“You asked me what’s going to happen...I don’t know what’s going to happen. I regard it all as very weird...if interest rates go to zero, and all of the governments in the world print money like crazy...and prices are going down? Of course I’m confused. Anybody who’s intelligent and is not confused doesn’t understand the situation very well. I think in fact that, if you find it puzzling, your brain is working correctly.”

Charlie Munger, Vice-Chairman of Berkshire Hathaway Chairman of Daily Journal Corporation

Charlie Munger, firmly ensconced in the investor hall of fame, remains, at age 91, one of our favorite purveyors of worldly wisdom on subjects investment related and otherwise. He is also known to be blunt and humorous, offering the above response to a question regarding money-printing, interest rates and unintended consequences at the Daily Journal shareholder meeting a few weeks ago. When a genius like Charlie is confused...then things indeed are confusing.

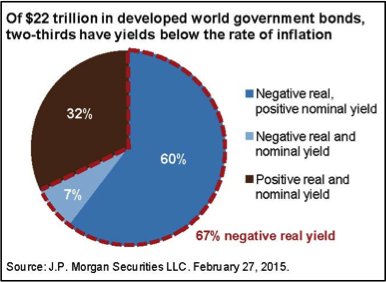

One of the more striking features of the crazy, confusing world in which we live is the appearance of negative nominal interest rates across wide swaths of Europe... something that would have seemed impossible just a few years ago. In fact, just a few years ago at the annual Berkshire Hathaway meeting, Charlie Munger and his partner, Warren Buffett, showed off a trade ticket from ‘08 which demonstrated that someone had bought Treasury bills from them at an implied negative interest rate. The fact that someone was actually willing to accept a negative interest rate in order to obtain the safety of Treasuries was held up as a piece of financial history and a sign of just how crazy the crisis was. Well here we are again, just seven years later and the world looks much crazier.

Instead of a slightly negative yield on an isolated trade during a panic, we now have seven percent of the developed world’s government bonds trading at negative nominal rates. No longer are negative nominal rates confined only to short-term maturities; Switzerland recently issued ten-year bonds with negative yields. As the textbooks are literally being re-written, we hear reports of oddities like the Spanish mortgage linked to (now negative) Swiss rates where the bank currently pays the borrower interest on his balance1! The amazements are not solely confined to the Continent; the U.S. 30-year bond just hit 2.44%, its lowest yield in the history of the Republic, and Mexico just sold a 100-year Euro bond priced to yield 4.2%. To restate, some investor ostensibly trusts that Mexico, 100 years from now, in 2115, will pay them back in a currency introduced into physical circulation thirteen years ago, in 20022. It is somewhat of an open question as to whether the Euro will even exist in 13 years, let alone 100. Wouldn’t you be worried? Prospective investors in Mexican “Centuries” ought also be worried that interest rates, or even worse, inflation, might pick up sometime between now and the 22nd century. Owners of bonds with negative yields and Mexican 100’s likely don’t intend to actually hold until maturity, and so these “investments” to us smack of “greater fool” reasoning and make us nervous...though, like Charlie, we find it difficult to pinpoint the exact direction of approaching danger.

So what do negative nominal rates mean and why are they so crazy? A negative nominal rate means you’ve agreed to receive back less money than you’ve lent out...i.e. I give you ten and you promise to return nine. The issue is not that investors are forced into losing purchasing power; this happens regularly whenever the inflation rate is greater than the nominal rate, as happened in the ‘70’s. It also is likely occurring in your bank account at present. The crazy part is that some bond investors now choose to lend money and not receive it all back, when they could instead do nothing and keep all their money. Why lend 102 Francs to the Swiss government in order to receive back 100 in two years when you could instead put 102 Francs in your sock drawer and in two years still have 102? This is why negative nominal yields are so shocking and were previously thought impossible- why would anyone agree to lose money? The answer becomes more clear when you think about the difficulty of putting 102 million Francs in a sock drawer. Is this really an alternative? In practical terms, one would have to pay for the storage of this money. And one would probably want to hire a guard… and also have insurance just in case. After those costs you’re not going to receive your full 102 million Francs back, even if you try to do “nothing”. Finally, if you change your mind and decide you want to do something else with your money, it would probably take time and considerable effort to retrieve 102 million physical Francs from our giant, fortified sock drawer, deposit them in a bank, transfer them to a broker, and from there buy stocks or other assets. Ownership of a government bond solves all of these problems (safety, ease of convertibility/transfer) at what the market apparently deems a cheaper rate3. Hence, we tend to see those negative nominal interest rates as actually being zero, minus a convenience fee. If rates do get much lower, perhaps we will see a bull market in Scrooge McDuck-like vault building.

