The Case for Not Currency Hedging Foreign Equity Investments: A U.S. Investor’s Perspective

EXECUTIVE SUMMARY

Investors often ask about GMO’s approach to currency hedging, even more so recently as the U.S. dollar has strengthened. We hedge currency for fixed income investments as they represent a nominal stream of cash flows in the local currency, but we do not typically hedge currency for equity investments. In the age of globalization, most companies have multi-currency costs and revenues; shorting the local currency on top of the equity investment does not hedge an exposure, but rather adds new risks to the investment. Therefore, as a rule we do not hedge currency for equity investments, but there are exceptions. For example, if we owned a portfolio of domestically-oriented stocks with most costs and revenues in a local currency, we may decide to hedge the currency exposure.

Many investors cite volatility reduction as a rationale for currency hedging. In this paper, we intend to show that:

1. While currency hedging may reduce volatility over short investment horizons for USD investors, it does not reduce volatility over long horizons;

2. Volatility reduction has decreased over time as companies have become more global;

3. Even if currency hedging reduces the short-term volatility of the international equity holdings, it does not reduce the volatility of the global equity portfolio because hedged equities are more correlated with U.S. equities than unhedged equities;

4. Hedging introduces leverage, which can lead to higher tail risk.

Although we do not employ simple currency hedging strategies for international equity investments, we engage in active currency management, incorporating currency positions supported by high-conviction views.

Introduction

Many investors ask whether we hedge the currency risk associated with positions in non-U.S. equites. To adequately address this question, it is necessary to describe our investment philosophy, which drives our approach to currency management.

We believe that to be successful we must have a long horizon, understand that over that period fundamentals and valuations matter, and recognize that risk is not described by a single number. Guided by these tenets, we will take active currency positions when we have a high-conviction view, but considering international equity investments, our default position is to own them unhedged.1

Currency “hedging” is not hedging

In the age of global business models, most large cap companies are not exposed purely to the currency that their stock is denominated in. For example, roughly half of U.K. stock market capitalization is comprised of companies whose business has minimal exposure to the United Kingdom; these companies simply decided to list in London.2 Shorting the British pound against a basket of U.K. stocks does not “hedge” currency exposure; it layers on a directional short currency position.

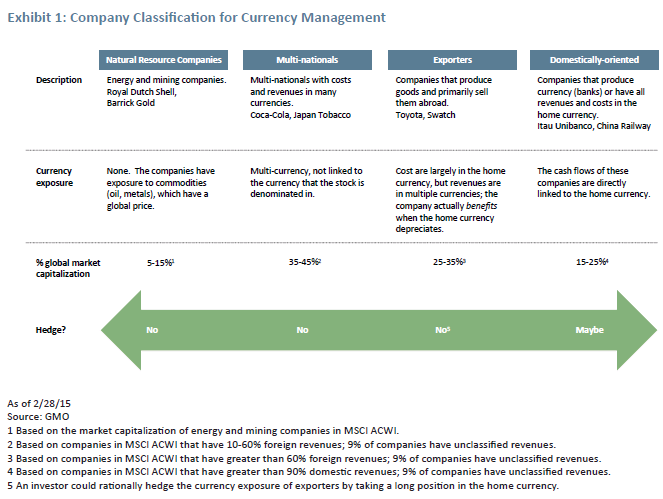

From the perspective of considering currencies, companies can be divided into four categories (see Exhibit 1). Most companies’ cash flows are multi-currency; in some cases, the cash flows have no relation to the currency that the company’s stock is denominated in. For natural resource companies (energy, mining), the dominant exposure is commodity exposure. As commodities have a globally set price, the associated revenues are not linked to any particular currency. Multi-national companies have revenues and costs in many currencies, thus their cash flows do not have direct exposure to any one currency. Exporters earn the vast majority of their revenues abroad. Exporters may actually benefit from a fall in the home currency as their products become more competitive abroad; by the same logic, exporters can be hurt by the appreciation of the home currency as their goods become relatively more expensive. For that reason, an investor could rationally hedge the currency exposure of exporters by taking a long position in the home currency. Certain domestically-oriented companies, which do the vast majority of their business locally, do have exposure to the home currency. For these domestically-oriented companies, it may make sense to hedge currency exposure, but these companies make up only 15-25% of global market capitalization.

