Are We the Stranded Asset?

(and other updates)

U.S. Secular Growth: Donkey or Racehorse?

As you know, dear reader, I have been hacking on for several years about the downward pressures on U.S. long-term growth prospects. What amazed me two years ago was to see the authorities, including the Fed, estimating a nearly 3% trend for the U.S., which seemed to me then and now as impossible. Negligible growth in population and man-hours offered to the workforce is the most important brake to growth, with a net drop of fully 1% from the pre-2000 trend. Less capital investment and growing income inequality do not help. But the most underappreciated important factor, in my opinion, is the drag on growth from the loss of sustained cheap energy as oil has moved from a $16/barrel 100-year trend pre-1972 to today’s approximate $75/barrel trend price.1 The GFC, in contrast, was a temporary factor and one that I believe (on my own, apparently) was given an exaggerated importance. Given these negative factors, I estimated a few years ago that the U.S. trend line growth for GDP was likely to be no higher than 1.5% a year, and perhaps only 1% for Europe and Japan. Well, wheels turn and estimates are re-estimated: official estimates for the longer-term growth trend of the U.S. have been falling slowly but surely over the last few years to a range from 2% to 2.5%. In the two or three years since 2012, I had expected to see them in the range of 1.5% to 2%.

Well, into this quiet world of creeping adjustment, an IMF paper released in early April of this year acted as an unexpected jolt of excitement as, unusually, estimates tumbled all the way down to 1.5%.2 Wonders never cease. Now, the question is how much will this affect the Fed’s beliefs? Presumably enough to matter. This would be timely because, as you may remember, I have been anxious about the Fed’s whipping our actual 1.5% donkey in the mistaken belief that it was a 3% racehorse. The danger was, as I said, that they would keep on whipping it until either the donkey turned into a racehorse or dropped dead. Death from overstimulation.

Not only has the IMF paper been a necessary gust of reality that might just convince Ms. Yellen that she is indeed dealing only with a humble donkey, but it has also raised some interesting further questions. It made its main point the reduced rate of growth and the ageing of the workforce. How, by the way, does this point, straight from the U.S. Bureau of Census, take over five years to make it into semi-official GDP growth estimates? It then references lower capital investment ratios in a traditional way. Also obvious enough. But what does it leave out? Resource limitations! I like to joke that the only thing that unites Austrians and Keynesians is their complete disregard for the limitations imposed by Spaceship Earth. In their thinking, a dramatic increase in price trend from the old $16/barrel to the new $75/barrel had no effect. Mainstream economics continues to represent our economic system as made up of capital, labor, and a perpetual motion machine. It apparently does not need resources, finite or otherwise. Mainstream economics is generous in its assumptions. Just as it assumes market efficiency and perpetually rational economic players, feeling no compulsion to reconcile the data of an inconvenient real world, so it also assumes away any long-term resource problems. “It’s just a question of price.” Yes, but one day just a price that a workable economy simply can’t afford!

I am still just about certain about three things: first, our secular growth rate in the U.S. is indeed about 1.5% (at least as stated in traditional GDP accounting, wherein expensive barrels of oil increase GDP; perhaps closer to 1% in real life); second, economists move their estimates slowly and carefully in order to stay near the pack and minimize career risk (despite the recent IMF heroics); and third, that we do not like to give or receive bad news and, when in doubt, we tend to be optimistic.

A brief update on the U.S. market: still not bubbling yet, but I think it will

■ The key point here is that in our strange, manipulated world, as long as the Fed is on the side of a strong market there is considerable hope for the bulls. In the Greenspan/ Bernanke/Yellen Era, the Fed historically did not stop its asset price pushing until fully-fledged bubbles had occurred, as they did in U.S. growth stocks in 2000 and in U.S. housing in 2006. Both of these were in fact stunning three-sigma events, by far the biggest equity bubble and housing bubble in U.S. history. Yellen, like both of her predecessors, has bragged about the Fed’s role in pushing up asset prices in order to get a wealth effect. Thus far, she seems to also share their view on feeling no responsibility to interfere with any asset bubble that may form. For me, recognizing the power of the Fed to move assets (although desperately limited power to boost the economy), it seems logical to assume that absent a major international economic accident, the current Fed is bound and determined to continue stimulating asset prices until we once again have a fully-fledged bubble. And we are not there yet.

