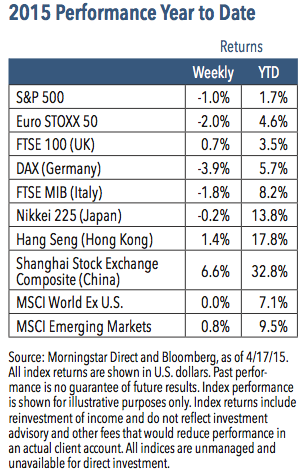

Investors focused on the negatives last week, including some disappointing U.S. economic data and growing concerns over what will happen with Greece’s debt problems. U.S. equities fell, with most of the damage coming on Friday amid a global risk-off trade.1 The S&P 500 Index declined 1.0%, with the industrials sector leading the way downward.1 In contrast, energy performed the best, helped by a rally in oil prices.1 Outside of the United States, Chinese stocks continued to soar,1 as weak economic data sparked expectations for additional policy support. Over the weekend, these expectations came to fruition when the People’s Bank of China announced a cut in bank reserve requirements, a move designed to boost lending.

Weekly Top Themes

1. Earnings expectations look weak, but we expect a rebound later this year. Standard & Poor’s is currently forecasting 2015 earnings for the S&P 500 to increase by a mere 0.2%.2 Most of this weakness is concentrated in the energy sector, and excluding energy, the growth rate would be 7.5%.2 Oil prices and the U.S. dollar both appear to be stabilizing, which we believe should help earnings outperform expectations in the second half of 2015.

2. The beneficial effects of lower oil prices have yet to be realized. In our opinion, the drop in oil prices happened so quickly that the results have yet to work their way through the economy. Even if prices don’t drop further and stay close to their relatively low levels, we think we could still see downward pressure on gasoline prices. Additionally, we expect to see consumer spending rise over the coming months.

3. We continue to have a bullish long-term view toward the dollar. Given the enormous increase since last summer, however, a period of consolidation or correction could last for weeks, or possibly even months.

4. Core inflation appears to be starting to pick up modestly. The core Consumer Price Index ticked up from 1.7% to 1.8% in March,3 which is consistent with our view that inflation is moving from around 1% to closer to 2%. Higher inflation should put pressure on the Federal Reserve to change its current stance. We continue to believe the Fed will begin increasing rates later this year, with September being the most likely liftoff point.

5. Despite the recent strength in the energy sector, we have a negative view toward energy stocks. The recent bounce can largely be attributed to the stabilization in oil prices. At current prices for energy stocks, investors appear to be forecasting a sustainable rise in the price of oil. We do not expect oil prices to experience a significant advance, which may mean that the energy sector could be at risk. Even if oil prices do rise, we believe the relative upside in energy is limited given higher oil prices are already discounted.

Equities Are Treading Water, but Look Resilient

Equities have struggled in recent weeks amid a slowdown in the U.S. economy, drama over Greece’s debt negotiations, lingering concerns about pockets of deflation and increased geopolitical tensions. Under the surface, however, it looks to us like the global economy is gradually recovering. In the United States, the twin dragsof lower oil prices and a stronger dollar appear to be fading and the outlook is brightening. Europe, which has long been a source of risk, looks to be stabilizing, with increased monetary policy support helping to combat deflation. A potential messy exit of Greece from the eurozone is a key source of risk and is holding back investor confidence, but our view is that we should see at least a temporary deal to prevent that from happening.

Despite an abundance of negative factors, U.S. equities have held their ground so far this year. The main headwind for stock prices has been the deteriorating earnings environment, and while we expect a period of soft earnings to persist, the longer term outlook does look brighter. Equity valuations may look a bit stretched, but we do believe that they look attractive compared to government bond markets. Assuming global economic activity continues to improve, we believe there should be further room for equities to advance.

1 Source: Morningstar Direct, as of 4/17/15 2 Source: Standard & Poor’s 3 Source: Bureau of Labor Statistics

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip

index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc. ©2015 Nuveen Investments, Inc. All rights reserved.