When the euro was introduced as an accounting currency on Jan. 1, 1999, it declined quickly, depreciating by 14.7 percent by Dec. 31 and hitting parity with the dollar early in 2000 before plunging to $0.83 by October of the same year. The euro’s recent slide has been no less severe, falling by 21 percent against the dollar since July of last year. With parity once again within sight, it seems quite plausible that one euro will once again equate to one dollar, and could potentially head even lower.

Of course, the biggest beneficiary of the depreciating euro has been Europe itself. Economic data coming out of the euro zone has been decent of late, and economic sentiment in Germany remains at a high level. The ZEW index of economic expectations for Germany, although perhaps tempered slightly by concerns over Greece and Ukraine, still rose to a reading of 54.8 for March, up from 53 the previous month and the highest level since February 2014. Meanwhile, European equities are being powered higher—on Monday, Germany’s DAX Index breached the 12,000 barrier for the first time and is now trading at just above that level—and euro zone consumer confidence is at levels last seen in 2007.

In contrast to the party spirit emanating from Europe, the U.S. economy faces some tough sledding in the weeks ahead, although not so much that it prevented the Federal Reserve from removing the word “patient” from its March meeting statement, signaling that there is enough strength in the economy for the Fed to start raising rates, most likely in September. In the short-term, temporary seasonal factors will likely tarnish investors’ faith in the economy. This seasonal downturn is not lost on the Fed. In the Federal Open Market Committee’s March meeting statement, it changed its description of economic growth from “has been expanding at a solid pace” to “has moderated somewhat.”

While U.S. job growth has been impressive, retail sales were weaker than expected, with last week’s sales print again coming in below expectations. But weak, weather-distorted first-quarter data is nothing new, and should not be taken as a sign of lasting weakness. In the early months of 2014, key economic data points, such as housing, retail sales, and even employment, were negatively impacted by an extended winter cold snap. Indeed, the U.S. economy shrank by 2.1 percent in the first quarter of 2014 before promptly turning back around in the second quarter. I expect a similar scenario to play out in 2015 as a result of another severe winter season.

The most likely place where we will see the direct impact of weaker economic data is the bond markets. Yields on U.S. 10-year Treasuries could fall meaningfully from 1.93 percent, perhaps even making a run on the lows we saw in January, with investors likely to be spooked by weaker economic data as the current quarter progresses. Personally, I have a great deal of confidence that the U.S. economic recovery remains on track and I don’t see weather-related economic data distortions having a lasting impact on the real economy. The prospects for U.S. equities and credit remain strong this year and recent weakness represents a buying opportunity.

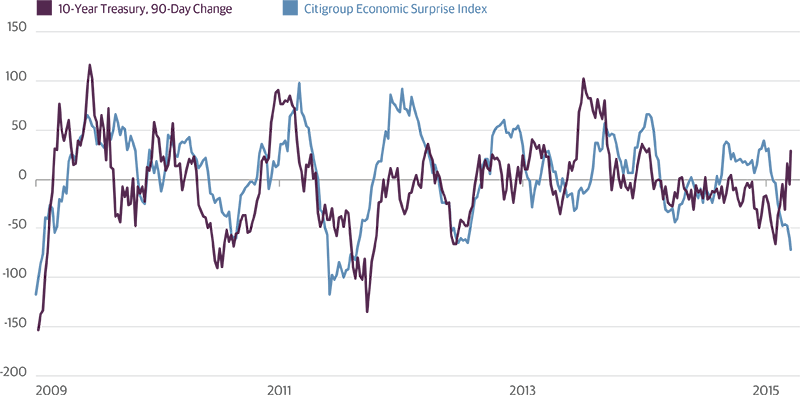

Tough Sledding: Winter Weather Could Weigh on Interest Rates

As it did last winter, recent economic data has surprised to the downside as a result of severe weather. Retail sales have fallen the past three months, housing starts plunged 17 percent in February, and consumer confidence has backed off its recent highs. With economic momentum temporarily slowing, the Fed signaling the possibility of a later rate hike, and capital continuing to pour in from overseas, U.S. Treasury yields could be headed lower in the near term.

Change in 10-Year Treasury Yield (bps) and Citigroup Economic Surprise Index

Source: Bloomberg, Citigroup, Guggenheim Investments. Data as of 3/18/2015.

Economic Data Releases

Weather Weighs on February Housing Starts

- Housing starts plunged 17 percent in February, down to an annualized pace of 897,000, the lowest in over a year. The decline was likely attributable to winter weather.

- Building permits painted a more upbeat picture for housing, rising 3 percent, the best monthly gain since last October.

- The NAHB Housing Market Index fell slightly in the March reading, down to 53 from 55. The future sales sub-index was steady.

- Industrial production was under expectations in February, inching up just 0.1 percent. January’s figure was also revised to show a 0.3 percent decline.

- The University of Michigan consumer sentiment index fell to 91.2 in March, shy of forecasts and down from 95.4 a month earlier. Expectations for future economic conditions slipped from 88 in February to 83.7.

- Initial jobless claims were mostly unchanged for the week ending March 14, inching up to 291,000 from 290,000.

- The Leading Economic Index rose for the 13th straight month in February, up 0.2 percent. Seven out of 10 indicators were positive.

Confidence Continues to Improve in the Euro Zone

- The euro zone February Consumer Price Index was unchanged in the final reading at -0.3 percent, while core CPI was revised up to 0.7 percent.

- Germany’s ZEW survey improved in March, with the current situation index jumping to 55.1 from 45.5, and expectations rising to a 13-month high.

- The unemployment rate in the U.K. was stable at 5.7 percent in January.

- Japanese export growth slowed in February, rising 2.4 percent from a year ago while imports were lower on a year-over-year basis.

Important Notices and Disclosures

This article is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.

©2015, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.