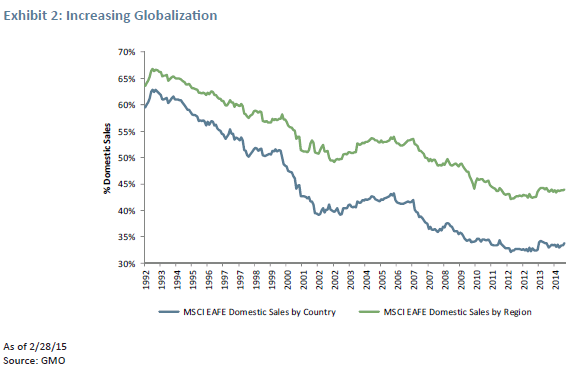

Globalization has increased significantly over the past 20 years. In 1992 60% of sales for developed international companies (as defined by MSCI EAFE) were domestic; today less than 35% of these companies’ sales are domestic (see Exhibit 2). For that reason, understanding the currency exposures of international stock holdings has become less straightforward over time.

Overall, a broad, diversified allocation3 to international stocks would not have an easily definable currency exposure.4 Yes, there are some domestically-oriented companies with closer ties to their home currency, but they are offset by exporters who have negative exposure to their home currency. It is not possible to hedge an exposure that is not there.

Currency hedging actually increases risk

Does hedging reduce volatility?

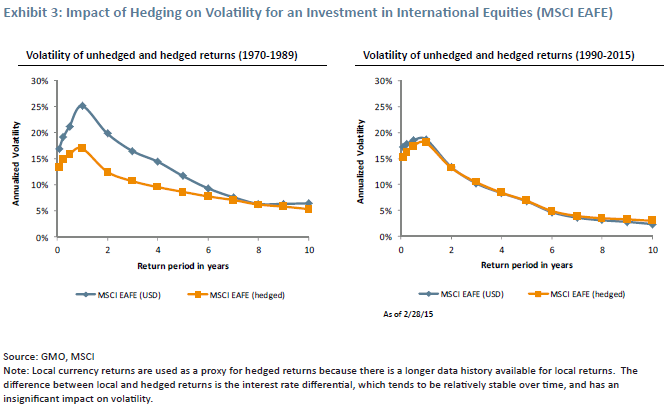

Investors frequently cite empirical work that demonstrates that hedging currency for international equities reduces risk (by “risk” they mean “volatility”). In the short term (i.e., less than a five-year investment horizon), hedging currencies may reduce volatility. For us at GMO, a reduction in short-term volatility is not a compelling argument for hedging because we are long-horizon investors.

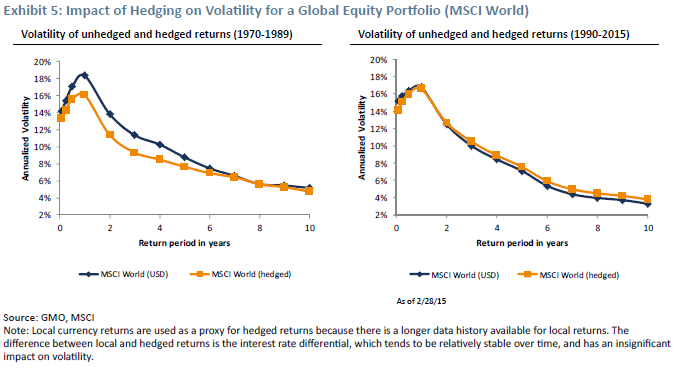

Relying on historical data can be problematic due to changing market dynamics, in particular, the increase in globalization shown in Exhibit 2. As shown in Exhibit 3, the impact of hedging on volatility was markedly different from 1970-89 than from 1990 to today. From 1970-89 currency hedging had a clear impact on the volatility of international stocks (MSCI EAFE). However, focusing on more recent data, there is little notable risk reduction beyond a one-year holding period; for longer investment horizons, hedging has resulted in marginally higher volatility. As globalization has increased, simple currency hedging strategies have been less effective; trends observed in historical data analysis may not persist in the future.