■ To remind you, we at GMO still believe that bubble territory for the S&P 500 is about 2250 on our traditional assumption that a two-sigma event, based on historical price data only, is a good definition of a bubble.3 (As we like to describe it, arbitrary but reasonable, for it fits the historical patterns nicely.)

■ For the record, probably the best two measures of market value – Shiller P/E and Tobin’s Q – have moved up over the last six months to 1.5 and 1.8 standard deviations (sigma), respectively. So, just as with the price-only series, they are also well on the way to bubble-dom but, clearly enough, not there yet. If we used these value series instead of just price it would add 5-10% to the bubble threshold, further improving my case that the current market still has a way to go before reaching bubble territory. Historically, we have often used the price series as both less judgmental than using measures of value, and as a much fairer comparison with other bubbles (e.g., commodities currencies and housing).

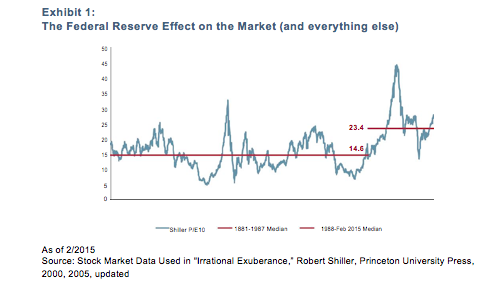

■ Bear in mind that in the Greenspan Era (from 1987 and still running) the market, measured by Shiller P/E, has averaged about 60% higher than it did prior to when the Fed’s habit (as in “addiction”) of pushing the market up in order to get a wealth effect became standard operating procedure (see Exhibit 1). It would be tempting to adjust the “normal” P/E downward for this, and treat it as a temporary anomalous phase, but we do not – we give each year equal weight.

■ Perhaps most importantly, the current economic cycle still seems only middle-aged, despite its measured long duration. For example, there is still plenty of available labor hiding in the participation rate for sure (male labor anyway).

■ It turns out that even the female labor force probably still holds substantial potential, for after a quick surge in the U.S. back in the 60s through the 90s, in recent years the female participation rate has pulled back while in other developed economies it has continued to increase. We are now well behind the average of the other 22 developed countries. So, we are in no danger at all of running out of labor.

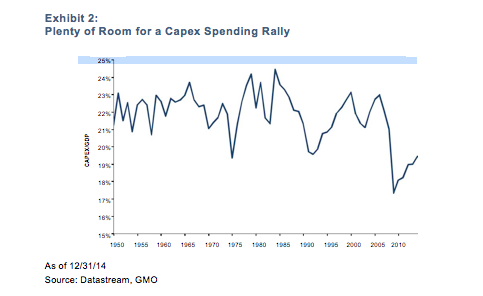

■ There is also room for an increase in capital spending, which has been quiet for years. Current capex to GDP ratio is still depressed below any level from 1950 through 2007 (see Exhibit 2). A steady rise in this capex ratio, particularly if coupled with an uptick in real hourly wages, is what is needed to inject more life into this slow-moving economic cycle.

■ The lower oil price should also have more of a stimulus effect for the U.S. as time passes. I argued in the last two quarters, however, that globally (in contrast to the U.S.) there would be surprisingly little benefit from lower-priced oil and that in GDP terms, as opposed to reality, it might well even be negative.

■ The U.S. housing market in terms of houses built is still way below the old average, and house prices are only around long-term fair value; there is room for improvement in both in the next two years.

