Earnings season kicks off this week (April 6 – 10) with Alcoa set to report first quarter 2015 earnings on Wednesday, April 8. This earnings season has received a great deal of attention in recent weeks because it may produce the first year-over-year decline in S&P 500 operating earnings since the tail end of the financial crisis during the third quarter of 2009. We preview earnings season and highlight reasons not to fear a potential decline.

FLAT IS THE NEW UP

Earnings growth has stalled in early 2015 primarily due to low oil prices and a strong U.S. dollar. The Thomson Reuters–tracked consensus currently expects a 2.8% year-over-year decline in S&P 500 earnings for first quarter 2015, compared with the 7% earnings gain produced in fourth quarter 2014. Should the S&P 500 produce the average upside surprise observed over the past four quarters (4%), then earnings may match the year-ago period or perhaps even grow marginally. Given these significant drags — each with an estimated impact of 4 – 6% — we would expect this outcome to be well received by the market, should it occur. Revenue is expected to drop by a similar 2.3%.

Upside to earnings estimates could come from several places:

- Low energy prices. Lower energy prices for consumers are like a tax cut that should help support earnings for the consumer sectors. Lower fuel costs also help lower transportation costs, which may benefit railroads, airlines, and shipping logistics providers (though lower fuel surcharges may mitigate benefits).

- Stellar cost management. Profit margins for S&P 500 companies remain near record highs and, we believe, probably held up well overall during the first quarter of 2015. Wage gains are the biggest component of the S&P 500 companies’ costs, and wage gains remain moderate at about 2% despite the drop in unemployment (based on the March 2015 jobs report). Commodity prices are another big corporate cost and those prices — even beyond oil — continue to fall. The Bloomberg Commodity Index has fallen about 4% year to date after a double-digit decline in 2014. And borrowing costs remain low.

- European growth picking up. This one is a double-edged sword, because one of the reasons European growth is picking up is the weak euro and its effect on European exports. That same weak euro (and corresponding strong dollar) is a drag on profits earned in Europe translated back into dollars. Nonetheless, on the margin we expect a good number of U.S. multinationals to cite improved economic conditions in Europe.

- (Slightly) better environment for financials. Increased volatility helps the trading divisions for the big money center banks and brokerage firms. Currencies are likely to prove particularly rewarding for the first quarter. The pace of legal settlements should continue to abate. And financials earnings fell modestly during the year-ago quarter compared with first quarter 2013, potentially setting the stage for upside surprises with an easy comparison. Low interest rates still hurt but may be already factored into estimates.

LOWER BAR EASIER TO CLEAR

The earnings bar has been lowered significantly, which may increase the odds of upside surprises. During the three months ending March 31, 2015, consensus first quarter 2015 S&P 500 earnings were cut by 8%. This compares with the average quarterly reduction of 3% over the past five years (20 quarters) and 4.8% over the past 10 years, according to FactSet data. Much of the reduction can be explained by energy and the dollar, but still the bar looks pretty low when considering the magnitude of the cuts and the comparison with the prior-year period.

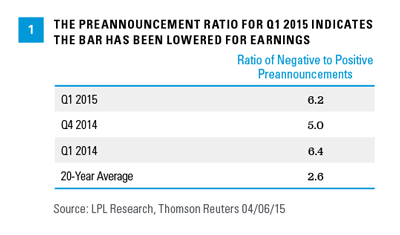

GUIDANCE KEY: ENERGYAnother way to assess how far the bar has been lowered is by looking at the preannouncement ratio: the number of companies providing positive guidance (raising estimates) versus negative guidance (lowering estimates). During the first quarter this ratio was 6.2, worse than the 20-year average of 2.6 according to Thomson Reuters, although similar to first quarter 2014 (6.4) and fourth quarter 2014 (5.0) [Figure 1]. Companies’ ability to manage expectations effectively may potentially increase upside surprises.

