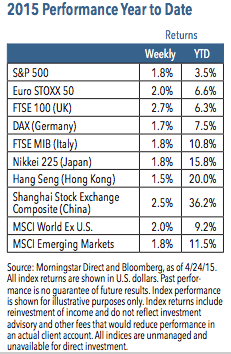

Investors mostly focused on the positives last week. Corporate earnings generally beat expectations and merger and acquisition activity remained solid. Despite disappointing economic data, this trend reinforced the perception that the Federal Reserve would hold off on rate hikes for the time being. The turmoil in Greece rattled investors, but remains relatively contained. For the week, the S&P 500 Index rose 1.8%, with the technology and telecommunications sectors leading the way.1 Energy and consumer staples were the chief laggards.1

Weekly Top Themes

1. Earnings are exceeding lowered expectations, but the energy sector remains a drag. With about 40% of the S&P 500 companies reporting results, earnings are beating expectations by 5.5%, while revenues are missing by around 1%.2 Were it not for the energy sector, earnings would be up close to 8%.2

2. We are not expecting significant changes from this week’s Fed meeting and believe rate hikes will begin in September. The Fed will likely acknowledge a first-quarter slowdown in economic growth and the labor market. However, with core inflation starting to creep higher and financial conditions looking good, the Fed should still be on track to raise rates later this year. When it does so, we think the central bank will be slow and deliberative, as the fed funds rate climbs gradually to 1% or slightly higher.

3. Global monetary policy remains in an easing mode. Outside of the United States, policy easing continues with the impact varying by country. In China, for example, we do not believe policy support will accelerate growth, but it should moderate the slowdown. In Europe, the massive quantitative easing program should boost growth.

4. Equities have accelerated since the end of the global financial crisis despite disappointing global economic growth. A combination of significant deleveraging and a global collapse in productivity has limited economic growth over the past several years despite unprecedented stimulus. Nevertheless, equities have enjoyed an extended bull market mainly because slow wage growth pushed earnings higher and an abundance of liquidity propelled investors into higherrisk assets.

5. The bull market in U.S. stocks recently celebrated its sixth birthday, but age alone will not derail the advance. There is no magic number of years at which bull markets end. Fundamentals, the economic backdrop and investor sentiment all matter far more than an arbitrary age. We believe these factors point to more time and more price advances for this bull market.

Economic Growth and Earnings Should Regain Traction The first few months of the year were marked by disappointing economic data and deteriorating earnings expectations that put U.S. equities into a choppy holding pattern. We expect economic growth to improve from here as the temporary effects of a harsh winter fade and consumer spending gradually accelerates. Earnings have been hit by the precipitous drop in oil prices and pressure from the rising U.S. dollar. In our view, profit growth should begin to improve as stabilizing oil prices settle the energy sector and non-energy earnings reflect the delayed benefit of cheaper oil. Assuming the advance in the dollar levels off and global growth continues to firm, we forecast a brighter environment for earnings in the coming months.

Such a backdrop should allow equity prices to advance, but the road ahead will be rocky and not without risks. The threat of a Greek debt default and a messy exit from the eurozone is much in the minds of investors right now. The ongoing negotiations may cause market turmoil, but we believe the most likely outcome is some sort of compromise that leaves the eurozone intact. The pending start of the Fed’s rate hike cycle is likely to result in increased bond yields and heightened volatility in the equity market. But we don’t believe this shift will derail the bull market given a healing economy and an accommodative global monetary policy environment. We think the balance of risks remain favorable for equities and continue to advocate a pro-equity, pro-growth investment stance. ▪

1 Source: Morningstar Direct, as of 4/24/15

2 Source: RBC Capital Markets

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.