Increasing financial disintermediation is a strong secular theme providing tailwinds in several financial industries, but a likely arduous and complicated process warrants the need for a disciplined focus on both risk and reward.

The financial system essentially performs one basic function—the direct or indirect movement of funds from savers to borrowers or investors. Although financial disintermediation is formally defined as the shifting of funds from indirect to direct financing, the term is more commonly used to describe the increasing role of non-bank intermediaries (brokers, pension funds and mutual funds, insurance companies, and financing companies) in the financial markets.

A number of factors drive financial disintermediation, including increased bank regulations, financial liberalization, stable institutional investor base and technological innovations. These factors are securely entrenched in many markets, most notably the U.S., and are gaining momentum in other countries. Against this backdrop, the role of traditional banks in the global financial system is in a secular decline, while the growth potential in other industries is on the rise.

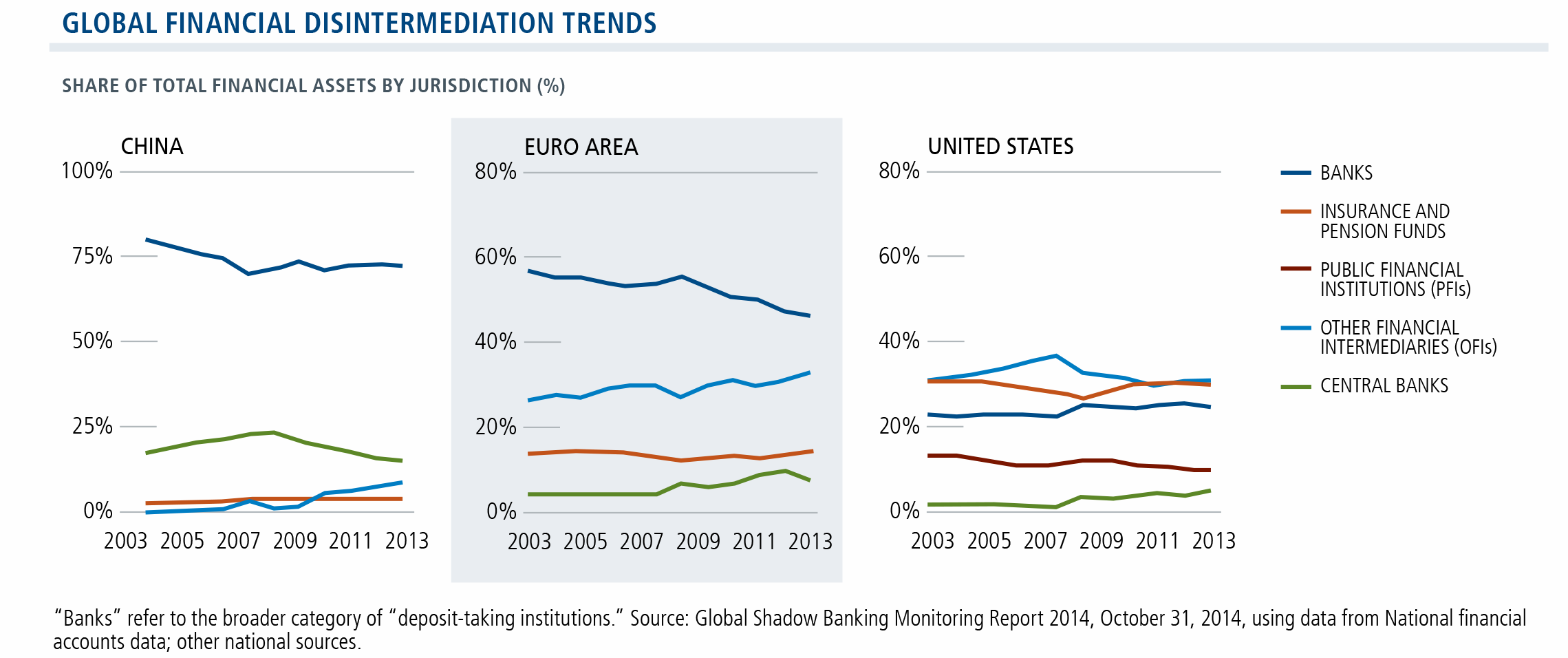

The most highly disintermediated financial market in the world is the U.S., where banks currently account for about 25% of total financial assets. While we don’t expect financial disintermediation in Asia and Europe to catch up with the U.S. any time soon given structural market differences, the trend toward disintermediation will likely be more pronounced in these regions.

