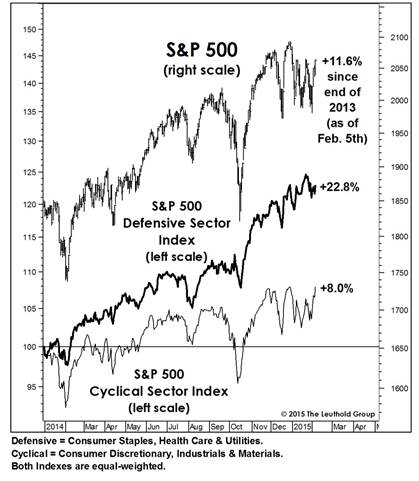

Last year’s economically defensive winners held their grip on stock market leadership in January. This action is consistent with our view that the bull market is an aged, overvalued one that has begun a final “distribution” process that will eventually erupt into a cyclical bear.

Like every other facet of the topping process, though, defensive leadership can persist for an extended period—to the point that it’s ignored when there’s a genuine warning to be heard. (Chart 1) Health Care, for example, has been a winner for four years—yet sector valuations have recovered just to mid-range. (We’ve held the Managed Health Care stocks in our Select Industries portfolio for 63 consecutive months.) Consumer Staples doesn’t look especially expensive, although Utilities do. Health Care and Consumer Staples sectors rate #2 and #3 in a roll-up of our domestic industry group rankings, while Utilities is #7.

Chart 1

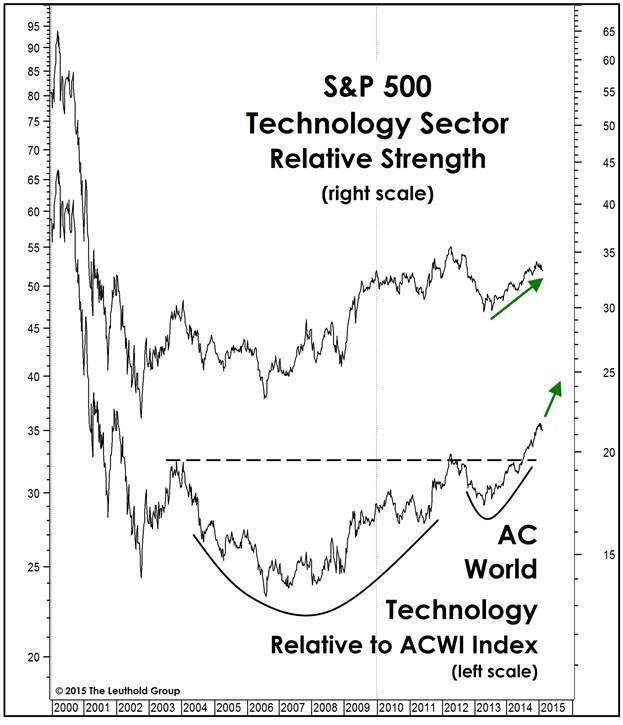

The top-rated sector in our work with the February scores is Information Technology, with seven industries on the Attractive list (defined as the top quintile of our 115-group universe), and another two IT industries are rated High Neutral (second quintile). While Technology’s relative upswing certainly plays into its appeal in our group rankings, its valuations also play a role—with the sector’s median trailing P/E (20.6x) and median price/cash flow ratio (13.9x) essentially equal to those of the median stock. These relative valuations are the lowest since the early 1990s.

Finally, the ACWI Technology sector has (on a relative strength basis) broken out from a textbook “cup and handle” pattern that was more than ten years in the making (Chart 2). The relative pattern in domestic Technology hasn’t been quite as powerful, but we expect the direction to remain up—with the sector our best bet for long-term stock market leadership (i.e., three-to-five years).

Chart 2

© 2015 The Leuthold Group