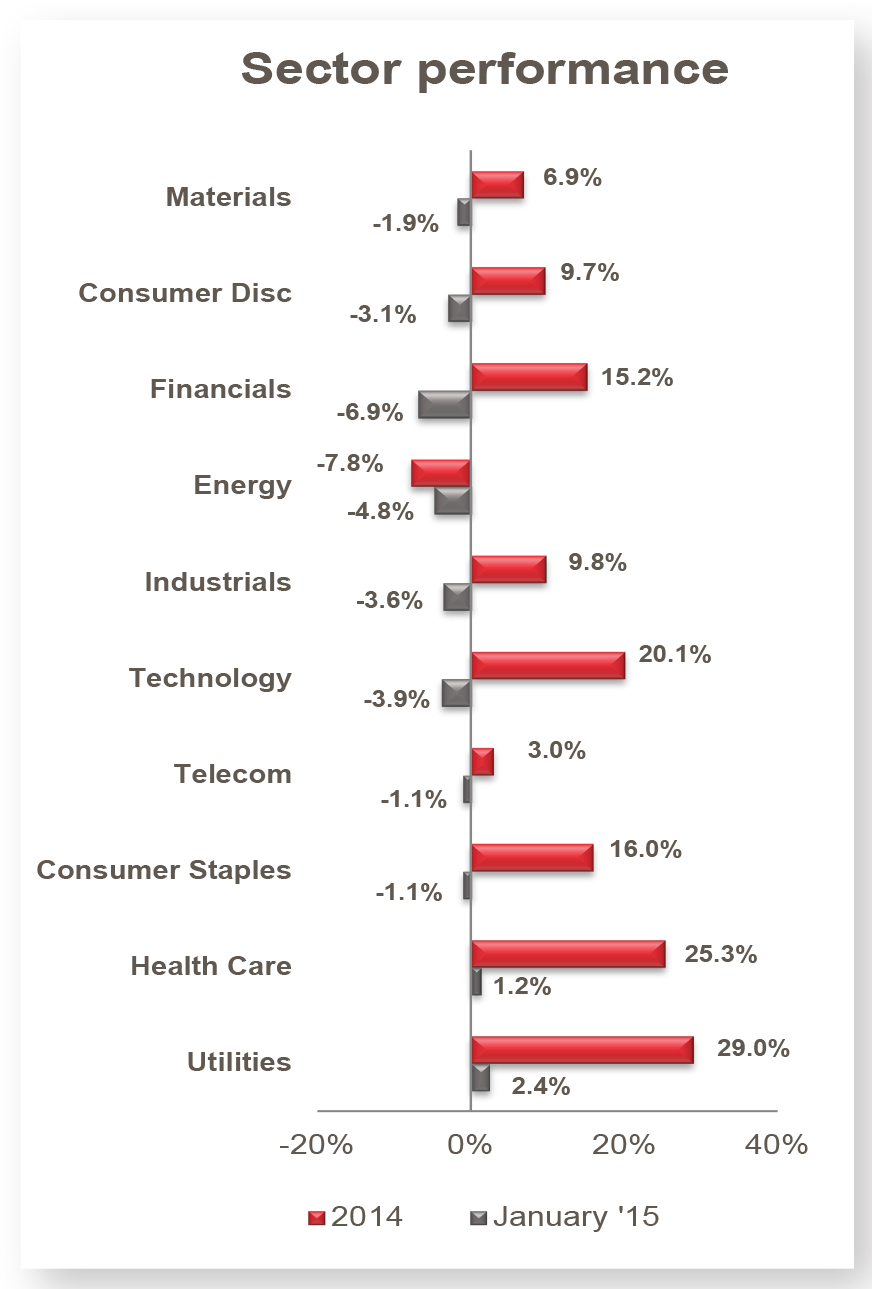

The stock market

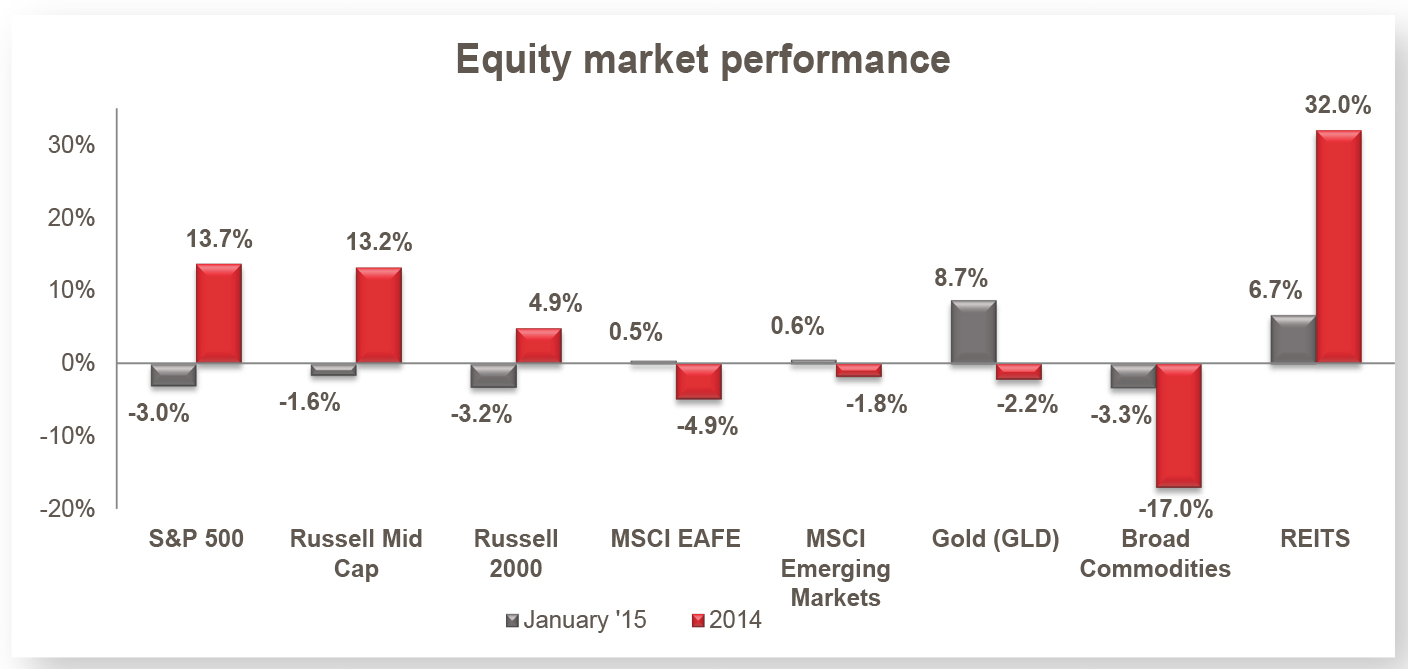

January reversal for stock market

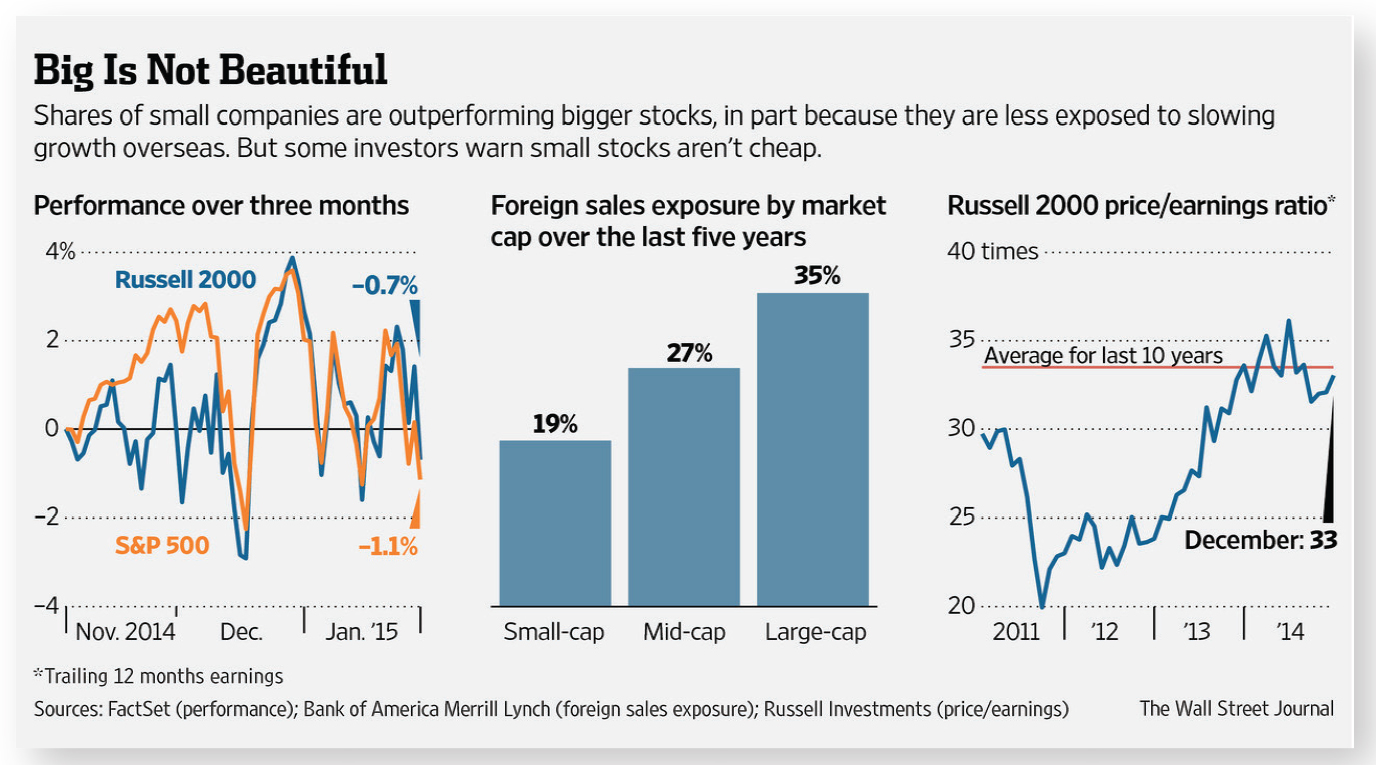

With U.S. stocks leading the way in global markets during 2014, a strong reversal took place in January as domestic markets pulled back and international markets stayed slightly positive. Gold experienced a major turnaround with an almost 9% return in the month, while energy-related investments continued their downward trend. Fourth quarter earnings are taking center stage with many companies citing currency exchange rates and the strong U.S. dollar as a cause for lower profits. From a sector standpoint, defensive companies have held up well, while energy and financial stocks have accounted for the most notable losses. P/E ratios continue to hover around 25-year historical averages, with some areas looking more expensive than others. After a strong run in U.S. stocks during the previous two years, now is a very important time to be well-diversified across multiple asset classes, as evidenced by the short-term swing in market leaders experienced in January.

