Global growth is likely to be a recurring theme for investors this week. The health of the global economy and key regions (U.S., Eurozone, Japan, China, etc.) is likely to get plenty of attention from corporate managements as they discuss Q1 2015 results and provide guidance for the rest of the year. In addition, the International Monetary Fund (IMF) will release the spring 2015 edition of its widely read World Economic Outlook on Tuesday, April 14, 2015, and China will release its Q1 2015 gross domestic product (GDP) that same day.

The outlook for global growth is important to investors, as it defines the ultimate pace of activity that creates value for countries, companies, and consumers. As investors begin to digest the S&P 500 earnings reports for the first quarter of 2015 (32 S&P 500 companies will report Q1 2015 results this week, with another 312 set to report in the final two weeks of April 2015), we provide an update on how consensus estimates for economic growth for 2015 and 2016 — in the United States and worldwide — have evolved over the past few years, and in particular, since oil prices peaked in mid-2014. We’ll also take the first look at how global growth is shaping up for 2017.

WHY GLOBAL GDP GROWTH MATTERS

In the past, prospects for U.S. economic growth garnered the most attention from market participants, but in recent years markets have focused more on global GDP growth. Why does global GDP growth matter? As we have noted in prior Weekly Economic Commentaries, financial markets — especially equity markets — focus intently on earnings. Broadly speaking, earnings growth is driven by “top-line” growth, or revenue growth, less the costs incurred earning that revenue, with labor accounting for more than two-thirds of total costs. A good proxy for global revenue growth is global GDP growth plus inflation. Thus, the pace of growth in the global economy is a key driver of global earnings growth, and ultimately, the performance of global equity markets [Figure 1]. As we noted in the April 6, 2015, edition of the Weekly Market Commentary, “Earnings Recession?” the market expects that S&P 500 companies will post a 2–3% drop in both revenue and earnings growth in the first quarter of 2015 versus the first quarter of 2014. The expected decline in revenue and earnings is primarily driven by the stronger U.S. dollar and the decline in oil prices; however, we expect more than a handful of firms may cite global growth concerns as they discuss Q1 2015 results and provide guidance for the rest of 2015 and beyond.

OIL’S EFFECTS ON GLOBAL GROWTH ESTIMATES

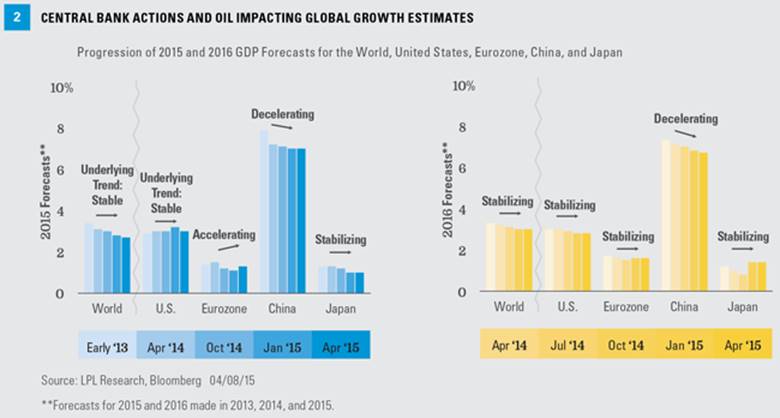

Figure 2 details the progression of the consensus GDP forecasts for 2015 and 2016 for the world, the United States, China, the Eurozone, and Japan over the past several years, while Figure 3 presents the change in the Bloomberg consensus GDP growth estimate for 2015 and 2016 for the 15 largest economies in the world, which account for 83% of global GDP.

The latest (mid-April 2015) Bloomberg-tracked economists’ consensus forecast for 2015 global GDP growth stands at 2.7%, down from the 2.8% expected three months ago in January 2015. In mid-2014 — just as oil prices peaked— the consensus expected 3.1% growth in 2015. A year ago, in early 2014, the consensus expected 3.1% growth in 2015; and in early 2013, when Bloomberg first began tracking consensus estimates for global GDP growth for 2015, the consensus expected 3.4% world GDP growth.

