In technical analysis, “intermarket analysis” looks at the way in which various markets interact. Intermarket analysis primarily looks at four market sectors: currencies, commodities, bonds, and stocks. From a technical analyst’s perspective, focusing our attention on only one market without considering what’s happening in the others leaves us in danger of missing vital directional clues and potential profits. The dollar, which has appreciated 24.4% since June 30, 2014 (as of March 19, 2015), has had an unusually strong intermarket effect of late. Today, we look at the dollar’s recent impact on other major markets and what it means for investors from a technical perspective. Since June 2014, a strong U.S. dollar has created a tailwind for European equities, while creating headwinds for the euro and commodities, especially crude oil, as well as equity markets for commodity-exporting emerging market countries such as Brazil. (To read about the dollar’s impact on domestic equity markets, see the March 16, 2015, Weekly Market Commentary, “Dollar Strength Is a Symptom Not a Cause.”)

CURRENCY RIPPLE EFFECTS

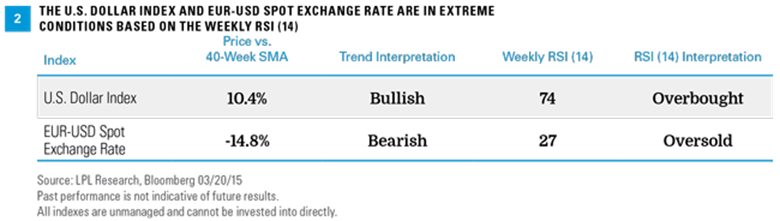

The strength or weakness of the U.S. dollar, as measured by the U.S. Dollar Index, is determined by the dollar’s value against a basket of major world currencies. As of March 19, 2015, the euro made up 57.6% of the U.S. Dollar Index. A strong dollar, therefore, generally corresponds to a weak euro. Technically, the U.S. Dollar Index has been operating in a bullish price trend, as represented by a positively sloping 40-week simple moving average [Figure 1]. The magnitude of its price move higher since July 2014 may be considered substantial, reflected by a weekly 14-period relative strength index (RSI [14]) value of 74 [Figure 2]. The RSI (14) is a technical momentum indicator that compares the magnitude of gains to losses over the last 14 trading periods. For the RSI (14), any reading above 70 is considered a strong, possibly overbought, uptrend; any reading below 30 is considered a strong, possibly oversold, downtrend.

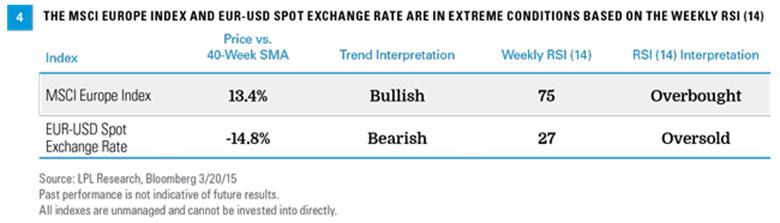

Conversely, related weakness in the price of a euro in dollars (EUR-USD) has pushed the euro into a bearish weekly price trend, as represented by a negatively sloping 40-week simple moving average. The euro’s move lower may be considered substantial, reflected by a weekly RSI (14) in oversold conditions at 27, the weakest value since May 2010 [Figure 2]. A weak euro (and strong dollar) have supported European equities, represented by the MSCI Europe Index [Figure 3], with the strong negative trend for the euro, as measured by an oversold weekly RSI (14), matched by a strong positive trend for the MSCI Europe Index with an overbought weekly RSI (14) [Figure 4].

Currently, we expect the dollar uptrend (and euro downtrend) to remain intact from a technical perspective. However, the trend and RSI (14) indicators are showing potentially overbought conditions, which does increase the potential likelihood of a future trend reversal. Nevertheless, the trend will be considered intact until we see lower highs and lower lows in both the weekly dollar index and the RSI (14). This trend change would be further confirmed by the price crossing below its 40-week simple moving average. A trend change in the U.S. Dollar Index may potentially present an investment opportunity in the euro.

