THe MISERY INDEX: June 1980

In June 1980, the U.S. economy was just exiting the first of two back-to-back recessions. The June 2, 1980, cover of TIME magazine was “The Big Blowup,” referring not to the awful state of the U.S. economy, but to the recent eruption of Mount St. Helens in Washington state. The Business and Economy section of the magazine that month, however, was full of stories about just how bad the U.S. economy was:

- June 9, 1980, “Consumers Feel the Pinch”: “With the economy in a downward spiral of still uncertain depth, many consumers have decided to cut their losses. …More Americans are unemployed, many others are doing without overtime pay, and inflation has eroded earnings."

- June 16, 1980, “The Bad News Gets Worse”: "…not only has the next recession begun, but it is already shaping up to be one of the worst slumps since the Great Depression of the 1930s.”

- June 30, 1980, “Harder Times in the U.S.": “While the Europeans generally hope to suffer only a mild slowing of economic growth, U.S. business continues to reel downward.”

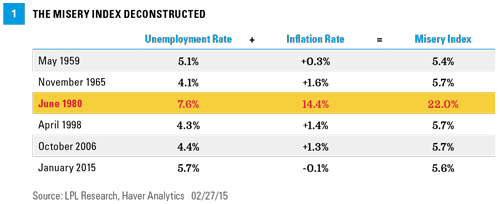

The unemployment rate hit 7.6% in June 1980 and the inflation rate (as measured by the year-over-year percent change in the consumer price index [CPI]) soared to an incredible 14.4%, pushing the Misery Index (year-over-year percent change in the CPI plus the unemployment rate) to 22.0% [Figure 1]. In retrospect, the 14.4% reading on CPI in June 1980 marked the high point for inflation in the late 1970s/early 1980s. Unfortunately, for the U.S. economy, the next recession (the one that would begin in mid-1981 and last through the end of 1982) would ultimately drive the unemployment rate to 10.8%. The economy in the early 1980s was truly miserable, matching the nation’s mood.

THe MISERY INDEX: THEn AND NOW

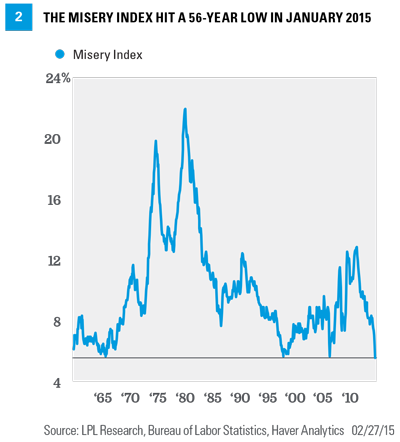

Interrupted only by the 1990–1991 recession, the Misery Index fell steadily for the next 20 years [Figure 2], hitting just 5.7% in April 1998, with the unemployment rate at 4.3% and the inflation rate at just 1.4%. By this time, TIME magazine had a Technology section, and the stories that month were about the latest “web-search” engines and Windows 98, while the Business section discussed “How OPEC Lost Control of Oil” and the latest wave of mega mergers in the banking sector. Times were good, and the nation’s mood—and the Misery Index—reflected it.

Last month, reports on the CPI (-0.1%) and unemployment rate (5.7%) for January 2015 sent the Misery Index down to 5.6%, surpassing the lows hit in 2006, 1998, and 1965, leaving the index at the lowest level in 56 years (May 1959). Although the economic and business headlines have certainly improved since 1980, they don’t quite have the same feel to them as they did in 2006, 1998, 1965, or even 1959—the last time the Misery Index was lower than today.

But are the unemployment rate and the inflation rate still the best measures of the misery (or lack thereof) of the American people in 2015? The index itself was created by economist Arthur Okun in the 1960s, and updated by economist Robert Barro in the late 1990s, who added interest rates and gross domestic product (GDP) to Okun’s index; and it could use a refresh as we head toward the second half of the 2010s. That is a good topic for a future edition of the Weekly Economic Commentary.

So why, with the economy closing in on a sixth year of expansion, the S&P 500 within a few points of an all-time high, and gasoline prices near six-year lows, doesn’t the nation’s mood match the best reading in 56 years on the Misery Index?

According to the latest Gallup poll asking Americans what the nation’s most important problem is, the “economy in general,” “unemployment and jobs,” and the “federal budget deficit/federal debt” were the top economic concerns; while “dissatisfaction with government,” “healthcare,” and “terrorism” topped the list of non-economic concerns. Although it would be easy to add a numerical value for the deficit or debt levels; the approval rating of Congress; tax rates; the number of pages of federal, state, and local regulation; or the even the latest approve/disapprove numbers on the Affordable Care Act to get a better gauge of American’s “misery,” that still may not capture what’s going on.

Conclusion

The disconnect may come down to wages. Federal Reserve (Fed) Chair Yellen noted not once, but twice in her prepared remarks on monetary policy and the economy before Congress last week (February 23-27, 2015), that wage growth remains “sluggish.” Indeed, average hourly earnings in January 2015 were just 2.0% ahead of their January 2014 level, and running well below the pace of wage growth (4.0%) seen prior to the onset of the Great Recession in 2007 [Figure 3]. Yellen’s signal to markets last week was that while the Fed was happy with the progress the labor market has made toward the Fed’s goal of “full employment,” it was not yet convinced that the inflation portion of the Fed’s dual mandate was on the right track. As we have written many times in this and other commentaries, wages are a key component of business costs, and the economy won’t see a sustained rise in inflation back toward the Fed’s 2.0% target until wage growth begins to accelerate. Once that happens, the Misery Index may or may not be at all-time lows, but perhaps consumers will feel better about the state of the economy.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.

Consumer price inflation is the retail price increase as measured by a Consumer Price Index (CPI).

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

(c) LPL Financial