■ It would, in my opinion, be odd to have a Fed-driven cycle end before the economy is working more or less flat out as it was in 1929, 2000, and 2007, to take the three other biggest equity bubbles of the last 100 years.

■ I still believe that before this cycle ends, the quantity of U.S. deals, including co-investments, should rise to a record given the unprecedented low rates and the current extreme reluctance to make new investments in plant and equipment (how old-fashioned that sounds these days) rather than into stock buybacks, which may be good for corporate officers and stockholders, but bad for GDP growth and employment and, hence, wages.

■ We could easily, of course, have a normal, modest bear market, down 10-20%, given all of the global troubles we have. If we do, then the odds of this super-cycle bull market lasting until the election would go from pretty good to even better. So, “2250, here we come” is still my view of the most likely track, but foreign markets are of course to be preferred if you believe our numbers. Stay tuned.

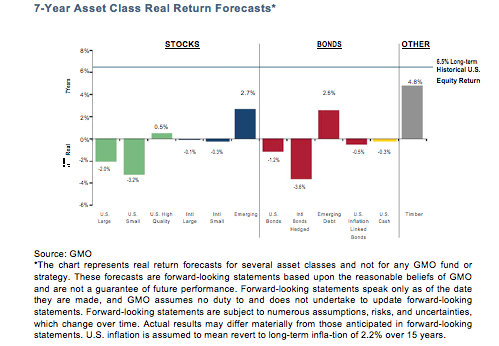

■ Please remember that this is my personal reading of the Fed’s impact. Our dismal 7-Year Forecasts speak for themselves in terms of longer-term risks and return.

The Race of Our Lives Updated: Malthusians vs. Cornucopians

With the environmental damage reports steadily coming in worse than expected (early reports from Jim Hansen in the 70s and Al Gore in the 90s, each damned in their day as looney pessimists, have by now, on average, been found to be optimistic), and with technology in alternatives steadily coming in better than forecast, the very close race continues. The pessimists, aka the Malthusians, seem determined to believe that nothing can save us, and their case is disturbingly well-reasoned. They point out that our complex economy is tuned to be energy-intensive and needs a very high energy return on energy expended to sustain itself. Early oil wells could deliver well over 100 times the energy expended obtaining the oil; today traditional oil wells are around 30:1. Coal is probably higher than that. U.S. fracking and Canadian tar sands are probably in the range of 10:1 or 15:1. The pessimists believe that a ratio of 8:1 is needed to merely maintain what we have: to educate our engineers and to build and maintain the roads over which the giant truck that carries the even larger blade for a wind tower travels. You get their point. Which is a reasonable one, I think. But although onshore wind is a respectable 8:1, solar is still only 4:1, and when energy is invested to smooth out their delivery to the grid, their ratios halve. Thus, they argue that although solar and wind can replace odds and ends of demand (which is better than a kick in the pants), they can never deliver an energy surplus back to the grid to power dense cities and our industrial system. They brush off the claims of optimists as superficial, wishful thinking.

“Rubbish,” say the optimists, aka the Cornucopians, who argue that technology and redesign are everything. Making homes and other buildings as energy-efficient as possible using existing technology, introducing new lightweight electric cars, and reducing waste everywhere can reduce energy intensity by a quarter to a half over 30 years from today’s needs. This would take the formerly required 8:1 ratio down to between 4:1 and 6:1. Then, steadily increasing technology of solar and wind generation and storage can meet that target in 30 years and we can all live happily ever after. And when you look at the details from, say, The Rocky Mountain Institute, their assertions also look plausible. They bat aside the arguments of the pessimists as the ignorant protests of technophobes. There appears to be no middle ground, yet that is where I find myself, and with substantial creative tension, being dragged from one side to the other as I read their latest salvos.

