The policymaking arm of the Federal Reserve (Fed), the Federal Open Market Committee (FOMC), will hold its second of eight meetings of the year this week (March 16–20, 2015) amid a near historic run-up in the value of the U.S. dollar versus the currencies of our major trading partners and the continuing collapse in oil prices. (For more on the impact of the dollar on the U.S. stock market, see this week’s Weekly Market Commentary, “Dollar Strength Is a Symptom, Not a Cause.”) What the FOMC says, if anything, about the rising dollar—and its implications for the U.S. economy, labor market, and inflation—could have ramifications for monetary policy over the next several quarters and beyond.

Will the fomc remain “patient”?

On Wednesday, March 18, 2015, at the conclusion of the two-day meeting, the FOMC will release a statement as well as a new economic and interest rate forecast. In addition, Fed Chair Janet Yellen will conduct her first post-FOMC meeting press conference of the year. With quantitative easing (QE) over—the FOMC made its final purchases of mortgage-backed securities (MBS) and Treasuries in October 2014—financial market participants are now focused intently on the timing of the first Fed rate hike. Matching our own long-held view, financial market participants expect the first Fed rate hike to occur in the final months of 2015, but that view may change if the Fed alters its promise to be “patient” in beginning to raise rates.

If the FOMC does remove “patient” from the statement, it may choose to replace that word with a similar word or set of words, as it did during the run-up to the first rate hike of the 2004–2006 rate hike cycle. We also continue to expect the FOMC to tie the first rate hike to the performance of the economy, in particular, the labor market and inflation. Fed officials refer to this concept as “data dependence.” In recent public appearances, including her semiannual monetary policy testimony to Congress in mid-February 2015, Fed Chair Yellen has noted that while the labor market appears to be on course, inflation continues to run well below the Fed’s 2.0% target. The stronger dollar, all else equal, will push down on inflation, and although there is a high hurdle for the Fed to mention the dollar or other international considerations in its FOMC statement, it may warrant a mention.

The FOMC will also provide markets with a new set of targets at this meeting, as it does four times a year. The FOMC’s new forecast for gross domestic product (GDP), the unemployment rate, inflation, the appropriate timing of the first rate hike, and the so-called “dot plot” (the appropriate level for the fed funds rate at year-end in 2015, 2016, 2017, and in the “longer run”) will be scoured by market participants looking for clues as to how the FOMC’s own economic forecast has evolved since the last forecast was released in December 2014. The dot plot, in particular the level of the fed funds rate the FOMC sees in the “longer run,” may play an important role in this week’s meeting if the committee does remove the word “patient.”

Shifting from “when” to “how much and how fast”

Markets have been focused on when the first rate hike will be, and because the Fed has not started a rate hike cycle in 11 years, the “when” is certainly important. But markets have spent less time focusing on “how much” rates will move up and “how fast” they get there, and those questions are likely to become increasingly important to markets, corporations, and households once the Fed makes it clear when rates will begin to move higher. The dot plots currently place the fed funds rate in the “longer run” at 3.75%. That’s important because the December 2014 FOMC statement said the following:

“The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.”

We expect that the statement following this week’s meeting will retain similar language, and that financial markets will continue to expect a gradual trajectory for rate increases once the Fed starts raising rates (so called “lift-off”). Currently, financial markets expect a fed funds rate of just 2.0% by early 2018, about 175 basis points (1.75%) below where the FOMC dot plots put the fed funds rate in the “longer run.” The current disconnect on the “how much” and “how fast” between the FOMC and the financial markets—and how it ultimately gets resolved—could be a major issue for financial market participants in the months ahead. We’ll be watching it closely.

