California Dreaming (of Rain)

This past quarter saw California announce unprecedented water rationing as their record drought led to the lowest snowfall in decades. Meanwhile, the East Coast tallied a record snow season. Just as the tides wax and wane, and the rain comes and goes, so go the commodity cycles and passion of investors for sectors of the market. The draught of investor interest in MLPs that began with the decline in commodity prices in mid-2014 spilled over into the beginning of 2015. After declining 13.7% from its peak in August through the end of 2014, the Alerian MLP Index declined another 9.0% the first two weeks of January. However, once the oil price stabilized in January, investors again refocused on MLP business fundamentals and unit prices stabilized - the Alerian MLP Index performance was up 4.0% from its trough in mid-January to quarter end.

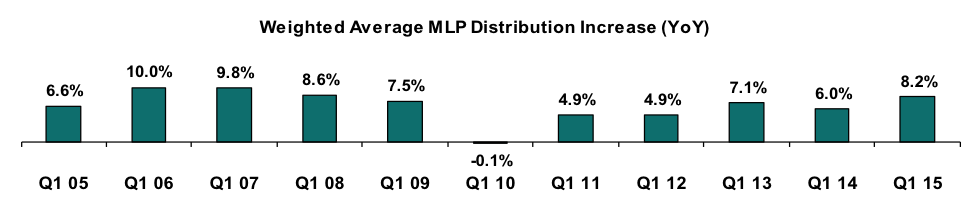

We view the recent sell off of MLPs/midstream energy infrastructure companies as a buying opportunity. Our long-term evaluation of the total return prospects of these companies is very good, especially on a risk adjusted basis. Lower interest rates improved the attractiveness of MLPs for yield oriented investors during the quarter. At quarter end, the yield of the Alerian MLP index stood at 6.1%, while the yields on most other yield alternatives had declined in the quarter. MLPs continued to increase their distributions in the quarter at a healthy rate, underscoring our contention that distribution increases in the current environment are not much affected by lower energy prices. The weighted average distribution increase in the first quarter was 8.2% over the prior year, above what it has been in recent periods.

Source: Eagle Global Advisors

Lower Energy Prices Create M&A Opportunities

Last quarter we predicted that lower energy prices might lead to an uptick in acquisition activity, and we saw several large transactions in the first quarter. Not surprisingly, Kinder Morgan was first to act with their $3 billion acquisition of Hiland Partners. Hiland Partners, a privately held company, was founded by Harold Hamm, the high profile CEO of Continental resources. The acquisition gives Kinder a footprint of crude oil infrastructure in the Bakken shale where they previously had no assets. In a transaction similar to Kinder Morgan’s roll-up of its MLPs last quarter, Energy Transfer Partners (ETP) offered to acquire the remaining shares outstanding of Regency Energy Partners (RGP) in an $18 billion deal including the assumption of debt. ETP already owned roughly 22% of the shares outstanding in RGP. RGP shareholders are scheduled to vote on the deal April 28th and if the deal closes, Energy Transfer Equity, the general partner of ETP and RGP, will be able to simplify its general partner ownership of both entities into one.

The first quarter saw a healthy pace of MLP equity issuance relative to 1Q14, likely factoring into the weak performance of the group. We tracked close to $4 billion of follow-on equity offerings with large issuances coming from Plains All American Pipeline, EQT Midstream Partners, Sunoco Logistics, and Enbridge Energy Partners. It was widely speculated that the purpose of the $1 billion offering by Plains All American Pipeline was to create a war chest to finance a large transaction. However, the company has yet to engage in any such activity despite public comments from CEO Greg Armstrong that he would like to be opportunistic with distressed asset acquisitions. EQT Midstream Partners issued over $700 million of equity to finance its large purchase of West Virginia Marcellus gathering assets from its parent EQT Corp. Sunoco Logistics and Enbridge Energy Partners raised $564 million and $294 million respectively to fund organic projects. In addition to the $2 billion that Sunoco Logistics will spend in 2015 on organic projects, the company will also likely invest in the large Dakota Access Bakken pipeline that will be constructed by its general partner Energy Transfer Partners.

MLPs were not the only ones active in raising equity capital this quarter; the independent Exploration and Production companies raised close to $13 billion in equity capital. From the perspective of the midstream companies however, this can be noted as a positive. With better balance sheet flexibility, E&P companies overall will likely maintain their current capital spending programs helping to insulate the utilization of the midstream assets tied to their production facilities. We believe that many non-core midstream assets exist at the E&P companies that could come up for sale, however, the urgency to effect such transactions has been muted somewhat. With upcoming borrowing base redeterminations and unsupportive commodity pricing likely hurting liquidity and cash flow, E&P companies looked to bolster balance sheets to help reduce leverage.

