The decline in oil prices since the summer of 2014 continued throughout the first quarter, as oil supply surpassed demand and we saw substantial price declines. This is of particular interest to municipal bond investors, as many US state and local budgets have a substantial dependence on oil production and exploration revenue, and lower oil prices can influence economic growth and inflation, which can affect Treasury and municipal yields.

Falling oil prices typically signal that the global economy isn’t growing fast enough to absorb oil production and can also produce investor anxiety over the credit quality of municipalities whose economies depend on the energy sector.

Municipalities may potentially see a decline in employment and revenues due to falling oil prices, but its impact can differ between state and local governments. Conversely, state and local governments can benefit as lower oil prices and related gasoline prices increase consumer spending, and in turn, increase sales taxes and boost the economy.

Risk varies by state

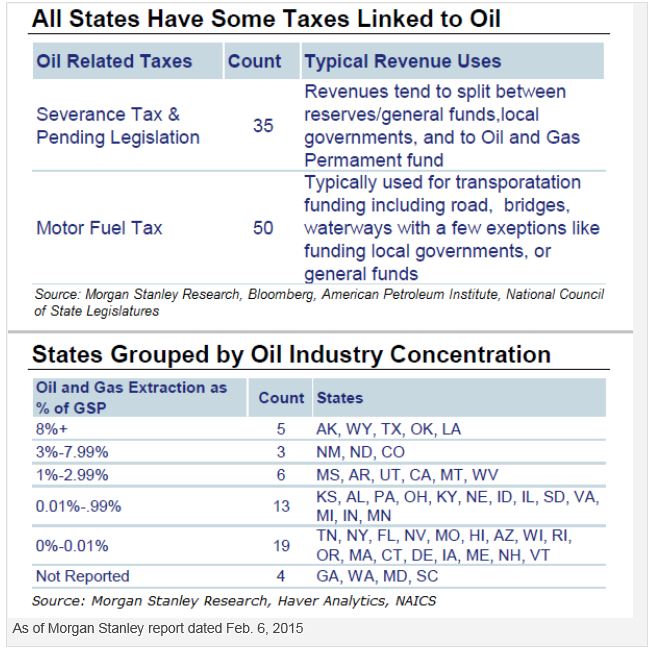

While states with high levels of oil production are at risk for potential weakening of their overall credit quality, state reliance on oil is diverse. The following is a summary of the impact lower oil prices can have on several oil-reliant states.

Alaska — Levies no income or sales tax on residents, but relies primarily on oil and gas revenue to fund operations. While lower oil revenues are beginning to result in fiscal pressure, the state has a considerable amount of reserves sufficient enough to provide a buffer from its structural imbalance.

Texas — The oil and gas industry has been the primary driver of Texas’ growth in recent years, but its economy is large and diverse. The diversity of its economy and sound financial profile is able to protect the state from fluctuations in oil.

Oklahoma — Tends to use its gross production revenues to feed its reserves and fund capital projects, reducing the general fund reliance on oil revenues, while providing for a cushion during times of economic downturns. While the state can face revenue shortfalls due to a decrease in oil prices, these shortfalls appear to be manageable.

Louisiana — With the drop in crude prices, Louisiana has a lot less room to maneuver and further rating revisions could be likely.

Wyoming — Receives 39.7% of its total state tax collections from oil severance taxes.1 According to the state, a $5 decline in oil prices results in a $35 million decline in state annual revenue collections.

The potential benefits for less oil-reliant states

Offsetting the decline in oil-related revenue is the increased consumer spending that is typically associated with a decline in oil prices. In many ways, falling oil prices can mimic tax cuts by transferring cash to the consumers due to an increase in discretionary spending. For states with less reliance on the energy industry, this would boost sales tax revenues and financial flexibility.

For municipal bond funds that primarily invest in revenue bonds, the drop in oil prices could result in a significant tailwind, particularly for bonds backed by revenues from toll roads, airports, electric utilities, airlines and sales tax bonds in cold weather states where gas/oil consumption is a large part of consumer expenditures.

1 Source: The National Association of State Budget Officers (NASBO)

Important information

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/ or interest.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.All data provided by Invesco unless otherwise noted.

©2015 Invesco Ltd. All rights reserved.