Factors we are watching to gauge when the fed may raise rates

We have included several charts in this week’s commentary aimed at gauging “when” the Fed may begin to raise rates. The charts extend back to the early 1980s, and cover five Fed rate hike cycles (shaded areas on charts indicate Fed tightening periods):

· Mid-1980s

· Late 1980s

· Mid-1990s

· Late 1990s

· Mid-2000s

The charts are measures of wages and inflation mentioned by Fed Chair Yellen or Fed staffers in the past six months or so and include:

· Average Hourly Earnings [Figure 1]

· Employment Cost Index—Total Compensation [Figure 2]

· Output Gap [Figure 3]

· Personal Consumption Deflator [Figure 4]

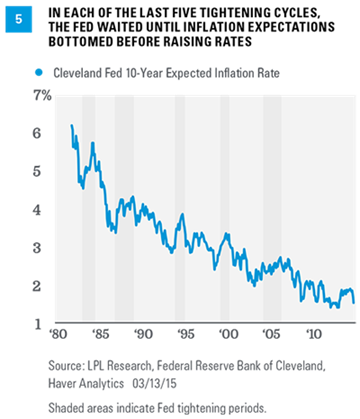

· Cleveland Fed Inflation Expectations [Figure 5]

Our initial intention was to identify a common set of conditions in each (or at least most) of these metrics to focus on the “when.” What we found, however, was that each Fed rate hike cycle is unique (economic and policy backdrop, labor market, inflation, external conditions, etc.), making it difficult to draw a specific conclusion such as: “The Fed always begins to hike rates when economic data point x crosses level y.” Instead, we can only draw very broad conclusions about when the Fed begins to hike rates. Looking at wages [Figures 1 and 2], the Fed generally does not begin to hike rates until after a definitive bottom in measures of wages has been made, although there are some exceptions to this. Currently, while average hourly earnings have not yet put in a definitive bottom, the Employment Cost Index (ECI) looks to have bottomed out.

There is no clear, consistent relationship between the output gap (see our Weekly Economic Commentary, “Mind the Gap,” September 22, 2014) and the onset of Fed rate hikes [Figure 3]. Often, the Fed has waited until the output gap has bottomed out, but not always. In the late-1990s cycle, the output gap had been narrowing for nearly 10 years before the Fed tightened. Today, the output gap has been narrowing for five years, but remains well below the level at which the Fed began tightening in prior cycles, except the one that began in the mid-1980s.

Figure 4 shows overall inflation and Fed rate hike cycles. While we didn’t include a chart here, the Fed also watches inflation excluding food and energy (core) closely as well, which makes sense, since over time, core inflation tracks headline inflation. As is the case with wages and the output gap, there is no clear “trigger” point for Fed on inflation. Since the early 1980s, when the Fed was tightening as inflation was still falling, the Fed has waited until inflation had bottomed before raising rates. However, the time between a clear bottom in inflation and the first hike has varied widely. Today, inflation is still falling and the Fed may want to see it accelerate for at least a few months before raising rates.

Figure 5 is the Cleveland Fed’s measure of inflation expectations. It captures inflation expectations from professional forecasters, the public at large, and market-based measures of inflation expectations. The issue here is that both inflation and inflation expectations have been in a downward trend since the early 1980s. However, a closer look at this figure does reveal that in each of the last five tightening cycles, the Fed did wait until after this measure of inflation expectations bottomed before raising rates. Currently, it appears that inflation expectations are still in free fall, and the Fed will likely want to see this decline halt and reverse course before hiking rates.

On balance, the market has been more focused on the “when,” and given that it has been 11 years since the Fed last initiated a tightening cycle, that focus is warranted. However, once the “when” is out of the way, market participants may ultimately focus attention on the “how much” and “how fast.”

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.Mortgage-backed securities are subject to credit, default, prepayment risk that acts much like call risk when you get your principal back sooner than the stated maturity, extension risk, the opposite of prepayment risk, market and interest rate risk.

DEFINITIONS

The Employment Cost Index (ECI) measures the change in the cost of labor, free from the influence of employment shifts among occupations and industries, and is published by the Bureau of Labor Statistics.The Output Gap represents the difference between the actual output of an economy and the output it could achieve when it is most efficient, or at full capacity, as measured by real and potential GDP.Personal consumption expenditures (PCE) is a measure of price changes in consumer goods and services. Personal consumption expenditures consist of the actual and imputed expenditures of households; the measure includes data pertaining to durables, nondurables, and services. It is essentially a measure of goods and services targeted toward individuals and consumed by individuals.

(c) LPL Financial