Another area of market attention is the energy sector, which continues to be affected by low oil prices. Given our contrarianism and how much oil/energy stocks have fallen, why haven’t we initiated a new energy position? Simply put, while today’s oil price may one day prove to be a bargain, we see evidence that oil and energy stocks are not exactly contrarian plays. This phenomenon is perhaps best illustrated in the words of an investment manager who was quoted as saying, “We continue to see significant client interest in the energy sector. We think it is a great contrarian play.” Clearly the speaker doesn’t understand what it means to be contrarian. Reports of investment houses raising energy-specific funds abound. Anecdotally we encounter non-Wall Street types who express great interest in establishing energy positions. The contention that going long energy is actually a consensus play is supported by the chart below showing that, despite the value of the energy sector being lower than in the recent past, assets have been flowing into energy ETFs since oil’s defenestration. Against this backdrop, we don’t think energy is currently a contrarian play, and remind readers that we didn’t always live in a 100-dollar-a-barrel world, and might not return to one for a long time, if ever.

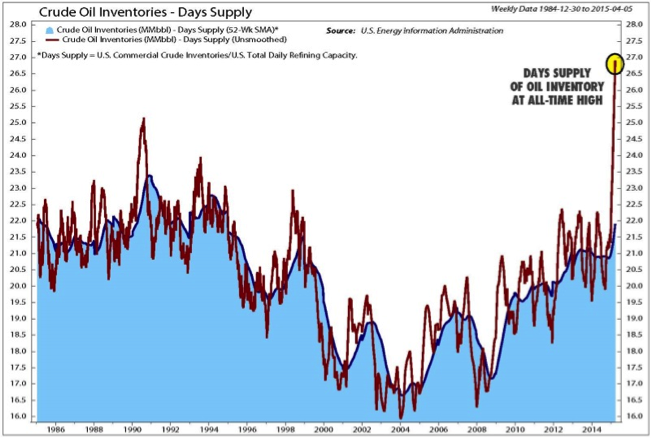

While we caution that anything could happen, we think it is probably worthwhile to wait before placing further energy bets. Banks are just now starting to re-assess the borrowing bases for energy companies, which could cut off their operating life blood and force them to sell assets, which would act as a force depressing prices. Companies trying to make it through the cycle will continue to try and squeeze every penny of cost savings out of their operations, and therefore out of their suppliers and servicers as well. In the meantime, domestic stockpiles of oil continue to be at their highest levels just about ever, indicating continued oversupply.

Just because energy isn’t contrarian, doesn’t mean it won’t be a good investment. Indeed, we have identified a number of potentially promising positions, but we will be more likely to pull the trigger and invest if we hear others swearing off the sector forever instead of excitedly discussing the “inevitable” recovery.

Today there is no shortage of commentaries on the Fed regarding the supposed upcoming rate raising cycle. You can divide these largely into two camps:

- Camp 1: the Fed has already left rates too low for too long...for too long have financial risks and dangerous excesses been building in the system. As debt, encouraged by low rates, continues to expand4, it will be more difficult to raise rates without tipping over a fragile system.

- Camp 2: The Fed is hyper-aware of 1937 when it raised rates too far too early and cut-off the nascent recovery before it could sustain itself, thereby extending the Great Depression for a number of years. Therefore, the Fed will be very cautious when it comes to raising rates.

We are inclined to agree with camp 1 about what the Fed probably ought to do, but on the not-to-be-confused question of what the Fed actually will do, we find ourselves in camp 2.

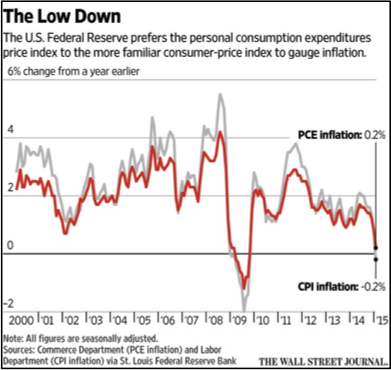

We often hear people tie the Fed’s rate considerations to debt servicing burdens (both private and public), or currency exchange rates, or bubbles, or overall financial fragility. These may all be important concerns, and the Fed has even occasionally acknowledged they are important concerns, but when it comes right down to it, the Fed has a dual mandate: full employment and price stability (low inflation)...and on that they will focus. Inflation, as measured by the Fed, is still low as the chart at right shows5.

Perhaps even more important in understanding Fed actions than its mandates are its models. The Fed may talk about many things, and care about them as well, but its core economic models still propose that there is a basic trade-off when it comes to rates: low rates bring the benefit of higher employment and the cost of higher inflation. At its core, existing economic theory (which we suspect may need some updating in coming decades) basically lists inflation as the only drawback to low interest rates.

Hence, if the Fed doesn’t fear a prolonged period of low rates, and doesn’t feel pushed by inflation, any rate raise in June/Sept might be followed by no further raise for some time. Indeed, those who say something along the lines of “rates are so low they must go up” may be surprised to hear that long-term U.S. Treasury yields remained below three percent for 22 years, from 1934 to 1956...notably, during a time when policymakers were trying to reduce the national debt (a climate that, while not currently present, isn’t hard to imagine). Given all this, (not to mention as we’ve cited in previous letters that stocks have tended to do well during the first few steps of a rate rising cycle) if the stock market reacts negatively to a first rate hike it might in fact be a buying opportunity.