While the high yield markets have been incrementally more difficult for E&P companies to tap, we have seen a few deals executed at reasonable rates. Rice Energy and Consol Energy were able to raise $400 million at 7.25% and $500 million at 8% respectively. Both companies have existing underlying MLPs that own infrastructure assets in support of the parent’s production interests. The incremental debt and equity capital likely delays broad-based M&A and distressed asset sales to some extent as producers try and weather the lower commodity price environment.

On the flip side, E&P sponsors of existing MLPs made good use of the symbiotic relationship during the quarter. Enlink Midstream Partners made a $600 million acquisition of a privately held company, and shortly after they bought logistics assets in the Port of Victoria vicinity for $210 million from their parent and general partner Devon Energy. We already referenced EQT Midstream Partners’ $1 billion purchase of gathering assets from its producer sponsor. In addition, Western Gas Partners was able to purchase an interest in its sponsor, Anadarko Petroleum’s Delaware Basin gathering assets for relatively advantageous terms which included no up-front consideration and a future payment based on the cash flow profile of the asset at its maturity in 2020.

IRS Lifts Moratorium of PLRs

A positive regulatory development during the quarter was the lifting of the moratorium on new Private Letter Rulings (PLRs) for MLPs by the IRS. A PLR is desired when a MLP wants to acquire an asset that does not obviously fall under the “natural resource exception” that has governed MLPs. The moratorium had served as a damper to a number of companies that wanted to include non-traditional assets such as water handling, petrochemical facilities, and timber related assets in MLP structures. The IRS announced it will release standards clarifying MLP qualifying income soon. While the IRS said it would start processing PLRs, it gave no guidance on when companies could expect them to act on their submissions.

Long Term Outlook: Positive

We continue to have a positive long-term outlook for MLP/midstream energy infrastructure total returns. Valuations, after the 18% decline in the index since August of last year, are more attractive on both an absolute and relative basis. The average MLP yield is now close to 6.1% and spreads of MLP yields versus Treasuries, REITS, corporate bonds, and high yield bonds have widened out to historically large levels. Despite lower commodity prices, we still expect high single digit distribution growth from our portfolio of companies. Combined with current distribution yields, MLPs should still have the potential for, what we believe to be, attractive total returns.

Confounding all the pundits, bond yields continue to drop, and the 10-year U.S. Treasury bond is yielding about 1.9% as of this writing. This continues to fuel a demand for yield in the markets, and other yield oriented investments like REITs, utilities, and most types of higher yielding bonds. MLPs/midstream energy infrastructure companies continue to offer a high, tax-advantaged yield with growth and we believe these attributes will continue to attract favor with investors. This demand is long term as we believe that the demographic trend of an aging population will result in a wider investor base seeking out the income generation of the MLP/midstream asset class. When inflation returns, the ability of MLPs to grow their distribution and allow investors to stay ahead of inflation is a further attraction.

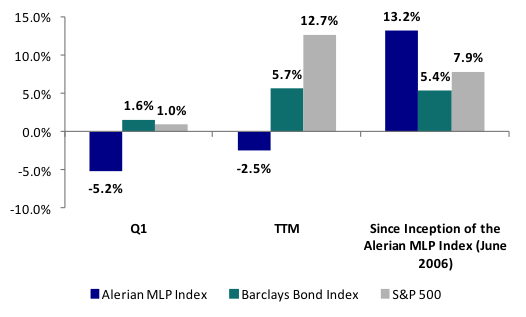

As a result of the recent performance, the MLPs have trailed U.S. stocks and bonds in the past quarter and trailing twelve months (TTM). However, for longer periods MLPs have significantly outperformed U.S. stocks and bonds as shown in the chart below.

Performance through March 2015*

*Annualized for periods greater than one year.

The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Indices do not include fees or operating expenses and are not available for actual investment. Indices presented are representative of various broad base asset classes. They are unmanaged and shown for illustrative purposes only. Data from Alerian and Bloomberg. Past performance is not indicative of future results. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

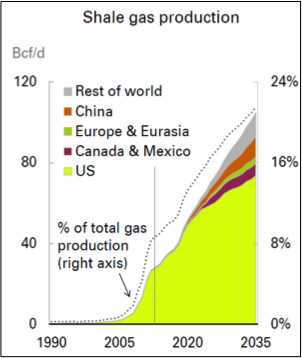

Following the sharp drop in oil and gas prices last year, many are questioning the forecasts of growth of U.S. produced volumes of oil and gas in the coming years. Therefore, we found BP’s February presentation of its long term outlook for energy particularly interesting. Driven by a global shift to use natural gas for power generation, BP sees significant growth in global demand for natural gas in the next decades; to meet this demand, it forecasts that U.S. shale gas production growth will rise an average of 4.5% per year for the next 20 years.

