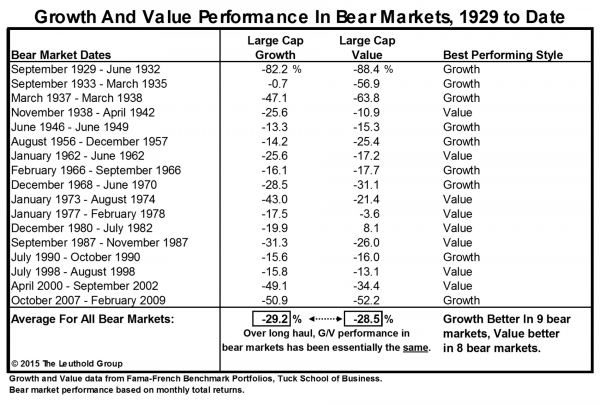

Will Rogers said, “It isn’t what we don’t know that gives us trouble, but what we know that ain’t so.” Investors have long “known” that Value stocks provide a safer place to hide than Growth stocks during a cyclical bear market, an assumption probably based on: (A) experience since the early 1970s; and (B) common sense, in that speculative investments with low price tags and low expectations should be expected to suffer less when animal spirits deflate. But it hasn’t always been so:

· During the nine bear markets from 1929 to 1970, Large Cap Growth generally proved to be the better bear market play, falling less than Large Cap Value in seven of the nine cyclical bear markets of that era. Value earned its defensive reputation during the seven bear markets of the 1973-2002 period, when it outperformed Growth (and usually by a wide margin) six times, and basically matched Growth once (1990 bear market).

· During the great “egalitarian” bear market of 2007-2009—in which all geographies, styles, sectors and capitalization tiers suffered comparatively equal beatings—Large Growth held a narrow performance edge (falling –50.9% on a total return basis, versus –52.2% for Large Value).

· Averaging losses for the 17 cyclical bears from 1929 through 2009 yields near-identical results: Value’s average decline has been –28.5%, with Growth stocks falling –29.2%.

Table 1

· Is there anything that might help us determine which style will play better defense in the next bear market? We think so… read on.

One of the factors complicating analysis of Growth and Value cycles is that the sectoral composition of each style varies significantly over time. For example, Large Growth in the early 1990s was dominated by Consumer Staples and Health Care (then considered “unit-growth” stocks), but morphed into mostly a Technology play by the end of the decade. These compositional shifts are difficult to capture through the modeling process, but we think we’ve found a short-hand way to measure them with the use of style betas.

Reviewing rolling 5-year betas for Large Value and Large Growth, there’s now less mystery to the multi-decade period (1930s-1960s) in which Growth stocks proved the better bear-market hiding place. Growth stocks exhibited a much lower beta throughout most of the 1930-1970 period—with an average 5-year beta over that period of 0.94, compared with an average of 1.20 for Value. Value played poor “defense” during the bear markets of that era for the simple reason that it wasn’t defense.

· Betas flipped during the 1975-2005 period, with Value’s beta plunging far below that of both Growth and the market itself (i.e., below 1.0). Value’s superior bear market performance during this era makes perfect sense in light of this new information.

· The last decade saw yet another flip, with the onset of the commodity and housing booms sending the Large Value beta sharply higher. The two betas have begun to converge in the last several months, but if a bear market were to erupt later in 2015 (which wouldn’t surprise us), we think Growth stocks will prove the better place to hide.

Chart 1

© 2015 The Leuthold Group