Though our strategy is far from based on predicting Fed rate cycles, the fact that we believe rates are likely to stay “lower for longer” presents a dilemma. The lower rates remain, the more risk builds in the system, increasing the danger and severity of a financial crash or other adverse event. On the other hand, the longer rates remain low, the more stocks become acclimated to low rates and associated higher valuations, and rise in price. We have so far elected to prepare for risks ahead of time, opting for lower risk positions, with a focus on positive absolute returns, despite potentially negative relative returns in the meantime.

After a six-year bull market, equity index returns have received a lot of attention. Many of those pursuing an absolute return orientation, including Knightsbridge, have underperformed as they sought to limit downside risk in the face of this raging bull. Hindsight Capital (which has never had a down year, by the way) is only now informing us that a focus on risk and limiting downside was ill-suited to the recent past. This result begs the question: what exactly is an absolute return orientation and why is it worth pursuing?

There are two answers that we would give. The first is that in the long run, relative performance is indeed what matters, but a focus on absolute performance in the short run usually gets you there best. A focus on absolute performance allows one to safely ignore overpriced assets. Anyone who was primarily concerned with relative performance would invariably have invested in technology stocks in the 1996-2000 run up to the dot-com bubble burst, thinking that any return below the index average represented a failure. Many value investors, ourselves included, ignored increasingly insanely priced technology stocks, to the great detriment of their relative performance. Knightsbridge’s performance in 1997, 1998, and 1999 trailed the market by 13%, 3.5%, and 3.5% respectively. However, this gap was more than made up by our 24% outperformance in 2000. It was the focus on absolute performance, the contentedness with solidly, but not wildly, profitable bets, that helped us to avoid the temporarily lucrative, but to our judgement dubious, game of betting on unproven technology at unprecedented valuations. The focus on absolute performance ultimately helped achieve relative outperformance.

The other lens through which to view an absolute performance orientation is risk. Applied to the same historical episode of the late 90’s, despite the great returns already experienced by others (or rather, because of them) the valuations of stocks were too high, indicating too much risk. Similarly today, and for the past few years, we have viewed the world as having a great deal of risk, and have intentionally undertaken some portfolio positions designed to move less with the overall market, and more according to their idiosyncratic situations. While these positions by and large produced positive returns, they have hurt our relative performance.

We currently sit with a high (near 30%) cash position in most accounts. This position was not undertaken due to our view of overall market risk, though it is consistent with such a view. Simply put: while we are uncomfortable with a cash position this high, we are more uncomfortable with putting cash into the valuations of the individual security alternatives with which we find ourselves faced. Some of our stocks hit our price targets, (Sealed Air, Motorola Solutions), where we felt it was no longer worth the risk to maintain a position. We find it natural and helpful that in the advanced stages of bull markets, more stocks hit our views of full valuation and are sold. Other stocks were acquired (Exelis) or advanced to a price too expensive for our tastes before we were able to establish full positions (Vectrus). Mostly, we haven’t been able to find a sufficient number of stocks with appropriate risk/reward balances to allow us to deploy the cash freed up through sales; the cash position is largely an artifact of this reality.

We continue to look for positions, both inside and increasingly outside of the United States. Our goal has long remained and continues to be beating the market over the long term, including during down periods6. We do not expect to be able to do this on an annual basis. Though we feel the unrelenting pressure to just “get invested” in a bull market, we prefer keeping money on the sidelines to making a bet in which we lack confidence. When we find ourselves too anxious to deploy capital into subpar investments, for support we look to the words of wise old Charlie Munger, “There are worse situations than drowning in cash and sitting, sitting, sitting. I remember when I wasn’t awash in cash – and I don’t want to go back.”

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Lest anyone get too excited about trying to obtain the same deal, it should be noted that the principal of the loan has actually soared from the borrower’s perspective because it is denominated in the strong Swiss Franc.

2 It was introduced electronically three years before that in 1999.

3 In addition to convenience, some actors (banks) might agree to negative government bond yields because new international banking regulations make it more limiting for banks to hold cash, hence banks would seem to be saying regulatory freedom gained by holding government bonds is worth the cash cost of negative return.

4 As noted in previous letters, we’ve already surpassed previous debt heights.

5 We would add that inflation measured in another manner could indeed be very high. The prices of financial securities of all types, and hyper-luxury goods such as mega-yachts, mega-jets, and exclusive real estate have all increased substantially. Perhaps this isn’t surprising given that the Fed used all its newly printed money to buy bonds, which are by and large owned by the wealthy (or by institutions that are owned by the wealthy). What would a wealthy person who was previously saving their money in bonds do when that bond was turned back into cash? Why, either continue to save it (i.e. buy some other financial asset) or buy something they didn’t have before (a luxury item). But this line of speculation is best left for another day.

6 There have been no ten percent corrections for three and a half years.