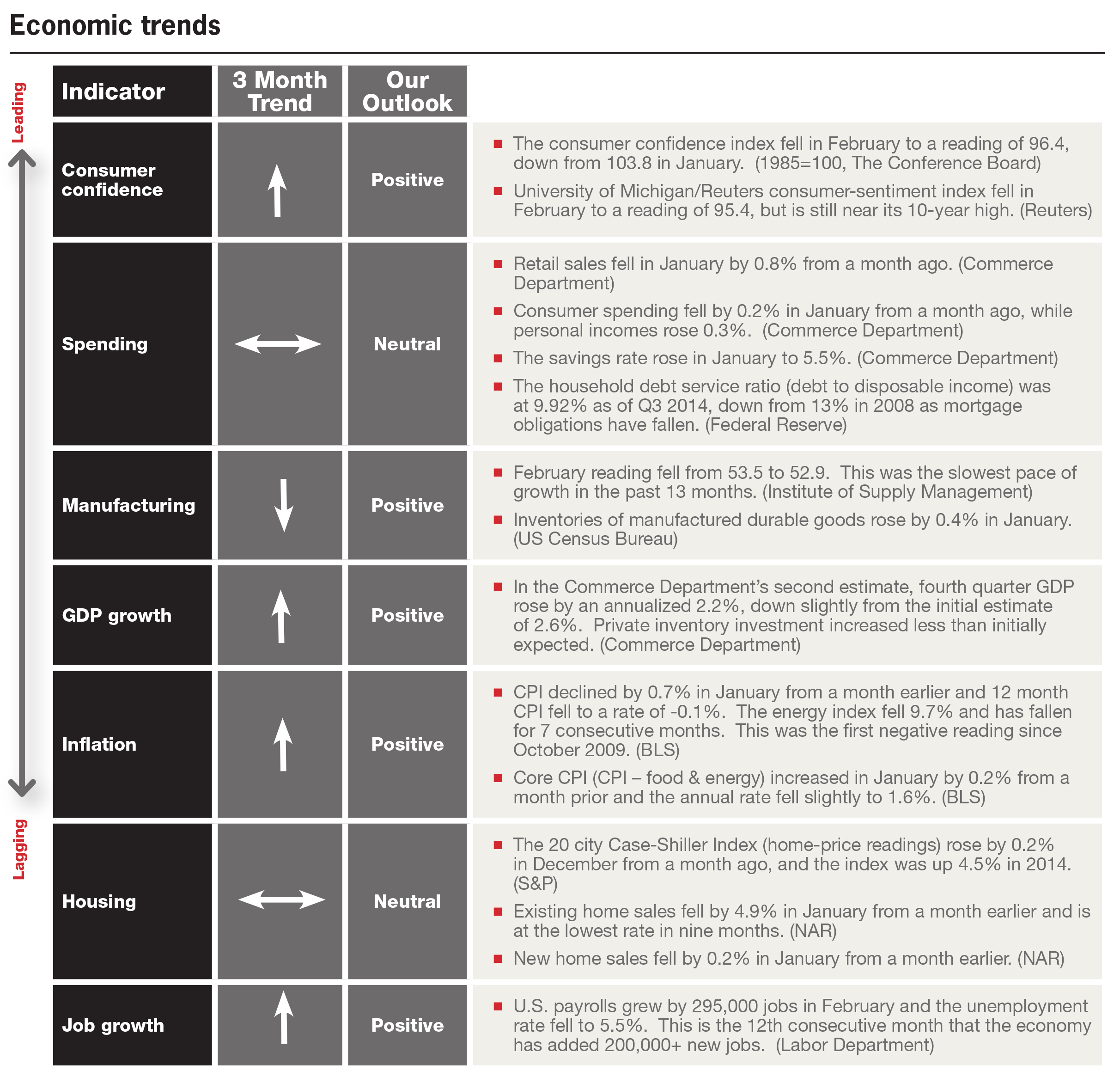

The economy

U.S. economy back at “full” employment

With the unemployment rate dropping to 5.5% in early March, the economy has reached the upper limits of the Federal Reserve’s estimate of long-run normal unemployment (5.2% - 5.5%). GDP growth remains stable, with a current estimate of 2.2% growth for the fourth quarter of 2014. The housing market recovery continues at a slow-but-steady pace, with prices rising twice as much as inflation during 2014 (+4.5%) according to the 20 city Case-Shiller Index. The most uncertain aspect of the economic recovery in the U.S. remains the consumer. Confidence is high, but wage growth has been slow and spending has dropped in recent months. Lower spending can be explained by lower gas prices, but also indicates that consumers are saving the extra money in their budget instead of spending it. While this may be the right choice at the individual level it does have a negative impact on the economic growth, as approximately two-thirds of gross domestic product is generated by consumers. All things considered, the U.S. economy appears to be on solid footing.

