I began investing in convertible securities during the 1970s, and since then, I’ve seen an exciting evolution of the asset class—from little-known securities to a global asset class totaling approximately $342 billion USD today, including issues from household-name companies worldwide. Clearly, what began as an “alternative investment” has become much more mainstream.

Despite this growth and broader acceptance, the different ways that convertibles can be used in asset allocation are less well understood. What’s important to remember is that convertibles can support multiple asset allocation goals because of their hybrid characteristics. Convertibles combine equity and fixed income attributes, but the balance changes over time—both for the convertible universe as a whole as well as for individual securities. That makes active management essential. You can’t reap the potential benefits of convertibles simply by including them in a portfolio. Instead, you need to find the right blend of convertibles and manage them to achieve a particular objective.

Because convertibles offer the opportunity for equity participation with potential protection from downside volatility, I’ve long advocated including them within a strategic (or core) allocation, held through full market cycles. (My paper, “The Case for Strategic Convertible Allocations.” explores this at greater length.) In my view, the benefits of using convertibles to pursue lower-volatility equity participation are particularly pronounced in the current market environment. As our team has discussed in other posts, this bull market has been volatile but we see continued upside. Because fixed income attributes may lessen the impact of equity market downside, convertibles can mitigate anxiety about short-term market fluctuations.

In addition to holding convertibles strategically through market cycles, I believe there’s good reason overweighting convertibles more tactically in the current environment, within what I like to call an “enhanced fixed income” allocation. An enhanced fixed income allocation seeks to further portfolio diversification—with less vulnerability to interest rates changes than traditional fixed income investments (government bonds and investment-grade corporate bonds). Increasingly, we’re speaking with institutional investors who are concerned about how an eventual rise in interest rates could hurt their fixed income investments. Convertibles have historically been less sensitive to interest rate risk because of their equity characteristics. This can make convertibles a compelling alternative to traditional fixed income securities—for institutional and individual investors alike.

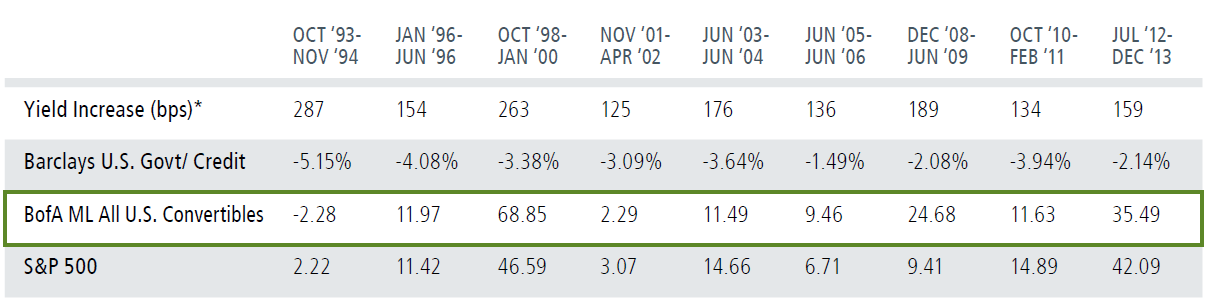

Convertibles Delivered Compelling Performance in Rising Interest Rate Environments

Past performance is no guarantee of future results. Source: Morningstar Direct and Bloomberg; most recent data as of 12/31/2014. Yield is represented by the 10-year Treasury yield, showing periods where yields rose more than 100 basis points. Performance shown is cumulative.