|

Indexes |

YTD |

Treasury yields |

|||||

|

Stock indexes |

Prime rate |

3.25% |

6-month |

0.07% |

|||

|

Dow Jones |

17,165 |

-3.58% |

LIBOR rate (3 mos.) |

0.24% |

1-year |

0.18% |

|

|

S&P 500 |

1,995 |

-3.00% |

Unemployment rate |

5.7% |

2-year |

0.47% |

|

|

NASDAQ |

4,635 |

-2.08% |

15-year mortgage rate |

3.06% |

5-year |

1.18% |

|

|

Bond indexes |

30-year mortgage rate |

3.78% |

10-year |

1.68% |

|||

|

Broad Market Barclays Agg |

2.10% |

CPI (12-mo. ending 12/31/2014) |

0.8% |

30-year |

2.25% |

||

|

US Corporate Barclays Capital |

2.83% |

GDP (fourth quarter 2014) |

2.6% |

||||

|

US Government Barclays |

2.50% |

Oil price (price/barrel) |

$48.24 |

||||

|

Mortgage-Backed Barclays |

1.80% |

Gold (oz.) |

$1,279 |

Economic trends

|

Indicator |

3 Month Trend |

Our Outlook |

|

|

Consumer confidence |

|

Positive |

§ The consumer confidence index rose in January to a reading of 102.9, up from 93.1 in December. (1985=100, The Conference Board) § University of Michigan/Reuters consumer-sentiment index rose in January to a reading of 98.1, recording its highest reading in a decade. (Reuters) |

|

Spending |

|

Neutral |

§ Retail sales fell in December by 0.9% from a month ago. (Commerce Department) § Consumer spending fell by 0.3% in December from a month ago, while personal incomes also rose 0.5%. (Commerce Department) § The savings rate rose in December to 4.9%. (Commerce Department) § The household debt service ratio (debt to disposable income) was at 9.92% as of Q3 2014, down from 13% in 2008 as mortgage obligations have fallen. (Federal Reserve) |

|

Manufacturing |

¯ |

Positive |

§ January reading fell from 55.1 to 53.5. The index has now fallen for 3 consecutive months, but is still showing expansion in the sector at a reading above 50. (Institute of Supply Management) § Inventories of manufactured durable goods rose by 0.5% in December. (US Census Bureau) |

|

GDP growth |

|

Positive |

§ In the Commerce Department’s first estimate, fourth quarter GDP rose by an annualized 2.6%. This is coming off of a 5% growth rate during the third quarter. (Commerce Department) |

|

Inflation |

|

Positive |

§ CPI declined by 0.4% in December from a month earlier and 12 month CPI fell to a rate of 0.8%. The gasoline index was the main reason for the drop in CPI. (BLS) § Core CPI (CPI – food & energy) was unchanged in December from the month prior and the annual rate fell slightly to 1.6%. (BLS) |

|

Housing |

« |

Neutral |

§ The 20 city Case-Shiller Index (home-price readings) fell by 0.2% in November from a month ago, and the index was up 4.3% over the past 12 months. (S&P) § Existing home sales rose by 2.4% in December from a month earlier. (NAR) § New home sales rose by 11.6% in December from a month earlier. (NAR) |

|

Job growth |

|

Positive |

§ The U.S. added 257,000 jobs in the month of January. The unemployment rate rose from 5.6% to 5.7%. The rate rose because the labor force grew, a sign of growing confidence among households. (Labor Department) |

Headlines

Consumer sentiment at highest level since 2004.

Source: University of Michigan, FactSet, JP Morgan Asset Management

Savings rate higher as consumers pocket extra money from lower gas prices.

Source: The Wall Street Journal

Equity markets

Source: Morningstar, Inc.

U.S. stocks see volatility to start the year, while foreign stocks turn positive.

Commodities move lower as oil prices fall, however precious metals start strong.

Defensive sectors show strength during volatile month of January.

Source: Wall Street Journal

Source: Wall Street Journal

Source: Morningstar, Inc.

Fixed income markets

Source: Morningstar, Inc.