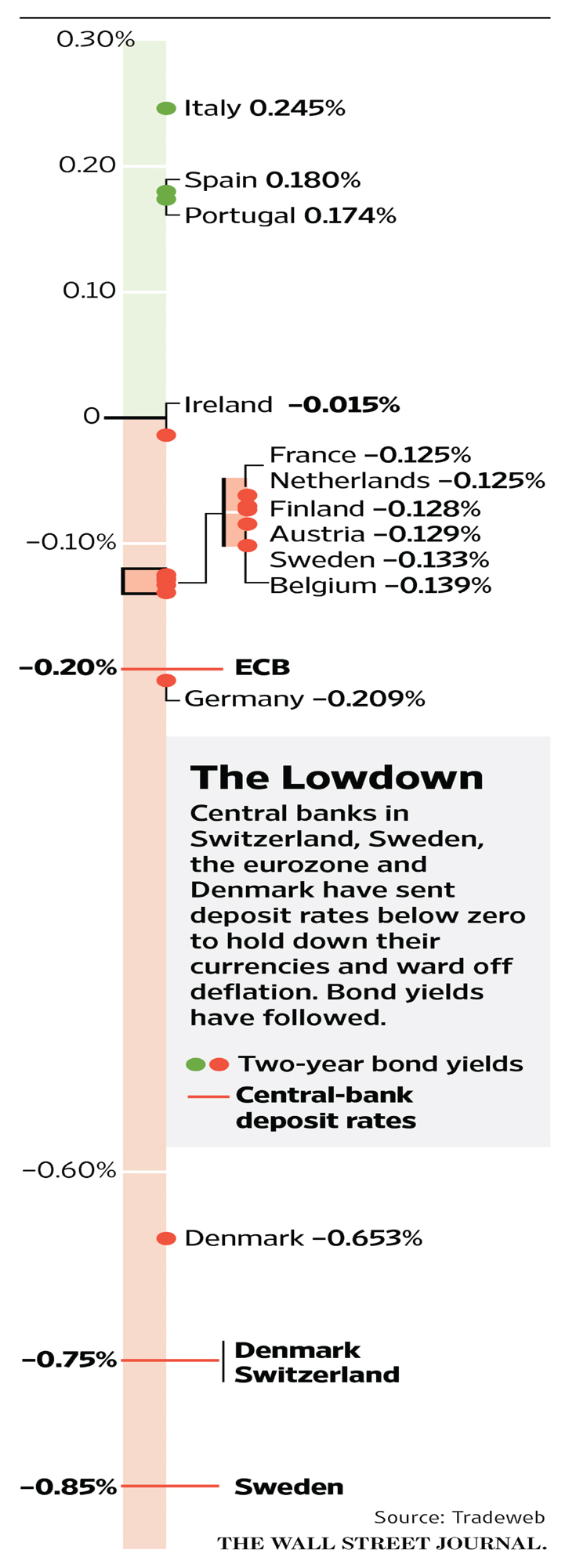

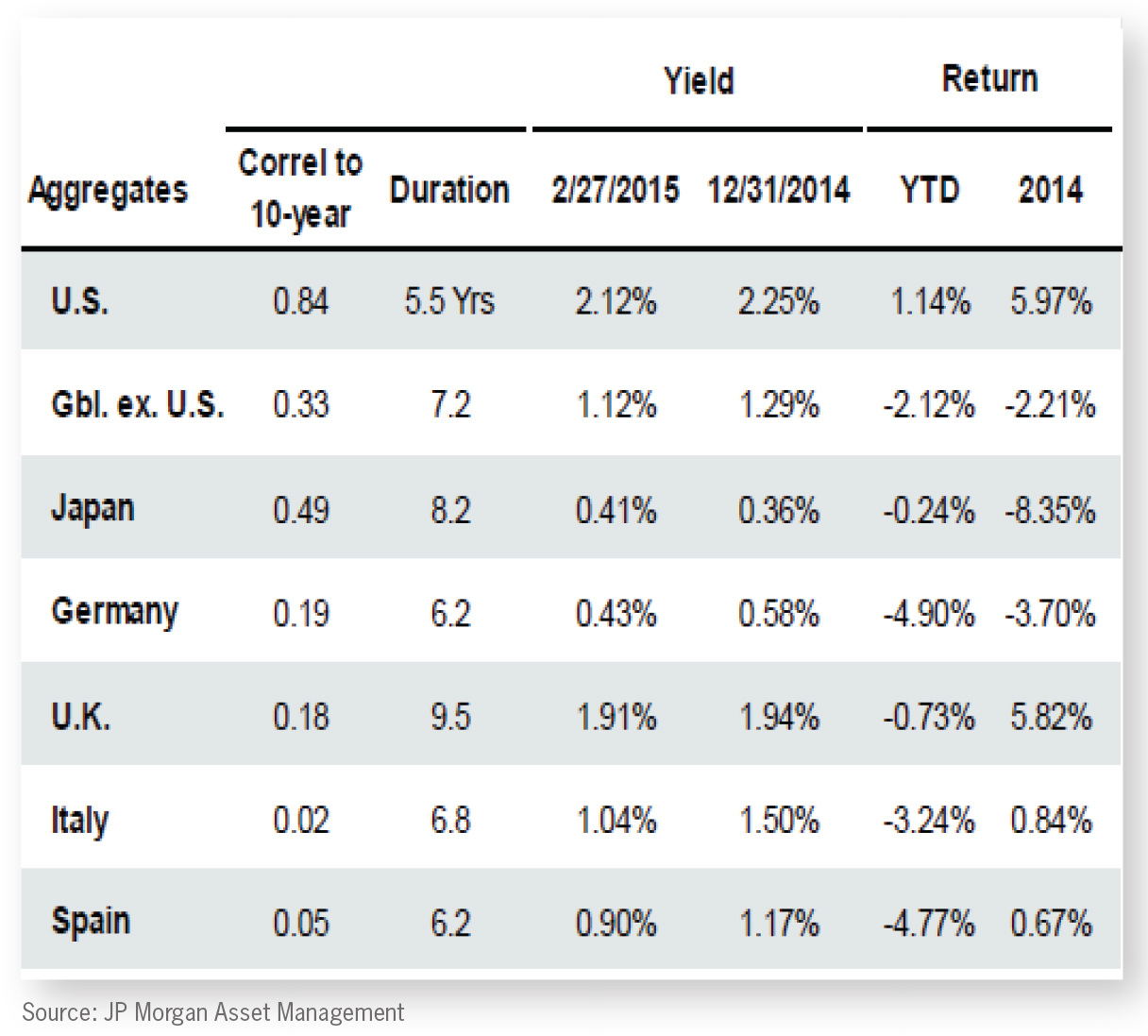

The bond market

Interest rates back to year end levels

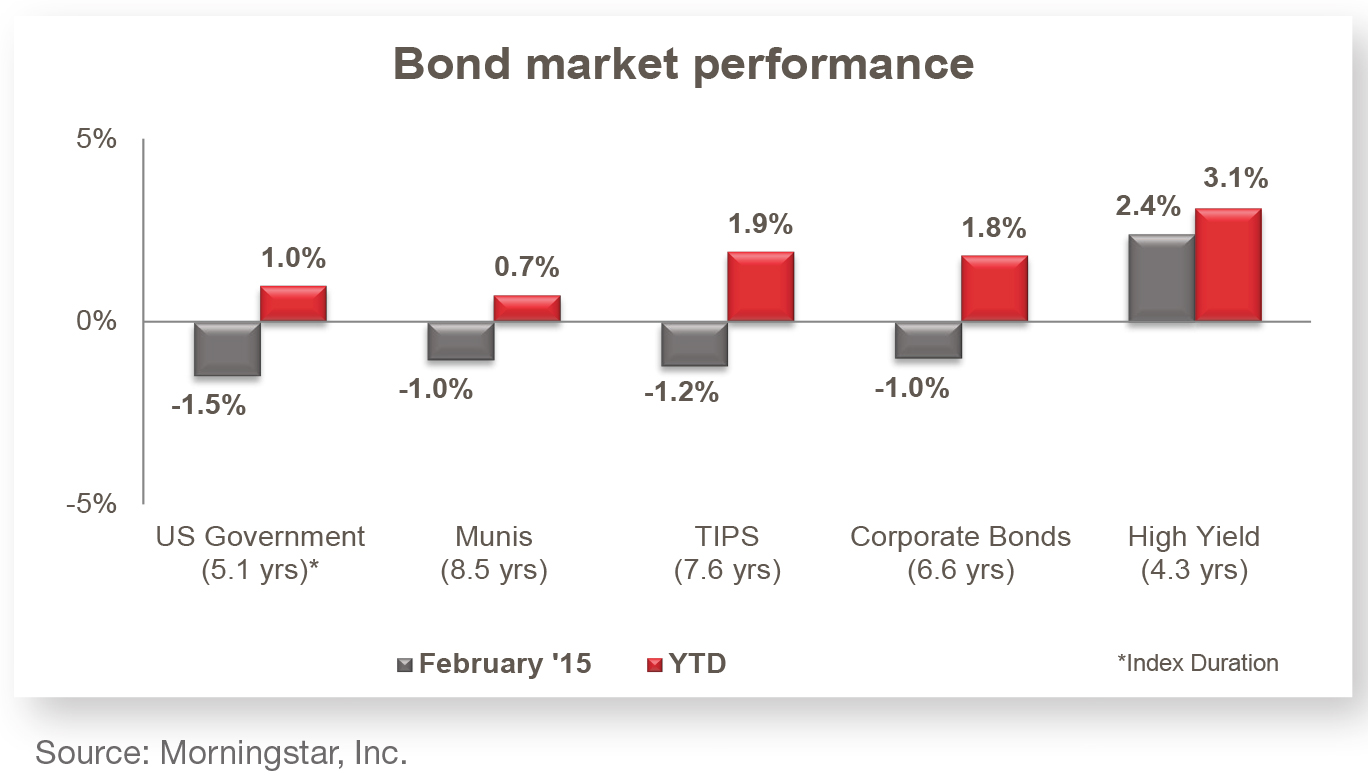

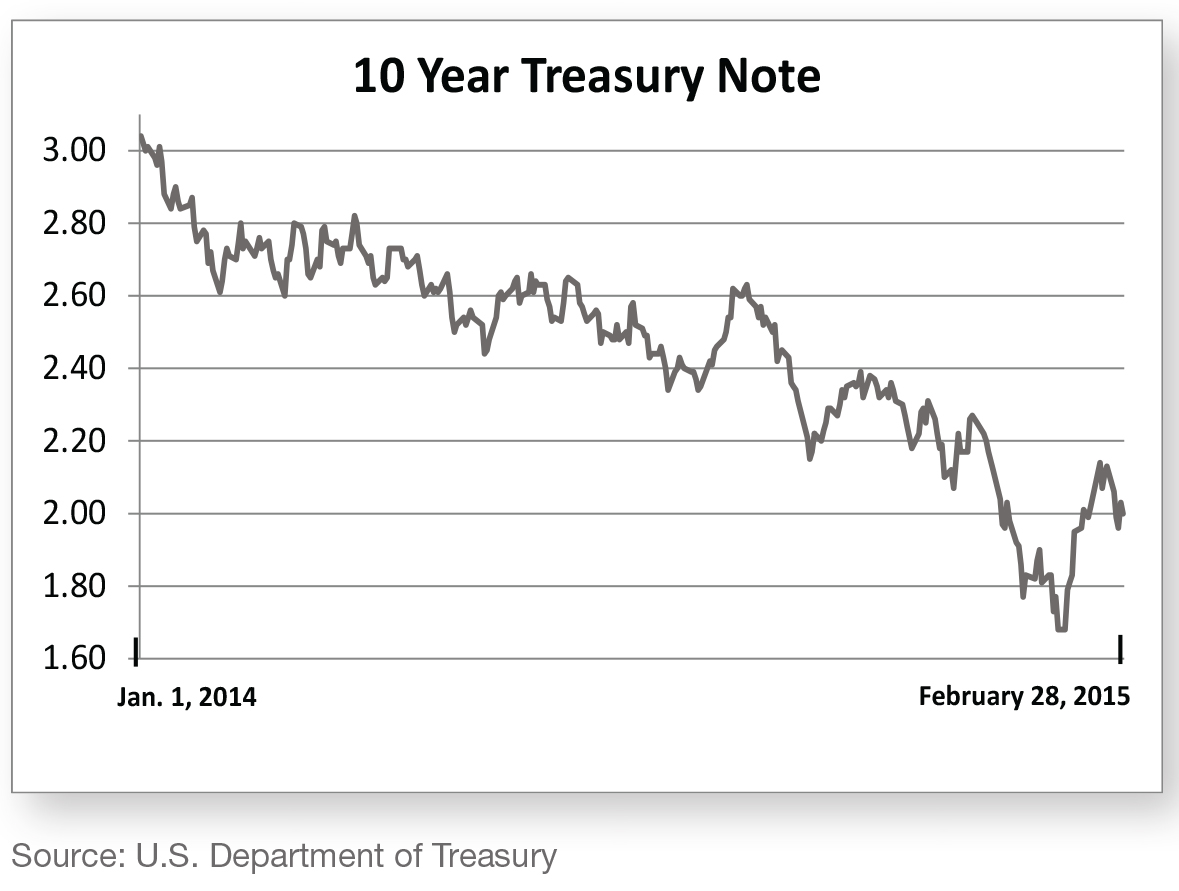

