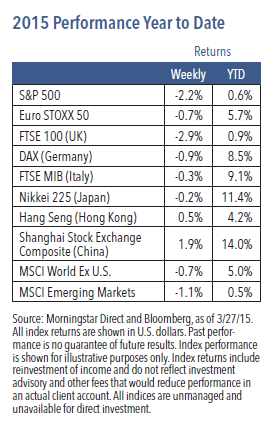

Downward pressure on U.S. equities returned last week, with the S&P 500 Index falling 2.2%.1 This marked the second-largest weekly downturn of the year and the fourth negative week in the last five.1 Some of the decline can be attributed to fading positive sentiment that came in the wake of the recent Federal Reserve meeting. Ongoing negative earnings forecasts have taken their toll as well. All market sectors were in negative territory last week, with financials, technology and industrials losing the most ground and consumer staples and energy holding up the best.1

Weekly Top Themes

1. Fourth quarter growth was a bit weaker than expected, but the consumer sector showed strength. Despite expectations that it would be revised upward, the gross domestic product growth report remained unchanged at 2.2%.2 One bright spot was that real spending hit its strongest level since 2006, suggesting that consumers have benefited from the drop in energy prices.2

2. Corporate earnings estimates continue to weaken. Falling oil prices and the rising dollar have prompted analysts to cut expectations. Earnings for U.S. companies are now expected to grow 2% in 2015, down from 8% at the beginning of January.3 At the same time, sales are expected to contract by 1.0%, compared to growing by 2.5%.3 Downgrades have been concentrated in the energy sector, but the fallout from the strong dollar has also been hurting multinationals.3

3. Concerns over an economic slowdown should be temporary. Given the recent spate of relatively weak economic data, we expect fears of a slump will persist over the next few months. Longer term, however, we believe stronger employment growth and improving consumer spending levels will cause some degree of economic optimism to return. We still expect the Fed will begin rate increases this year, which should reduce concerns over deflation. This shift should also cause bond yields to rise.

4. The trend of global growth decoupling is persisting. Notwithstanding some recent data, the U.S. economy is still accelerating while China is showing signs of a deceleration. Within Europe, we are also starting to see evidence of different growth rates, with Germany appearing to improve as France, Italy and Greece struggle.

5. Negotiations between Greece and the European Union remain stalled. Although we have not seen much progress in talks lately, we still expect a relatively benign outcome and do not anticipate that Greece will exit the European Union. Nevertheless, the possibility of some sort of significant financial disruption cannot be ignored.

Improving Growth Should Eventually Help Risk Assets

Equities have been struggling to find direction, with sagging profits weighing prices down and still-ample liquidity providing a tailwind. In the immediate aftermath of the recent Fed meeting, investors interpreted its statement as a sign that interest rate hikes may be delayed, but the Fed really hasn’t changed stances. It has indicated all along that any rate moves would be data dependent and has done little more than acknowledge that recent data has been somewhat disappointing. In our view, at least some of the recent softness is due to harsh winter weather and the West Coast port strikes, both of which are temporary factors. Looking ahead, we think the employment picture remains positive and we expect the broader data to rebound.

Despite the recent deterioration in earnings trends, U.S. equities have still held up reasonably well. We expect earnings data to remain volatile due to the twin factors of lower energy prices and a stronger dollar. However, earnings should improve in the second half of 2015 as the economic recovery regains traction. Stock prices are likely to remain volatile as well as investors digest earnings data and await more signals from the Fed. When the Fed does raise rates, it should do so slowly and carefully and it should serve as an acknowledgement that the economy has strengthened. Outside of the U.S., policy is still in an easing trend, which should help the global economy. Together, all of these factors should mean that we see solid returns for equities, particularly compared to bonds and cash. But until the earnings picture improves, gains will be tougher to come by.

1 Source: Morningstar Direct, as of 3/27/15 2 Source: Bureau of Labor Statistics 3 Source: MRB Partners

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted averageof 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc. ©2015 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM5-0315P 6829-INV-W-03/16