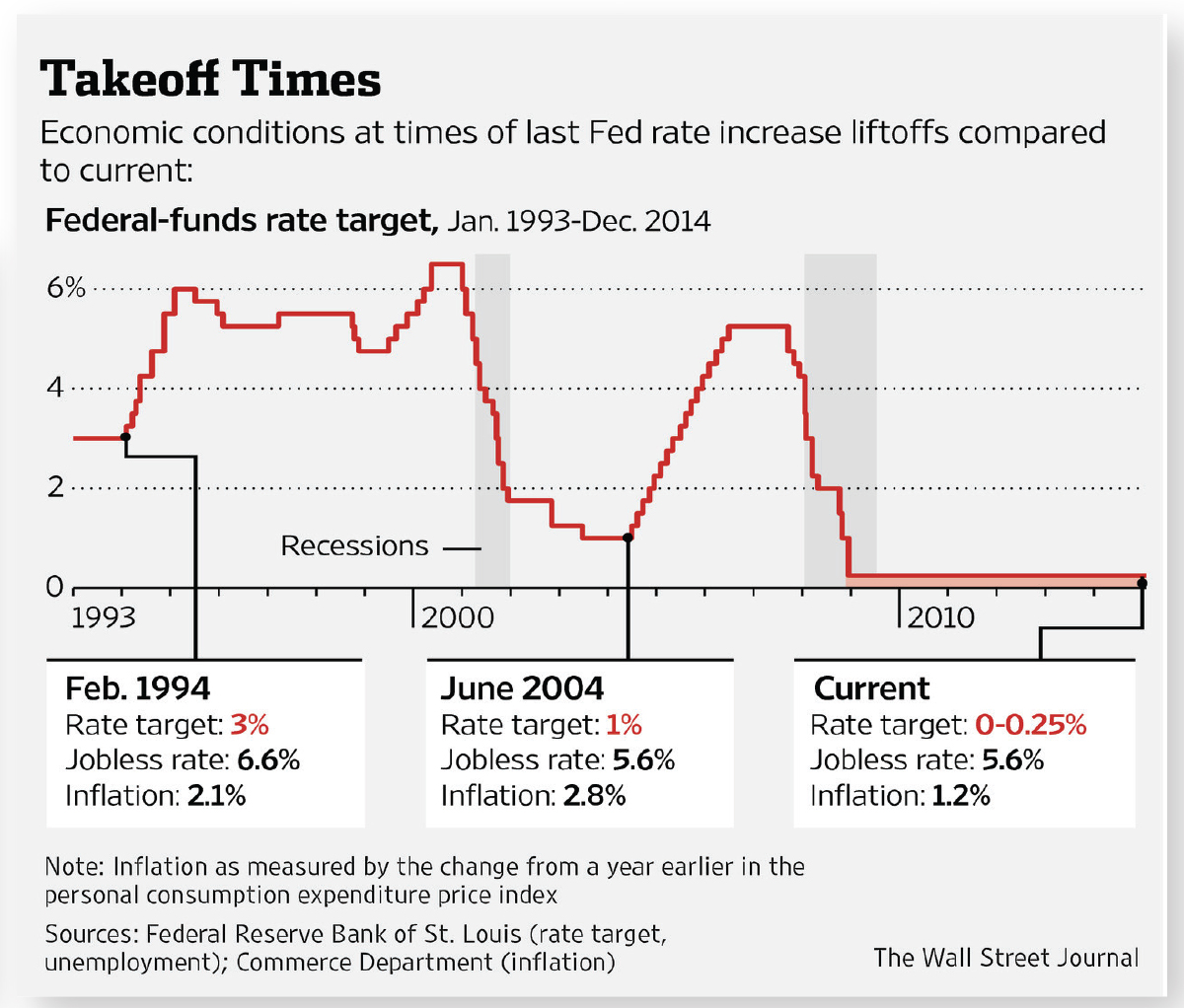

Federal Reserve weighs rate-hike policy against strong U.S. economy versus low inflation and global growth concerns.

Bonds show impressive start to the year as demand continues to be high.

Interest rates fall across all maturities. 30 year bond at record low rate of 2.25%.

Source: U.S. Department of Treasury

Source: The Wall Street Journal

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2015 Bronfman E.L. Rothschild, LP