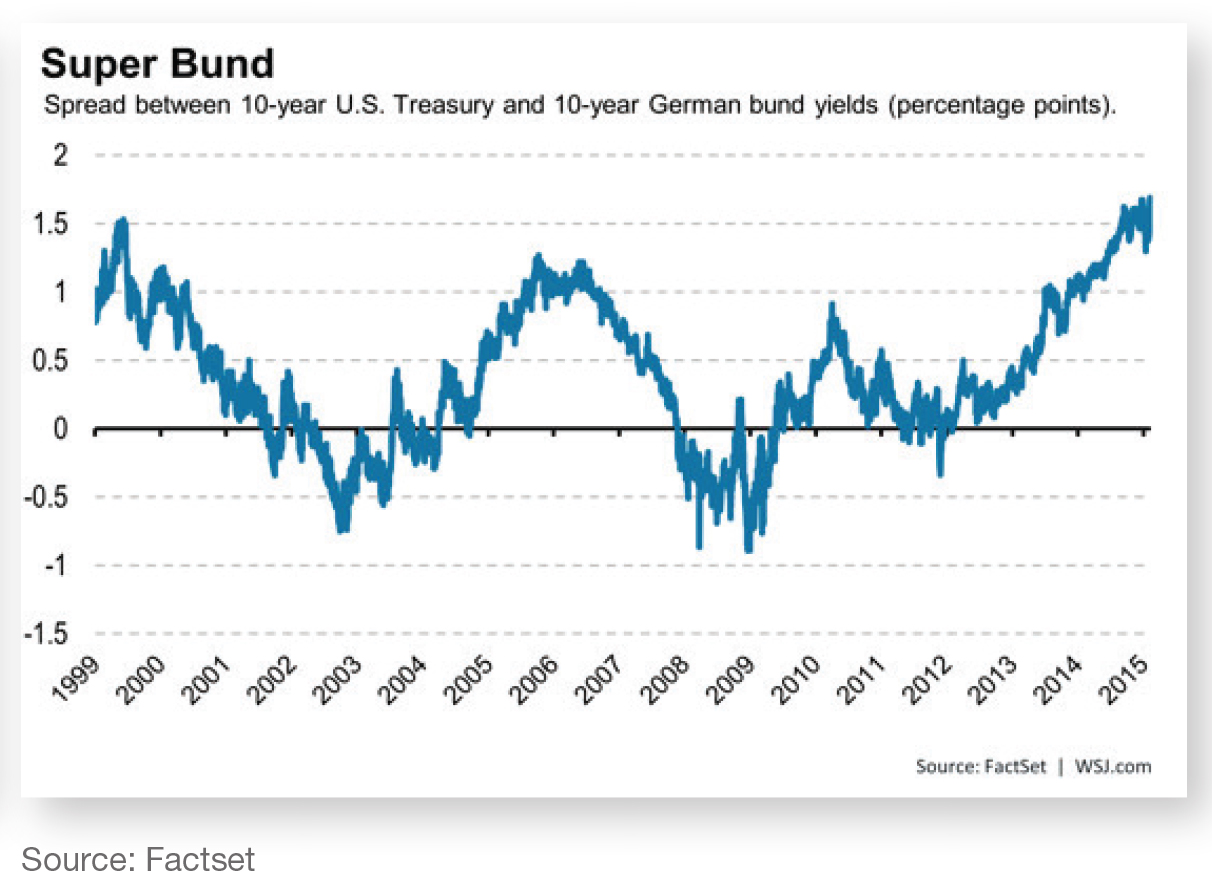

After an initial drop during January interest rates have bounced back to beginning-of-year levels, putting pressure on fixed income investments. Investors have begun reacting in anticipation of the Federal Reserve raising interest rates in the second or third quarter of the year. While the effects of these expectations may play out on the short end of the yield curve, longer-dated bonds should continue to be driven by supply and demand. With global interest rates well below those in the U.S., we believe there will be continued ample demand for U.S. debt. Much like quantitative easing in the U.S., the European Central Bank’s new bond buying program should suppress yields throughout the Eurozone.