Asia

The banks remain the primary financial intermediary in Asia, accounting for more than 60% of total financial assets, but similar to the U.S. during the 1970s, high rates are increasingly motivating savers/borrowers to seek alternative sources of investment/financing. The expansion of non-bank intermediaries is further supported by financial liberalization, the wealth effect, and a highly regulated banking system.

We believe China presents one of the most notable opportunities for disintermediation, given both the size and inflated role of banks in the country’s financial system. The rapid growth of the shadow banking system has been well documented by pundits as a failed attempt at financial disintermediation due to the limited transparency and implicit guarantees from the banking system. While concerns about some key elements of the Chinese shadow banking system are well founded, we are more optimistic about the longterm prospects for disintermediation and the resulting growth opportunities in key non-bank financial industries. The underlying driver remains intact: an overly regulated banking system has motivated savers/borrowers to seek alternatives. A great deal clearly needs to be done to develop a more balanced financial system capable of properly pricing risk and allocating capital more efficiently, but real progress has been made–interest-rate liberalization, equity/bond market reforms, new market and product trials (including assetbacked securities [ABS], municipal bonds, and derivatives), and promotion of an institutional investor base (such as insurance deregulation, pension system, and HKEx Connect).

China has a reputation for moving slowly, and the disintermediation of its banking system is particularly tricky given the need to balance long-term objectives with the more immediate liquidity and credit risks, but small changes at the margin would still be very meaningful to non-bank intermediaries. To put the opportunity into perspective, with total social financing in China at more than $20 trillion (USD), a 1% disintermediation of the banking system translates to an increase in non-bank intermediary assets of $200 billion. According to a recent Financial Stability Board study (“Global Shadow Banking Monitoring Report 2014,” October 30, 2014), China’s banking system still accounts for nearly 75% of total financial assets versus a global range of 40-60% (U.S. is 25%). To gain exposure to this theme, we have opportunistically held positions in the brokerage, insurance and asset management industries.

Europe

Among the more developed economies, financial disintermediation has historically been more challenged in Europe, with banks accounting for approximately 60% of financial assets. However, there has been a pronounced increase in disintermediation following the global financial crisis. In a more restrictive regulatory environment, banks have been forced to de-lever and can no longer take advantage of low funding costs as they once could.

While banks now account for close to 50% of total aggregate financial assets in Europe, there are still several major economies where banks account for more than 60% of total financial assets (including Germany, France, Italy, and Spain). Moreover, at more than 100%, the aggregate loan-to-deposit ratio in Europe is still well above the global average of approximately 80%.

To date, the primary channels of financial disintermediation have been renewed growth in the corporate bond market and a transfer in assets to non-bank entities. The European Central Bank is currently attempting to jumpstart the private ABS market, which would provide further support.

To put the upside in perspective, total bank disintermediation would surpass $1 trillion (USD) if the bond market grew from 20% to 30% of non-financial corporate funding (versus 70% in the U.S.), the RMBS market matched the size of the private label U.S. market (approximately 8%) and the ABS market grew to about 5% of non-financial corporate funding (versus more than 7% in the U.S.). In our view, key beneficiaries of financial disintermediation in Europe are the investment banking, private equity and asset management industries.

Financial disintermediation has developed a bad reputation over the past few years between the global financial crisis and growing concerns regarding the exponential growth in the Chinese shadow banking system, but if properly regulated and monitored, it should benefit the overall economy by lowering financial costs through increased competition.

Conclusion

Over decades, the disintermediation of the financial system could contribute to a more stable global economy, with risk dispersed across more companies and a reduction in the number of “too-big-to-fail” silos—that is, to the extent that capital markets are transparent and well regulated. Indeed, while financial disintermediation is clearly a strong secular theme that provides tailwinds in several financial industries, it’s likely to be a long and volatile process, complicated by ongoing regulatory and litigation risks. We believe that our disciplined focus on both risk and reward should continue to serve us well in this environment.

Asset-Backed Security (ABS) refers to a financial security backed by a loan or receivable against assets excluding real estate and mortgage-backed securities. Residential Mortgage- Backed Security (RMBS) is a financial security consisting of a pool of residential mortgage loans created by financial institutions. Hong Kong Exchanges and Clearing Limited (HKEx) operates a securities market and a derivatives market in Hong Kong and the clearing houses for those markets. Loan-to-deposit ratio is a measure of a bank’s liquidity. A high ratio indicates banks might not have enough liquidity to cover unforeseen requirements. A low ratio indicates banks might not be earning as much as they potentially could be.

© 2015 Calamos Investments