The massive U.S. dollar rally has wide-ranging impacts. It hurts international stock returns generated in foreign currencies. It influences global trade and the flow of investment dollars. A strong dollar hurts corporate earnings by reducing revenue earned by U.S.-based multinationals overseas in foreign currencies. It even puts downward pressure on inflation and commodity prices (including oil) and can influence monetary policy, corporate profit margins, and consumer spending.

These are important considerations, but the key question investors are asking is whether the strong dollar will derail the bull market. We don’t think so, based on how stocks have done historically during strong dollar periods. But the dollar does have important implications for asset classes and sectors, as we discuss below.

IS THE STRONG DOLLAR BAD FOR STOCKS?

We can certainly understand why market participants and the media are so focused on the dollar. Its ascent has been steep and its implications are wide ranging. In our January 26, 2015, Weekly Market Commentary, “No Deflating the U.S. Dollar,” we highlighted some of the reasons for recent dollar strength, including relative economic performance, relative interest rates, and monetary policy differences, among others. These factors all contribute to the outlook for the economy and corporate profits and help determine stock market direction. The dollar itself, however, is not a key driver of market performance – it is a symptom.

There is a fundamental link between the dollar and corporate profits. However, even though a rising dollar is a drag on earnings, generally the market looks past short-term currency fluctuations and evaluates companies’ longer-term, sustainable earnings power. Historically, based on the past four decades, as the dollar weighs on earnings, stocks tend to hold their value or rise, and valuations tend to increase. For example, during the latest leg up in this bull market since October 2014, the strong dollar has dragged earnings estimates down, while the stock market has risen, resulting in higher valuations.

Stocks have historically performed very well after strong gains in the dollar. When the dollar is higher over a one-year period, the S&P 500 is up an average of 11.2% over the following year and is higher 75% of the time (data back to 1980). For stronger gains in the dollar, stocks on average have done even better historically, as shown in Figure 1. So does that mean buy stocks just when the dollar is rising? Not necessarily. Stocks are up nearly as much when the dollar is down, as Figure 1 also shows.

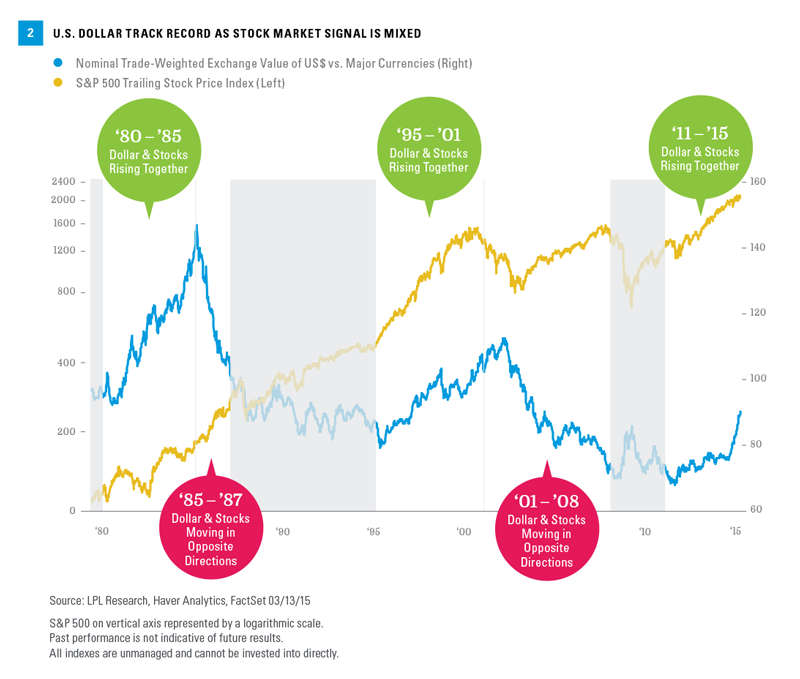

Another way to show the mixed relationship between the dollar and the stock market is to plot them both on the same chart. We did this in Figure 2, where you can see that over the past four decades stocks rose during some rising dollar periods (such as the late 1990s tech boom, which attracted foreign investment and overlapped with emerging markets currency crises) and some falling dollar periods (such as the mid-2000s when global capital was attracted to the boom in emerging markets). Bottom line, although quantitative easing is an unusual monetary policy for central banks, the current period with the stock market and the U.S. dollar rising together is not unusual; thus, we do not view the strong dollar as a reason to turn more cautious on U.S. stocks.One takeaway here is that the dollar is not necessarily connected to the macroeconomic cycle, partly because it can be driven by so many different factors. Stocks can do well when the dollar is up strongly or down strongly. Accordingly, the dollar is not a useful tool for guiding decisions on buying or selling stocks.

Although it is not clear whether a rising or weakening dollar is better for the stock market, we have found some interesting sector relationships. We have sector data covering the two dollar bull markets since 1990 (late 1990s and 2010s) and the dollar bear market during the 2000s, and although the sample size is very small, the following sectors have logical relationships with the U.S. currency:WHAT’S WORKED IN DOLLAR BULLS

· Commodity sectors: May favor falling dollar. Energy was the top-performing sector during the U.S. dollar bear market in the 2000s, while the materials sector was second. Conversely, these two sectors were among the worst performers during the late 1990s and current bullish dollar periods.

· Consumer discretionary: May favor rising dollar. The sector is more domestically focused and tends to be inversely correlated to energy, which makes sense given how much consumers spend on gasoline. Consumer goods companies also import a lot of stuff from overseas and benefit from sourcing products in weaker currencies.

· Financials: May favor rising dollar. Financials performed much better during the two dollar bull markets than the one dollarbear market since 1990. The economic cycle had more to do with the performance than interest rates, but the sector’s more domestic focus was likely also a factor in the better strong dollar performance.

As with the more domestic-focused sectors, it would seem to follow that the more domestic-focused small caps would perform better than more global large caps during periods when the dollar is rising. Interestingly, a look at performance by market cap during these dollar cycles reveals a mixed relationship, suggesting it is important to consider a broader set of factors when making these allocation decisions.

During the rising dollar periods:

· Small caps outperformed during the early 1980s dollar bull market.

· Large caps outperformed during the late 1990s dollar bull market.

· Large caps have outperformed during the strong dollar period since 2011.

During the falling dollar periods:

· Large caps outperformed during the falling dollar period of the late 1980s.

· Small caps outperformed during the dollar’s decline in the 2000s.

CONCLUSIONAlthough the strength of the dollar has important implications, it is more of a symptom of economic and market forces rather than a cause of them. Although some sector relationships are interesting, the dollar is not very useful as a predictor of stock market performance and we do notexpect it to derail this bull market.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5013 0315 | Tracking #1-364110 (Exp. 03/16)