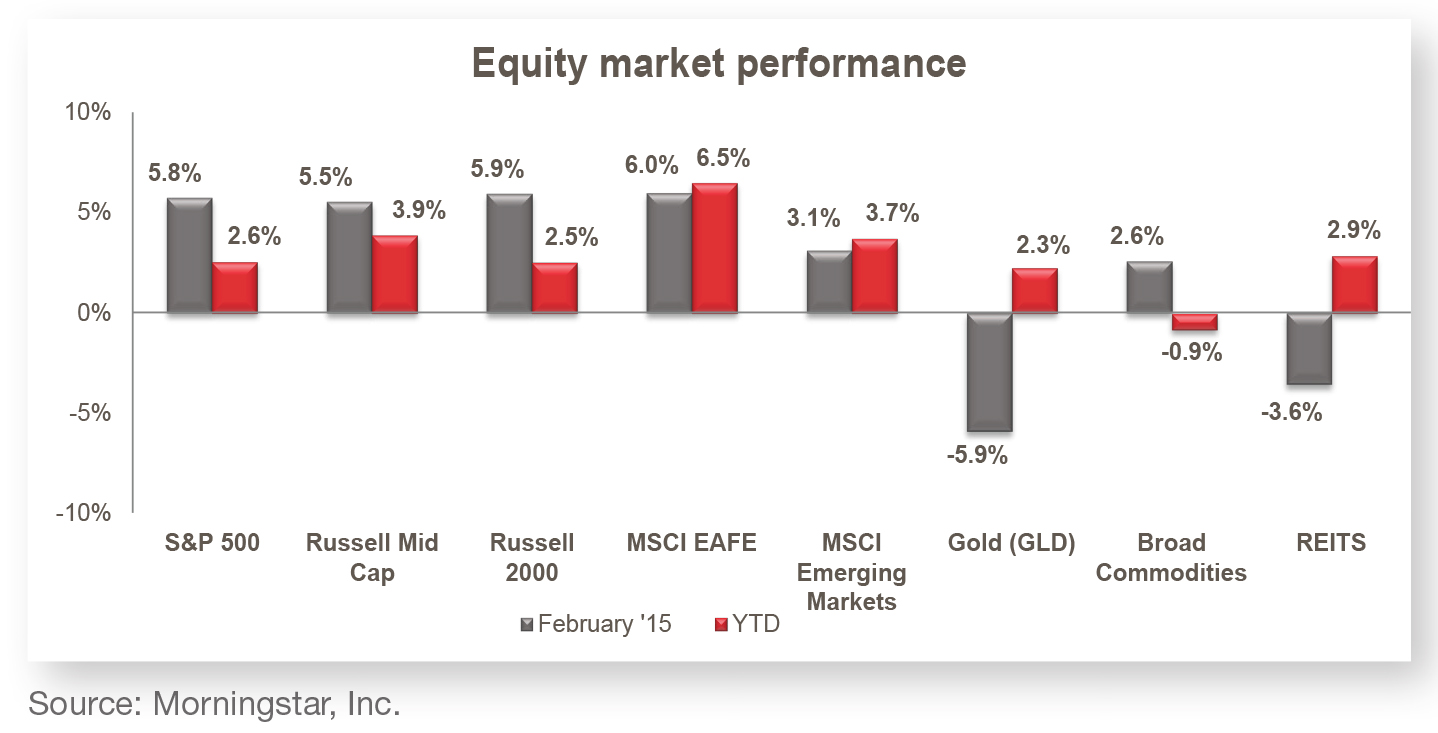

The stock market

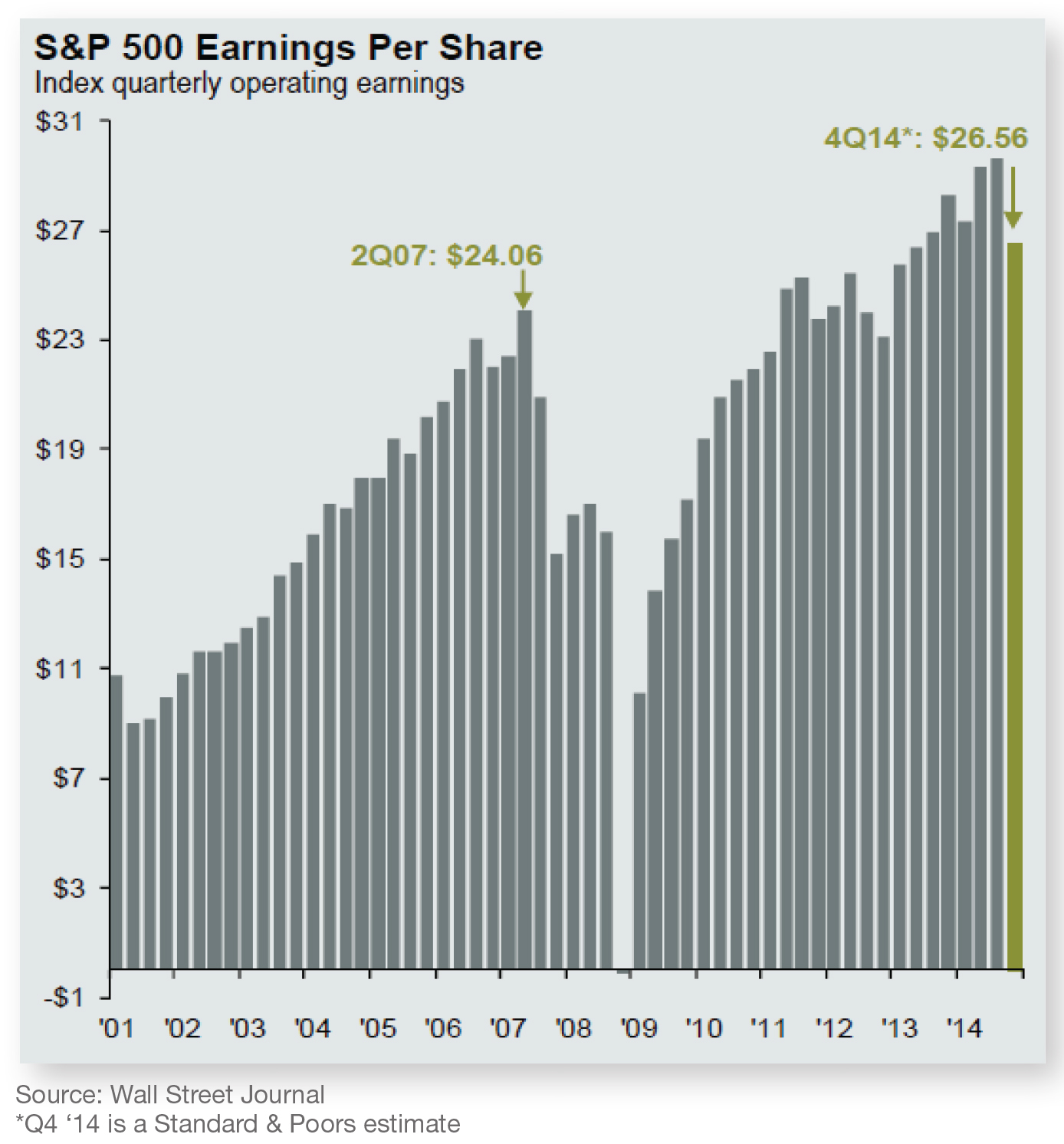

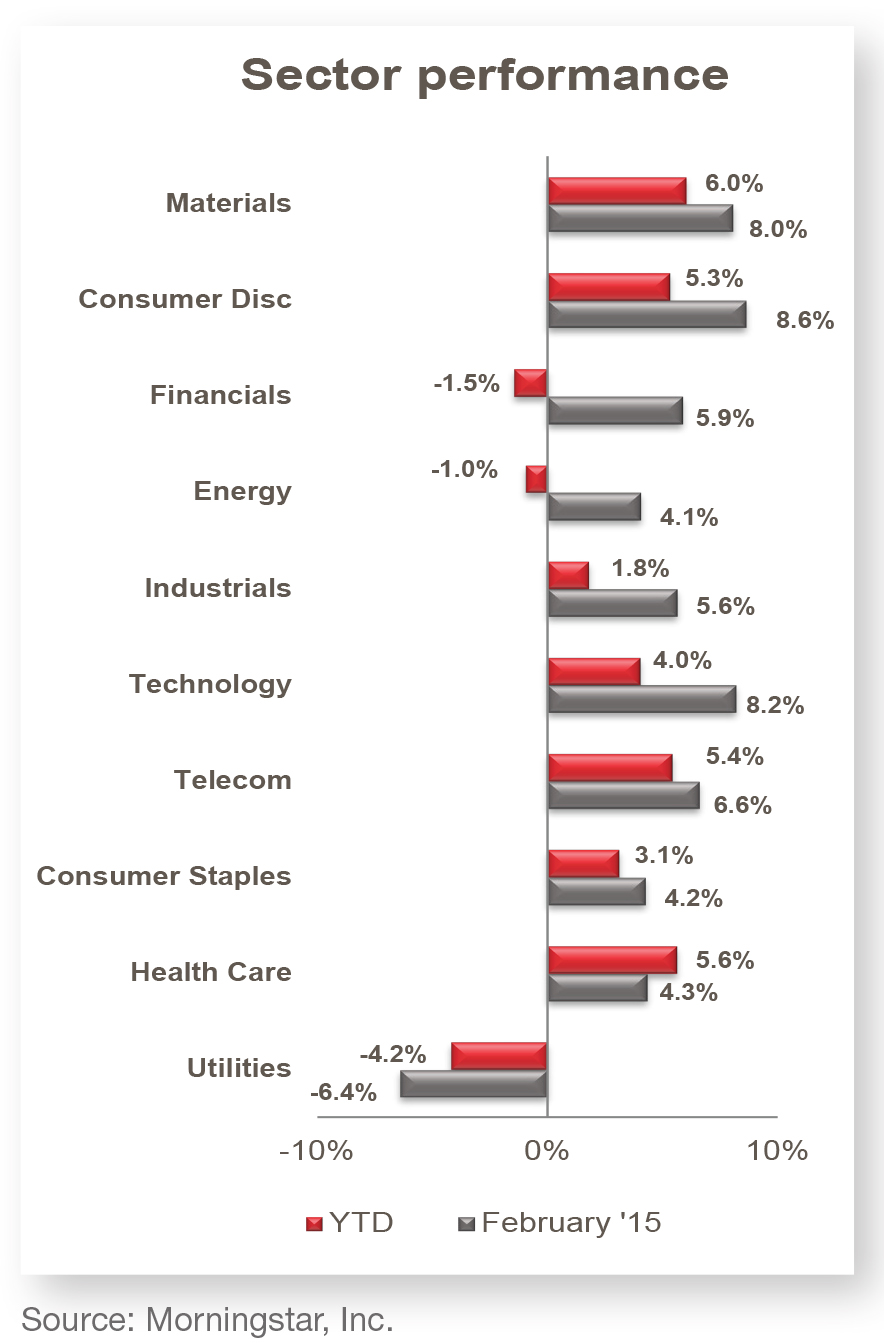

Stocks bounce back into positive territory

Stock market volatility continued during the month of February, but this time to the up side. U.S. and international developed markets rose nearly 6% during the month and are well into positive territory for the year. The value of the Euro against the U.S. dollar fell to near a 12-year low in early March, which had contributed to the underperformance of foreign investments in late 2014. Forward looking valuations for the S&P 500 Index are now slightly above the 25-year average, but