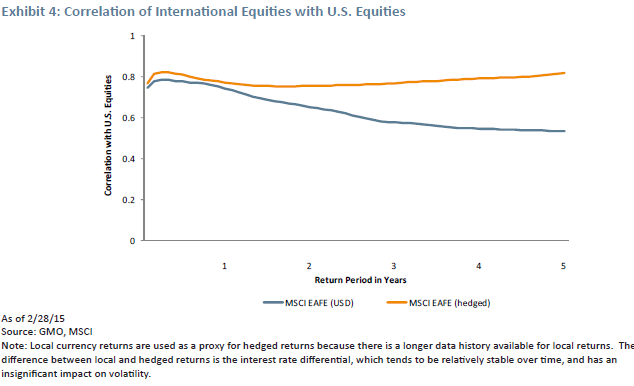

Even over the time periods when hedging has been a volatility reducer, hedged equities have had a higher correlation to the U.S. stock market than unhedged equities (see Exhibit 4).

At the levels of non-U.S. equity exposure that most investors have in their portfolios, hedging doesn’t meaningfully reduce portfolio volatility even if it does reduce the volatility of the non-U.S. equities on a stand-alone basis. Hedging the international equities in a global equity portfolio has increased the total portfolio volatility for a two-year holding period or longer (1990 to today, Exhibit 5, right chart). For most investors, non-equity (primarily fixed income) assets are also largely USD-based; unhedged equities provide valuable diversification at the total portfolio level. By focusing on the impact of hedging on one area of the portfolio (international equities), investors may be missing the impact to the overall portfolio.

Hedging may increase tail risk

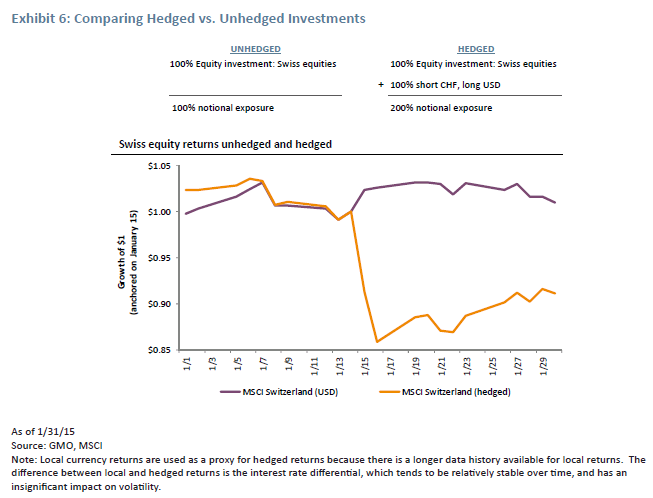

The idea that hedging increases volatility in the long term may seem counter-intuitive. While commonly accepted as a benign form of leverage, currency hedging equities increases the notional exposure, and therefore the magnitude of possible return or loss (see Exhibit 6). In other words, hedging increases tail risk by layering (short) currency exposure to the equity investment.

A recent example to illustrate this point is the case of Swiss equities in January 2015. On January 15, 2015, the Swiss National Bank abandoned the peg to the euro, and the Swiss franc sharply appreciated relative to the euro (and most other global currencies including USD). In local terms, the equities fell sharply (MSCI Switzerland was down 14.1% across January 15 and 16 in local currency) while an unhedged investment from a U.S. investor’s perspective had only a modest impact (MSCI Switzerland was up 2.6% in USD). The Swiss market as a whole maintained approximately the same value from a U.S. investor’s perspective because the appreciation of the currency was offset by a move in the equities; the market overall did not change intrinsic value. It is true that certain Swiss exporters (e.g., Swatch, a watchmaker with over 80% of its revenues sourced abroad) lost competitiveness, and those stocks fell in USD terms. However, this impact was offset by domestic companies (e.g., Swisscom, a telecommunications company that earns the substantial majority of its revenues in Switzerland) that generate a nominal Swiss franc cash flow, which became more valuable from a U.S. investor’s perspective.

Likewise, consider an investment in the European periphery today (e.g., Spain and Italy). This equity investment may be held unhedged, or the investor could currency hedge by adding a short euro position. In late 2014 through early 2015, hedged European equities delivered higher returns than unhedged equites as the euro has weakened relative to the U.S. dollar (i.e., short euro relative to USD was a good trade). Looking forward, we believe there is a risk to shorting the euro. Hypothetically, if Spain and Italy were to exit the eurozone, Spanish and Italian equities would likely deliver negative returns. In this scenario, the euro could appreciate as the weaker countries leave the euro (i.e., the euro effectively becomes a Deutschmark, a stronger currency). In this hypothetical example, an investor could lose on both sides of a hedged equity position: the equities fall, and the short euro position generates a (potentially substantial) loss as the euro strengthens. Investors must be careful to understand the fundamental risk exposures of investments and resist the temptation to employ a strategy that promises volatility reduction or one that has impressive recent returns. Some investors may believe that an unhedged equity position has unintended risks; we believe a hedged equity position has the potential for even greater unintended risks.

