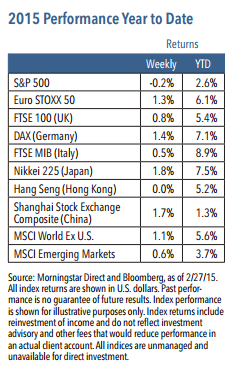

U.S. equities were mixed last week, with the S&P 500 declining -0.2%.1 The Federal Reserve (Fed) had a busy week, as the nuanced debate continues around when to begin policy normalization. The global policy divergence grabbed headlines, but the focus was mainly on negative yields in Europe and inflows to non-U.S. equities. Following the bounce in U.S. equities over the last few weeks, discussion emerged about potential headwinds such as valuation and near-term Fed tightening. Consumer sectors were the best-performing, while energy, utilities and industrial sectors showed weakness.1

Weekly Top Themes

1. The Fed continues to leave the door open to options. Janet Yellen indicated “there will not be a rate hike in the next couple of meetings.” All options seem to be on the table beginning with the June FOMC meeting. The Fed wants greater flexibility to raise interest rates, and economic data will become more important. Increased uncertainty should put pressure on longer-term rates.

2. U.S. economic conditions no longer require a zero interest rate policy. The Fed should begin to normalize interest rate policy relatively soon. We anticipate the onset of policy tightening, which has not occurred in the United States in almost a decade,2 will act as a revaluation catalyst for the long end of the global yield curve.

3. Historically, equities have performed well at the start of a rate hike cycle. Generally, equities seem to produce gains when interest rates start to creep up, then often pause for a few months before continuing to climb.1

4. The oil price decline should be a net long-term positive for U.S. and global growth. Over time, the benefits of declining prices should make up for the near-term pullback in oil production.

5. The bull market is nearly six years old. Investors have faced many steep walls of worry. The economy has been growing, and the stock market has been rising as a result of profits from entrepreneurial activity. We anticipate these trends will continue until corporate profits fall sharply, interest rates rise significantly or the stock market increases beyond the current value of discounted earnings.

The Big Picture

In the near term, significant crosscurrents lie beneath the surface. Risks are emerging, as the market appears complacent and leadership is less prominent. The market’s view of the Fed seems aligned with FOMC statements and data, and although inflation is not a concern, disinflation discussions are growing stale.

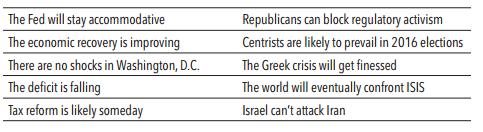

As we think about the intermediate term, we highlight key reasons to stay optimistic, as recently discussed by Potomac Research Group:

The Fed will stay accommodative Republicans can block regulatory activism

Assessing the environment overall, equities are hovering near the top of the range that began last fall. Reduced U.S. liquidity will force profits — which have entered a difficult phase — to become the primary driver of capital appreciation. Pricing power, rising wages and a strong U.S. dollar have dampened earnings projections. We believe the global economy is slowly healing, and low inflation allows policymakers to provide reflationary support. The extension of the Greek bailout program provides potential for the global economy to shift into higher gear by enabling the fledgling European recovery to gain traction. However, high levels of debt, geopolitical turbulence, low inflation and concerns about financial bubbles require caution. A combination of improving global growth and reflationary monetary policy underpins our pro-growth investment stance, including an overweight to equities. We believe equities will achieve positive returns in 2015, and likely outperform cash, bonds, inflation and commodities, but not without a bumpy ride.

1 Source: Morningstar Direct, as of 2/27/15 2 Source: Federal Reserve

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM1-0315P 6451-INV-W03/15