Talk of an unsustainable surge in mergers and acquisitions is premature. The current level of activity suggests that corporate managers will continue to buy rather than build.

Some buzz has developed of late on the subject of mergers and acquisitions (M&A). A recent piece in Business Insider is indicative. It talks about an M&A surge, and identifies it as a sign of a bubble. Such talk is wrong on two counts. The statistics show no such surge, and even if there were, it would hardly signal a toppy market. On the contrary, it would suggest that values are still attractive enough to impel decision makers to buy rather than to build. Matters would look ominous if there were a surge in initial public offerings (IPOs), but there is certainly no sign of that.1

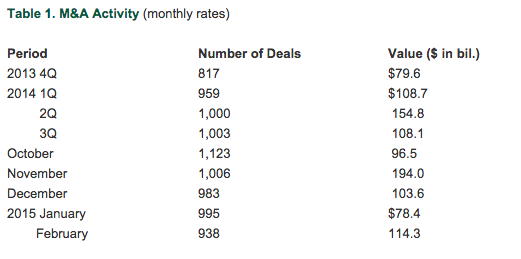

To be sure, M&A activity has picked up. That is only typical of ongoing cyclical recoveries. The upward trend, however, could hardly be characterized as a “surge.” Table 1 lays out the figures. The number of deals, 938 last February (the most recent month for which data are available) is up a noticeable but hardly overwhelming 4.5% from February 2014. It is actually down 4.6% from last December and off 10.2% from a crest in January 2014. On this basis, one might even see a falling-off in M&A activity. The value of deals, at $114.3 billion in February, is probably more important and on a stronger uptrend. It is up more than 25% from the $154.3 billion averaged in February 2014 and up 10% from last December. But even here, the figures are far from overwhelming. February’s measure is, after all, still 41% below the strikingly high $194.0 billion in November 2014. Rather than play too close a game with the statistics, a fair judgment might conclude that M&A activity, both deals and volumes, are about holding their own after a real surge earlier in 2014.2

There is some sign that a pickup will take place. In a recent CNBC poll, some 56% of companies said that they plan an acquisition in the coming year, up from 40% last October and the first time since 2010 that more than half plan to do something. But even if such plans were to generate a surge later this year, it would make a bullish argument for equities, not the bearish one accompanying much of this recent buzz.3

M&A, quite simply, is a vote of confidence in market values and the future generally. Companies buy each other when they see a reason to expand and when other firms look attractively cheap. The same goes for private equity, which is no less in the acquisition business than corporations. If these decision makers saw stocks as expensive, they would pursue their expansion with direct investments in new equipment, premises, and in a hiring program. Since they are buying these days and doing relatively little building, they have effectively announced that stock values still make a purchase the more attractive way to expand. To be sure, managements sometimes get swept up in a bubble and purchase at exorbitant prices. But such mistakes, even if sometimes dramatic, are more the exception than the rule. The continued broad flow of M&A activity now, even if a surge fails to materialize, announces that this “smart money” still thinks stocks are cheap.

Initial public offerings would tell a very different story. Unlike M&A, an increase in these would announce that managements and investment bankers see prices as high, a time to get a premium price for the firm. Of course, people make mistakes from time to time, but a general run of IPOs would raise a red flag about market pricing and valuations. Here, patterns confirm that few decision makers see matters this dangerous way. According to the latest statistics, IPOs have actually fallen off this year. First quarter figures show only 34 deals valued at $5.4 billion, down from 68 deals valued at $16.2 billion in the fourth quarter last year and 64 deals valued at $10.6 billion in 2014’s first quarter. In fact, the most recent quarter is the slowest in two years, hardly a sign that owners or investment bankers see any urgency to cash in on high prices.4

Source: FactSet.

Some of this misplaced buzz may reflect the sudden and still novel growth of overseas financing. It seems that because the European Central Bank has flooded the eurozone with liquidity, the resulting low interest rates and bond yields there have begun to attract many American borrowers. Though data is far from comprehensive, what figures are available indicate that so far this year American companies have raised nearly €30 billion on European markets in some 24 deals, up from eight deals and €7 billion on average last year. Since they have no doubt brought some of this money home to support their acquisition strategies, some observers might feel a strangeness about today’s M&A activity, enough to distract them from more favorable fundamental interpretations. But beneath novelty, it hardly looks ominous. On the contrary, it really just announces that U.S. securities and markets will gain from the liquidity being created in Europe even as the U.S. Federal Reserve begins, very tentatively and very gradually, to step back from its policy of pouring liquidity on markets.5

1See, Jim Edwards, “If You’re Looking for Signs of a Bubble, IPOs and M&As Both Hit New Highs,” Business Insider, October 3, 2014.

2Data from FactSet.

3See, “Corporate Deals Appetite Hits Five Year High,” CNBC, April 13, 1015.

4 Renaissance Capital IPO Research, “2015 IPO Market Off to a Slow Start,” Seeking Alpha, March 31, 2015.

5 Eric Platt, “U.S. Companies Sell Record Euro Debt,” Financial Times, March 23, 2015.