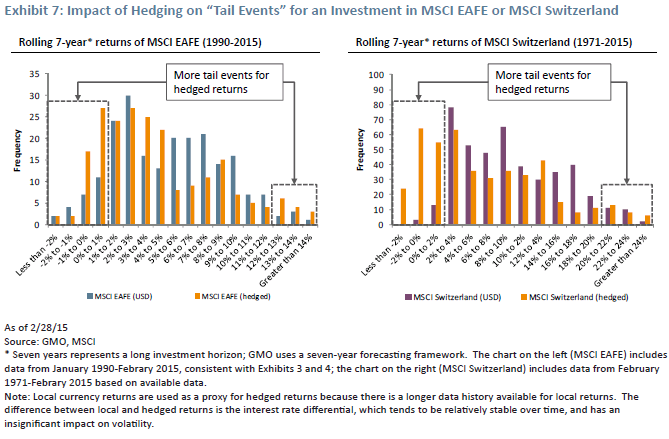

Looking at returns over a long horizon, we can see the evidence of the increase in “tail events,” be they positive or negative; see Exhibit 7 for a histogram of rolling seven-year returns for MSCI EAFE and MSCI Switzerland.

Hedging reduces the volatility of an international equity investment in the short term if the short currency position has a negative correlation to the equities, not because hedging is eliminating a risk exposure. Effectively, this is a “correlation hedge” and investors are relying on the correlation persisting. Because the USD is a safe haven currency (i.e., it tends to do well when equities suffer), currency positions that are short foreign currency and long USD have tended to exhibit a negative correlation to local market equity returns over short horizons. (Please see sidebar on page 8 for a discussion of other base currencies.) However, as discussed, these hedged equities have a higher correlation to U.S. stocks and bonds, limiting volatility reduction at the total portfolio level. Over the long term, the increased tail events (from the levered position) increase the volatility of a currency-hedged position.

Currency hedging adds inflation risk to the equity investment

Adding a currency position to an equity investment may actually increase the risk exposure. Equities are real assets: they are shares of companies that produce real goods and services. Over the long term, companies keep pace with inflation by selling their goods and services at higher prices. Currencies are not real assets: a currency depends on the creditworthiness of its issuer. A currency can be completely devalued by unexpected inflation as has happened with hyperinflation scenarios like Brazil (1980-94). By adding an inflation-sensitive asset to a real asset, you effectively add inflation risk to your equity investment. Underwriting an additional risk without getting paid for it is not a good investment strategy.

We believe currency hedging gives investors a false sense of risk reduction; hedging does not eliminate a risk exposure and can actually increase overall fundamental risk.

We don’t hedge as a rule, but there are exceptions

For most international equity holdings, there is not a direct exposure to the home currency, as we showed in Exhibit 1. However, there are certain investments where currency hedging may make sense.

Domestically-oriented companies

An investor may want to hedge a concentrated investment in domestically-oriented companies (e.g., banks, insurance companies, REITs). Domestically-oriented companies realize the majority of their revenues and costs in the local currency; therefore their cash flows are essentially a nominal return stream in the local currency. An investor who does not want exposure to that currency may choose to hedge these types of equities. In 2013, some of GMO’s asset allocation strategies held a portfolio of Japanese equities that was substantially allocated to domestically-oriented companies. At that time, we did not want exposure to the yen because we believed it was expensive, so we hedged the domestically-oriented portion of our Japanese stocks by shorting yen.