VARYING REVISIONS TO 2015 ESTIMATES, MAINLY DUE TO OIL

Although other factors are at play (inflation, war, sanctions, weather, fiscal and monetary policy, political and social upheaval, as well as longer-term secular trends like demographics), the drop in oil and other commodity prices over the past year or so has played a key part in the progression of GDP forecasts across the globe. The United Kingdom and India were the only countries to see the consensus expectations for 2015 growth revised higher since oil peaked in mid-2014. The consensus for South Korea’s 2015 growth rate was unchanged over the past year, while the GDP growth forecasts for the United States, Turkey, and Poland were only marked down marginally. The United States, India, and South Korea are all in the top five of net oil-importing countries and are benefiting from the drop in oil, and both Turkey and Poland are net importers of oil. Although China is also on the list of top oil-importing nations (it is number two), its economic growth prospects have moved down sharply over the past 12 months.

SEVERAL FACTORS ARE CONTRIBUTING TO CHINA’S DECLINING GROWTH PROSPECTS

All else being equal, the drop in oil and commodity prices should have been a net positive for China’s growth prospects, but several of the factors noted above swamped the positive impact of oil, and forecasters have continued to mark down their estimates for China’s growth. In early 2014, the consensus forecast for the Chinese economy called for 7.2% growth in 2015. Today, the consensus is 7%. In recent months, China’s leaders have set the stage for a downshift in growth expectations in China and want markets to focus on a set of broader economic and social indicators as the best measures of China’s economy, and they have hinted that economic growth in 2015 may be in the 6.5 – 7.0% range.

RUSSIA’S ECONOMY IS NOW EXPECTED TO CONTRACT

Not surprisingly, Russia, one of the globe’s top oil producers, has seen its 2015 growth estimates cut sharply over the past year, but oil wasn’t the only reason forecasters took down their view of Russia’s economic activity. Russia’s undeclared war with Ukraine — and the sanctions that resulted — along with increased uncertainty around Russian President Putin’s activities, have taken a severe toll on Russia’s economy. In early 2014, the market was expecting the Russian economy to grow at around 2.0% in 2015. Today, the consensus expects the Russian economy to contract by more than 4% this year.

ECB AND BOJ TAKE CONTINUED ACTION TO STRENGTHEN THEIR ECONOMIES

As noted above, since oil prices peaked in June 2014, only three nations have seen their 2015 growth estimates remain the same or move higher: the United Kingdom, South Korea, and India. Four nations have seen their 2016 growth estimates hold steady or move higher over the same period, including the Eurozone and Japan. The central banks of both areas (the Bank of Japan [BOJ] and the European Central Bank [ECB]) have embarked on massive bond buying (quantitative easing [QE]) programs in an effort to reinvigorate their respective economies. Both the Eurozone and Japanese economies should be net beneficiaries of the drop in oil and commodity prices, but demographics lean heavily in the other direction. Unless growth — and more importantly, inflation — picks up in Japan in the coming months, the BOJ is likely to increase the size of its QE program.

WHAT MATTERS NOW

At this point in the year, 2015 economic growth matters much more than 2016, but by the middle of this year, market participants’ focus will be firmly on 2016. When Bloomberg first tallied up 2016 global growth estimates in early 2014, the consensus was for 3.2% growth [Figure 2]. Today, the forecast stands at just 3.0%, which is an acceleration from 2015’s forecast of 2.7%, but still relatively sluggish by historical standards. Since oil peaked in mid-2014, the consensus forecast for GDP growth in 2016 has moved from 3.2% (July 2014) to 3.0% (today), dragged down by the same factors that have lowered 2015’s forecast.

Although it’s not on the market’s radar just yet, 2017’s economic growth will begin to matter as we move further into 2015. As of April 2015, the consensus for global GDP growth in 2017 is 3.1%, an acceleration from the 3.0% expected in 2016. Russia, Brazil, Mexico, India, and Australia are all expected to see a substantial acceleration in growth in 2017 versus 2016, while growth is expected to slow significantly (versus 2016) in China and Japan.

On balance, the market continues to expect that global GDP growth will accelerate in 2015, 2016, and 2017, aided by lower oil prices and stimulus from two of the three leading central banks in the world. The prospect for another year of decelerating growth in emerging markets remains a concern for some investors, who may still be waiting (in vain) for China to post 10 – 12% growth rates as it consistently did during the early to mid-2000s. The likelihood of rate hikes in the United States in late 2015 and the United Kingdom in early 2016 is also a potential growth headwind. Still, much stimulus remains in the system, and more is likely from the BOJ and the ECB, which may help bolster growth prospects in two key areas of the globe. Although China is unlikely to embark on QE, Chinese authorities have recently enacted a series of targeted fiscal, monetary, and administrative actions aimed at stabilizing China’s economy in 2015 and beyond, and more such actions may follow.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

(c) LPL Financial