Equity investors can be categorized into a broad range of equity strategies, including valuation-based approaches, whereas bond investors generally think in terms of interest rates and duration management. Professional investment managers have been taught that the market is efficient and while this may often be true, we believe there are a number of select areas within the bond market that exhibit less efficient behavior. This paper will discuss these potential inefficiencies and how “value oriented” bond management looks to exploit the inefficiencies. First we need to define “traditional” vs. “value oriented” bond management, then we will turn to a discussion of these perceived inefficiencies.

Traditional Bond Management

As we define it, “traditional” bond management generally focuses on macroeconomic and interest rate forecasting leading to duration based decisions. Often traditional bond investors spend a great deal of time monitoring the Federal Reserve and predicting its expected actions as well as forecasting broad economic outlooks. We believe this type of interest rate forecasting is inherently difficult and does not result in a repeatable competitive advantage.

In addition, some traditional bond managers will add yield curve forecasts and sector expectations to their tool box. Occasionally these investors will invest in credit risk oriented bonds; however, any such decision is often driven by an economic forecast and is likely indifferent as to a specific bond issuer or issue. We feel there are many more opportunities to uncover value in the bond market than this traditional approach would suggest.

Value Oriented Bond Management

“Value oriented” bond management, as we define it, is an approach to bond selection and management whereby a unique value oppor- tunity related to a particular bond issuer or issue is identified. The concept behind this issuer and issue focused approach is to not only identify an inherent underlying value, but to also identify a catalyst that might result in realization of that value. Thus, we see it as a “bottom up” analysis with a value focused perspective. Value oriented bond management is less dependent on interest rates as a consequence of the non-interest rate catalysts often involved in the value proposition. We believe that while the inputs and events will vary, the process of analysis involved in value oriented bond investing may be repeatable.

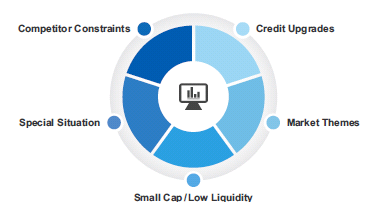

As previously mentioned, value oriented bond management focuses on potential exploitation of a variety of perceived market inefficiencies, which can create value. We break these into several broad categories.

We start with Credit upgrades because we believe that credit

upgrades are a common element in many value oriented bond portfo- lios. The concept with credit upgrades is to identify an issuer or issue that may improve in credit quality which, in turn, may result in a reduc- tion in the yield required by investors to own it. This reduction in yield, if realized, could create issue-specific gains that are independent of overall market performance. We believe that when pursuing a credit upgrade it becomes critical to identify the most effective issue in the capital structure to utilize. In our view this is typically the longest duration security in the issuer’s capital structure.

A second inefficiency where opportunities can arise are market themes. Thematic opportunities are generally developed from research or recognition of a situation where similar or common characteristics exist among multiple bond issuers or issues. Market themes may be broken into two broad categories – recurring or opportunistic.

Recurring themes tend to exist for a long time and may be almost permanent market features. For example this could include charter “arbitrage” and small cap/liquidity opportunities, which are explained in more detail below. These opportunities persist due to enduring market limitations and inefficiencies.

Opportunistic themes tend to have a shorter life that may only exist for months or a few years. Examples of this might be high coupon bond tenders and selected industries subject to merger and acquisi- tion. For example, in the current environment many issuers have high coupon bonds that may have call protection. The only way to refund this debt is through bond tenders where a premium of 2-3(+) points may be required to encourage bondholders to tender. This opportu- nistic theme will disappear over time.

Certain industries may be prone to merger and acquisition activity. The idea in this case is to identify lower quality issuers that may be acquired by higher quality issuers, potentially realizing an increase in credit rating as a result.

Small Cap or Low liquidity opportunities can arise for several reasons. With small cap bond issues, we believe that, in addition to an illiquidity premium, there may be fewer competing investors because of limited information flow and/or limited ability to interpret available information. A quick to market approach may be beneficial when an information advantage is perceived, as other investors will “catch up” and reduce inefficiency. Examples of these opportunities would be companies that are underrated due to size but hold prospects for growth or the probability of a takeover by larger, higher quality issuers. Another example would be a situation where a company has the possibility of self-liquidity, which could result in the capitalization of the acquired illiquidity premium.

Special situations, as we define them, involve unique, non-tradi- tional fixed income or fixed income like opportunities. Special situa- tions could have elements of credit quality uncertainty, lower liquidity, unusual covenants and/or complex structure. Special situations could also involve market inefficiencies resulting from charter restrictions or firm culture.

Competitor constraints, as we define them, may occur for many reasons. For instance, some smaller investors may not commit resources to credit analysis or other elements of value oriented bond investing. At the same time, some opportunities may not be consid- ered feasible by larger investors with many billions of dollars under management.

Finally, some bond market investors, for cultural, charter restrictions or other reasons, may not be prepared to act outside of traditional bond management. For example, cultural restrictions might occur if an institution self-imposes a complicated or cumbersome decision making process.

An example of a charter restriction might be an insurance company that is restricted from buying BB bonds because of regulatory reserving requirements. While the issuer of such a bond may be in the process of becoming BBB, the insurance company could not purchase the issuer’s bond until the rating improves. However, investors without such a restriction could buy the bond at any time. We refer to this as “charter arbitrage”.

In conclusion, as outlined above, value oriented bond management seeks to exploit perceived market inefficiencies and identify individual issue or issuer-specific opportunities in an attempt to add value. We believe this bottom-up, value oriented process can be considered as an alternative or complement to traditional bond management, which focuses on top-down factors like interest rate movements, duration management, and economic forecasting.

Zach Jonson, CFA, (left) is Senior Vice President of Investment Management and co-portfolio manager of the ICON Bond, High Yield Bond and Risk-Managed Balanced Funds. He is also portfolio manager for the ICON Materials Fund and serves as a member of the ICON Investment Committee.

Jerry Paul, CFA, (right) is Senior Vice President of Fixed Income and co-portfolio manager for the ICON Bond, High Yield Bond, and Risk-Managed Balanced Funds. Jerry has over 35 years’ experience in investment management and research.

The data quoted represents past performance, which is no guarantee of future results.

Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securi- ties generally decreases. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher- quality bonds.

Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies. ICON’s value approach involves forward-looking statements and assumptions based on judgments and projections that are neither predictive nor guarantees of future results.

Consider the investment objectives, risks, charges, expenses, and share classes of each ICON Fund carefully before investing. The prospectus, summary prospectus, and the statement of additional infor- mation contain this and other information about the Funds and are available by visiting www.Investwith- ICON.com or calling 1-800-828- 4881. Please read the prospectus, summary prospectus, and the statement of additional information carefully before investing. ICON Distributors, distributor.