A NOTE ON NON-U.S. DOLLAR INVESTORS

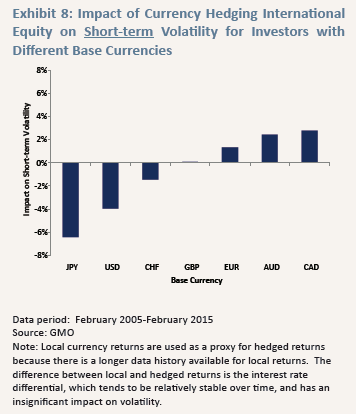

This paper discusses currency hedging international equities from a U.S. dollar investor’s perspective. The analysis may look different depending on the investor’s base currency. For example, consider the impact of currency hedging on short-term volatility (Exhibit 8). For U.S. dollar, Japanese yen, and Swiss franc investors, hedging reduces volatility in the short term. These are safe haven currencies (i.e., they tend to do well when equities suffer). Currency positions that are short foreign currency and long the safe haven currency have typically exhibited a negative correlation to local market equity returns, hence reducing volatility. For euro, Australian dollar, and Canadian dollar investors, hedging currency has actually increased short-term risk. These are high beta currencies (i.e., they tend to do well when equities do well). Currency positions that are short foreign currency and long the high beta currency have typically had a positive correlation to local market equity returns, hence increasing volatility.

Long/short investments

Our practice of not hedging currency risk for equity investments holds for long-only investments. In long-only investments, volatility is a positive: it provides opportunities for the patient, long-term investor, but it does not impose a requirement that the investor take any action. A fall in the price of the asset gives the long-only investor the opportunity to buy more at a more attractive valuation, but the investor does not have to take any action at all. In a long/short portfolio, volatility is a negative because it can force the investor to take action; for example, an investor may be compelled to cover a short position, thereby locking in a loss. For that reason, anything that can make a long/short position less volatile without impacting expected return improves the trade. Because of the short-term correlation between stocks and their local currency, adding a currency position (hedging) may be a way to mitigate this drag from volatility.

Active currency management is an important part of the GMO process

Though we do not typically hedge currencies, we are not absolving ourselves of currency management. When we have a high-conviction currency view, we will express that in our portfolios whether or not we have a long position in the stocks of that country. In addition to developing long-term forecasts for stocks and bonds, we also develop long-term forecasts for every major currency, and frequently express active currency positions across portfolios.

Conclusion

At GMO, we carefully consider how currency can impact portfolios, both in terms of risk and expected return. Our baseline position is to hold international equities unhedged. In fact, we are concerned that the term “currency hedging” gives investors a false sense of security, as adding currency positions to equity investments may add risk. While we typically do not hedge currencies for equity allocations, we may for specific equity investments, for example, a position in foreign banks. As always, we view active currency management as an important source of potential return.

Recently, as assets have been flowing into currency hedged equity exchanged traded funds (ETFs),5 we worry that investors have observed the higher returns from hedged equities as the dollar has risen and concluded that currency hedging is the right thing to do. Systematic currency hedged strategies (such as hedged ETFs) short currencies based on the stock’s listing currency. As we demonstrated in Exhibit 1, we believe this is not an accurate representation of the currency exposure. In fact, by adding short currency positions, investors may be opening themselves up to new risks. Currency management is a useful tool when done for the right reasons: because of a high-conviction view, or a desire to mitigate an identified risk exposure. We caution that a simple currency hedging strategy may not achieve these objectives.

1 The comments in this paper do not hold true for fixed income investments. In the case of fixed income, our default position is to hedge because the cash flows of fixed income contracts are directly tied to a particular currency.

2 Roughly 49% of U.K. listed companies (by market capitalization) in MSCI ACWI have less than 10% of revenues from the U.K. An additional 20% of U.K. listed companies in ACWI have unclassified revenue data. Examples of U.K. listed companies with limited business in the U.K. include: BHP Billiton Limited (BHP), Glencore PLC (GLEN), and Rio Tinto LTD (RIO). (Source: GMO as of February 28, 2015.)

3 For a concentrated stock portfolio, the manager could reasonably estimate the underlying currency exposure by looking at each company’s currency exposure and make a hedging decision based on that analysis.

4 Additionally, some companies may engage in their own currency hedging programs.

5 Michael Shagrin, “Institutional Investors Flock to Currency Hedging as Dollar Surges,” Fund Fire, March 16, 2015.

Catherine LeGraw Ms. LeGraw is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2013, she worked as a director at BlackRock. Previously, Ms. LeGraw was an analyst at Bear, Stearns & Co. She received her B.S. and her B.A. in Economics from the University of Pennsylvania. She is a CFA charterholder.

The author would like to acknowledge the meaningful contributions of Ben Inker, Sam Wilderman, and Tom Hancock as well as thank GMO colleagues for their thoughtful suggestions.

Disclaimer: The views expressed are the views of Catherine LeGraw through the period ending April 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

© GMO