COMMODITIES AND EMERGING MARKETS RIPPLE EFFECTS

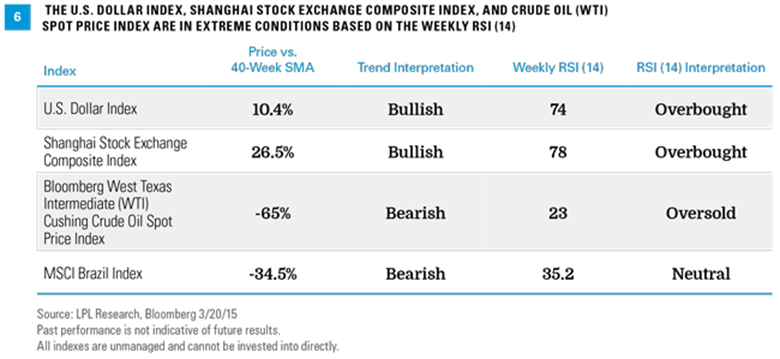

The dollar can also impact commodities and emerging markets (EM), especially those that are large net commodity exporters. For example, as the dollar has climbed, we have seen the price of crude oil move lower, as well as commodity exporters such as Brazil. However, not all EM countries are following crude oil lower (and not all EM countries are big commodity producers). For example, the Shanghai Stock Exchange Composite Index has been trending higher with the dollar, as China’s economy benefits from lower oil while Brazil’s economy is dependent on oil exports [Figures 5, 6]. A potential reversal lower in the dollar could drive crude oil higher. Rising oil would increase the likelihood that the MSCI Brazil Index would move higher and the Shanghai Stock Exchange Composite Index would move lower.

EUROPE: TO HEDGE OR NOT TO HEDGE

The improving technical picture for Europe, coupled with improving economic data, has led us to become more positive on the region. The weak euro is helping drive Eurozone exports, while quantitative easing (the European Central Bank’s bond purchase program) is helping to increase confidence that the central bank will be able to generate desired inflation (and stave off deflation). And although valuations have become more expensive following recent gains, they remain cheaper than those in the U.S.

Should those considering adding European equity exposure hedge currency? We would say yes at this point, given the likelihood that the strong dollar uptrend may continue. By hedging the euro, an investment in European stocks may benefit from the weaker euro’s positive effect on European exports, while not detracting from the returns realized due to the currency translation effects (investment returns overseas can be reduced by a strong U.S. dollar, due to currency translation for U.S.-based investors).

Beyond technical analysis, the dollar should continue to benefit from stronger relative economic growth in the U.S. compared with Europe, higher interest rates, and prospects for the Federal Reserve to begin raising interest rates possibly this fall, while Europe is adding stimulus. Moreover, historically, dollar uptrends can last a number of years (see last week’s Weekly Market Commentary, “Dollar Strength Is a Symptom, Not a Cause,” for more details).

CONCLUSION

Intermarket effects will change over time, but of late, dollar strength has had a significant impact on other currencies, commodities, and both emerging market and developed market equities. As part of our daily process we analyze the markets as a whole and are always looking for relationships that may provide profitable opportunities through the art and science of intermarket analysis.

IMPORTANT DISCLOSURES

All performance referenced is historical and is no guarantee of future results.

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Technical analysis is a methodology for evaluating securities based on statistics generated by market activity, such as past prices, volume and momentum. Technical analysts do not attempt to measure a security’s intrinsic value, but instead use charts and other tools to identify patterns and trends. Technical analysis carries inherent risk, chief amongst which is that past performance is not indicative of future results

All indexes are unmanaged and cannot be invested into directly.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

INDEX DESCRIPTIONS

The US Dollar Index (USDX) measures the value of the United States Dollar relative to a basket of foreign currencies. USDX goes up when the US dollar gains “strength” (value) when compared to other currencies. The make-up of the “basket” has been altered only once, when several European currencies were subsumed by the euro at the start of 1999.

The MSCI Europe Index is a free-float weighted equity index designed to measure the equity market performance of the developed markets in Europe. It was developed with a base value of 100 as of December 31, 1998.

The MSCI Brazil Index measures the performance of the large and mid-cap segments of the Brazilian market. With 70 constituents, the index covers about 85% of the Brazilian equity universe.

The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The index was developed on December 19, 1990 with a base value of 100.

DEFINITIONS

Momentum is the rate of acceleration of a security’s price or volume. The idea of momentum in securities is that their price is more likely to keep moving in the same direction than to change directions.

Overbought is a technical condition that occurs when prices are considered too high and susceptible to a decline. Overbought conditions can be classified by analyzing the chart pattern or with indicators such as the Relative Strength Index (RSI). A security is sometimes considered overbought when the Relative Strength Index (RSI) exceeds 70. It is important to keep in mind that overbought is not necessarily the same as being bearish. It merely infers that the stock has risen too far too fast and might be due for a pullback. The caveat is that sometimes when prices are in an overbought condition they may stay that way until the trend reverses, which is classified as momentum.

Oversold is a technical condition that occurs when prices are considered too low and ready for a rally. Oversold conditions can be classified by analyzing the chart pattern or with indicators such as the Relative Strength Index (RSI). A security is sometimes considered oversold when the Relative Strength Index (RSI) is less than 30. It is important to keep in mind that oversold is not necessarily the same as being bullish. It merely infers that the stock has fallen too far too fast and potentially may be due for a reaction rally. The caveat is that sometimes when prices are in an oversold condition they may stay that way until the trend reverses, which is classified as momentum.

(c) LPL Financial