strong earnings and a growing economy provide a solid backdrop for these levels. The U.S. large cap market has evaded a 10% correction for three calendar years in a row. A correction of this magnitude has historically occurred annually. With stocks reaching record levels and consumer confidence at 10-year highs, it would not be surprising to see the recent volatility continue as investors assess positive economic reports and future Federal Reserve policy.

|

Indexes |

YTD |

Treasury yields |

||||

|

Stock indexes |

Prime rate |

3.25% |

6-month |

0.07% |

||

|

Dow Jones |

18,133 |

2.21% |

LIBOR rate (3 mos.) |

0.26% |

1-year |

0.22% |

|

S&P 500 |

2,105 |

2.58% |

Unemployment rate |

5.50% |

2-year |

0.63% |

|

NASDAQ |

4,964 |

5.02% |

15-year mortgage rate |

3.17% |

5-year |

1.50% |

|

Bond indexes |

30-year mortgage rate |

3.91% |

10-year |

2.00% |

||

|

Broad Market Barclays Agg |

1.14% |

CPI (12-mo. ending 1/31/2015) |

-0.10% |

30-year |

2.60% |

|

|

US Corporate Barclays Capital |

1.81% |

GDP (fourth quarter 2014) |

2.20% |

|||

|

US Government Barclays |

0.98% |

Oil price (price/barrel) |

$49.76 |

|||

|

Mortgage-Backed Barclays |

0.85% |

Gold (oz.) |

$1,213 |

Disclosure:

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2015 Bronfman E.L. Rothschild, LP