This quarter, much like last quarter, we are sure to hear a lot from management teams about the impact of the strong dollar. (We have written recently on that topic in two Weekly Market Commentaries: “Dollar Strength Is a Symptom, Not a Cause,” on March 16, 2015, and “The Dollar’s Ripple Effect,” on March 23, 2015.) But we believe energy may be the key to how well future earnings estimates hold up during the six busy weeks of earnings reports.

As guidance comes in from energy companies, we may find that estimates for the sector have been sufficiently cut already. First quarter 2015 S&P 500 energy sector earnings estimates were cut by more than 60% over the past six months. Estimates for the next two quarters (Q2 and Q3 2015) have both been reduced by similar amounts (65 – 70%, based on Thomson Reuters–tracked estimates), and reflect yearly declines of more than 60%. For comparison, energy sector earnings fell by about 50% during the oil downturn in the early 2000s (October 2001 through March 2003), and by about 70% during both the 2008 – 2009 financial crisis (admittedly not a great comparison) and the mid-1980s oil downturn (March 1984 through December 1987, based on Ned Davis Research earnings estimates). We believe the mid-1980s period offers a reasonable comparison because a boom in U.S. energy production came during the middle of an economic expansion.

Beyond energy, we expect management teams to remain generally positive in their outlooks for the U.S. economy despite the latest slowdown, as temporary drags (West Coast port strike, harsh winter weather) are expected to reverse, and we hope to hear upbeat commentary on business conditions in Europe. (For more details, see the Weekly Economic Commentary, “Beige Book: Window on Main Street,” March 9, 2015.)

ISM SIGNAL HANGING IN THERE

WHAT IF WE HAVE AN EARNINGS RECESSION?Our favorite earnings indicator, the Institute for Supply Management (ISM) Manufacturing Index, has continued to signal earnings gains over the next six to nine months and offers an encouraging sign regarding where earnings may be headed [Figure 2]. Although the index pulled back during March 2015 due to temporary factors, it remains in expansion territory at slightly over 50 (50 is the breakpoint between growth and contraction for the index) and well above the sub-40 levels that have historically signaled recession.

Despite some evidence to the contrary, earnings may drop versus the prior year when first quarter results are in the books. The same could happen in the second quarter, where the Thomson Reuters consensus is indicating a marginal 0.6% decline. Using the unofficial definition of an economic recession as two straight quarters of contraction, could an earnings recession with two straight negative growth quarters be in the cards?

The answer is, it is possible, but there are several reasons not to be overly concerned. First, we expect the two primary drags on earnings to reverse. The dollar will almost certainly not repeat its dramatic ascent of the past year and oil prices may soon stabilize (that process is well underway). Energy companies will align costs with revenue over the balance of the year, and thus, should not weigh nearly as heavily on 2016 profits. Bottom line, we expect market participants to look beyond these temporary factors to better earnings growth later this year and into 2016.

It is also worth noting that we’ve been in potentially similar situations before. During the mid-1980s (1985–1986) and late 1990s (1998), S&P 500 earnings growth similarly dipped into negative territory despite U.S. economic growth. In addition, earnings were flat during the third quarter of 2012. Earnings quickly rebounded in all of these cases and the S&P 500 delivered solid returns during the subsequent year after the earnings declines.

(Keep in mind different sources such as FactSet, Bloomberg, and others have different calculations than Thomson Reuters for S&P 500 earnings, based on different methodologies and different interpretations of what constitutes operating earnings. So some sources may cite an earnings recession and others may not.)

CONCLUSION

First quarter 2015 earnings will likely not be very good, due to the drags of low oil prices and the strong dollar. However, results for S&P 500 companies may exceed dramatically reduced expectations and we see better prospects for earnings as the year progresses. We continue to expect earnings to drive stock market gains in 2015, as we stated in our Outlook 2015: In Transit, but investors may need to be a bit more forward looking. n

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The Bloomberg Commodity Index is calculated on an excess return basis and composed of futures contracts on 22 physical commodities. It reflects the return of underlying commodity futures price movements.

(c) LPL Financial