For oil and natural gas liquids, BP expects world demand to grow from approximately 92 million barrels per day (bpd) today to 111 million bpd by 2035; of this 19 million bpd increase, BP sees almost 50% or 9 million bpd coming from North America: 6 million bpd from the U.S. and 3 million bpd from Canada. If these forecasts are anywhere close to the mark, the need for new midstream infrastructure in North America should continue for decades.

|

David Chiaro

Co-Head of MLP Strategies for Eagle Global Advisors, LLC

Co-Advisor of the Eagle MLP Strategy Fund

Disclosures:

Investors should carefully consider the investment objectives, risks, charges and expenses of the Eagle MLP Strategy Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 1-888-868-9501 or visiting www.eaglemlpfund.com. The prospectus should be read carefully before investing. The Eagle MLP Strategy Fund is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. This is an actively managed dynamic portfolio. There is no guarantee that any investment (or this investment) will achieve its objectives, goals, generate positive returns, or avoid losses. The information provided should not be considered tax advice. Please consult your tax advisor for further information. Eagle Global Advisors, Princeton Fund Advisors, LLC and Northern Lights Distributors, LLC are not affiliated.

A master limited partnership (MLP) is a limited partnership that is publicly traded on a securities exchange. It combines the tax benefits of a limited partnership with the liquidity of publicly traded securities. To qualify for MLP status, a partnership must generate at least 90 percent of its income from what the Internal Revenue Service (IRS) deems "qualifying" sources, generally relating to the production, processing or transportation of natural resources, such as oil and natural gas.

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor's using a float-adjusted market capitalization methodology.

A real estate investment trust (REIT) is a security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors a regular distribution, as well as a highly liquid method of investing in real estate.

Risk Factors:

Credit Risk: There is a risk that note issuers will not make payments on securities held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes.

Distribution Policy Risk: The Fund’s distribution policy is not designed to guarantee distributions that equal a fixed percentage of the Fund’s current net asset value per share. Shareholders receiving periodic payments from the Fund may be under the impression that they are receiving net profits. However, all or a portion of a distribution may consist of a return of capital (i.e. from your original investment). Shareholders should not assume that the source of a distribution from the Fund is net profit. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares.

ETN Risk: ETNs are subject to administrative and other expenses, which will be indirectly paid by the Fund. Each ETN is subject to specific risks, depending on the nature of the ETN. ETNs are subject to default risks. Foreign Investment Risk: Investing in notes of foreign issuers involves risks not typically associated with U.S. investments, including adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards.

Interest Rate Risk: Typically, a rise in interest rates can cause a decline in the value of notes and MLPs owned by the Fund.

Liquidity Risk: Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations.

Management Risk: Eagle’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests may prove to be incorrect and may not produce the desired results. Additionally, Princeton’s judgments about the potential performance of the Fund’s investment portfolio, within the Fund’s investment policies and risk parameters, may prove incorrect and may not produce the desired results.

Market Risk: Overall securities market risks may affect the value of individual instruments in which the Fund invests. Factors such as domestic and foreign economic growth and market conditions, interest rate levels, and political events affect the securities markets.

MLP Risk: Investments in MLPs involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. MLPs are generally considered interest-rate sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns. Depending on the state of interest rates in general, the use of MLPs could enhance or harm the overall performance of the Fund.

MLP Tax Risk: MLPs, typically, do not pay U.S. federal income tax at the partnership level. Instead, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law or in the underlying business mix of a given MLP could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in such MLP being required to pay U.S. federal income tax on its taxable income. The classification of an MLP as a corporation for U.S. federal income tax purposes would have the effect of reducing the amount of cash available for distribution by the MLP. Thus, if any of the MLPs owned by the Fund were treated as corporations for U.S. federal income tax purposes, it could result in a reduction of the value of your investment in the Fund and lower income, as compared to an MLP that is not taxed as a corporation.

Energy Related Risk: The Fund focuses its investments in the energy infrastructure sector, through MLP securities. Because of its focus in this sector, the performance of the Fund is tied closely to and affected by developments in the energy sector, such as the possibility that government regulation will negatively impact companies in this sector. Energy infrastructure entities are subject to the risks specific to the industry they serve including, but not limited to, the following: Fluctuations in commodity prices; Reduced volumes of natural gas or other energy commodities available for transporting, processing, storing or distributing; New construction risk and acquisition risk which can limit potential growth; A sustained reduced demand for crude oil, natural gas and refined petroleum products resulting from a recession or an increase in market price or higher taxes; Depletion of the natural gas reserves or other commodities if not replaced; Changes in the regulatory environment; Extreme weather; Rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities; and Threats of attack by terrorists.

Non-Diversification Risk: As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of one or more issuers. Small and Medium Capitalization Company Risk: The value of a small or medium capitalization company securities may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. Structured Note Risk: MLP–related structured notes involve tracking risk, issuer default risk and may involve leverage risk. Mutual Funds involve risk including possible loss of principal.