The most optimistic theme today from the Cornucopians is in the new developments for alternative energy and storage. Every important research group seems to have a major effort in this area and many of them claim to have had recent impressive successes, apparently ready to hit the market this year and next, not 5 or 10 years from now. It is very likely that within two years we will see the early entries of: a) the fast charging of batteries, up to and including car batteries, in 2 to 10 minutes; b) a one-third increase or much better in the energy density of small batteries; c) a 20-40% drop in the cost of large-scale electric storage; and d) substantially longer lives and lower costs for all batteries.

The most unnerving and scary belief of the Malthusians is that the incredible qualities of fossil fuels can never be remotely equaled by alternatives: take 10 tons of algae and other useful material and cook it for 500 million years and you will have 1 gallon of oil. Not easy to duplicate and an apparently unfair contest with any attempt to extract a small percentage of the daily sunlight. Each year, we are pumping thousands of years of accumulated energy from the sun. What a giant stroke of luck that we had this resource! And if only it were not finite and were not damaging to our home planet!

Yes, we all needed ultra-cheap fossil fuels to get rich and to have the surplus wherewithal to drive science forward. But every finite resource has its limits and, despite every ingenuity applied each year, newly discovered oil fields are smaller than the previous year! And deeper. Or in more solid rock. And, not surprisingly in these circumstances, the cost of delivering oil remorselessly rises, camouflaged as ever by its great price volatility. The scary and all too believable argument of the Malthusians is that the incredible wave of cheap energy of the last 200 years has carried us – not only in quality or wealth but, more importantly, in quantity, all 7 billion going on 11 billion of us – way over earlier high-tide marks and into the dunes. And now the tide of cheap oil is beginning to ebb, and as it does, it threatens to leave many, perhaps most of us, flapping around like so many beached fish. Indeed, unless we shape up pretty soon and agree that this is definitely not business as usual, the turning tide is likely to make us the stranded asset!

So what the Malthusians are saying, to make it very clear, is that even without considering the growing economic and environmental damage of climate change, the loss of cheap fossil fuels on its own would risk stranding us far beyond our ability to sustain our eventual population, unless, say the semi-optimists like me, we race forward in renewables to the very best of our abilities. Then we might just make it in good shape and have a new, bearable climate equilibrium in the bargain.

As I struggle to decide which of these two powerful opposing ideas is winning, I have begun to think that it comes down to two very different takes on us humans. The optimists are accurately describing what we are capable of if we put our best foot forward, and the pessimists are describing what they expect from us humans given what they see as our rather dismal record. I am, though, sustained by the hope that the pessimists are underestimating the degree to which we can scale back and bear deprivations as we did in WWII, especially in the U.K., where even potatoes and bread were rationed by the end. Yet, the social system stayed intact and many people were happier than they had been, the result of being given an unavoidable collective challenge. I do think that when times get much tougher most will rise to the occasion. And, you never know your luck – even Congress might pitch in. Will it be enough? For today, anyway, until I read something else convincing, I side with the optimists. But as I say, it is going to be a very close race.

The ultimate problem: feeding our peak population

With a little luck with the technology of alternative energy and perhaps some modest improvement in collective wisdom, I believe we will win the race of our lives as it applies to energy, but only after paying quite a high price in lower economic growth and some further substantial loss of biodiversity and damage from a rising sea level. And this is by its nature probabilistic: it could be far worse, and for some countries I have no doubt it will be. (And let me point out that even if it is not really as close a race as I believe, given the stakes even a 1 in 100 chance of disaster should surely justify investing our best efforts to head it off.) In a few decades though, I expect that we in the developed world will have at least a modest sufficiency of cheap alternative energy. And we will certainly need that advantage for we will still have other potentially existential risks to deal with. The most pressing of those is likely to be the task of feeding the world’s growing population in the face of accelerating erosion, increasing water shortages, and decelerating improvements in the productivity of grains.

Agriculture must be simultaneously adapted to changing weather; lowering inputs of fertilizer, insecticide, and pesticide; and decreasing erosion. Erosion control will be a particular problem and is my choice for the single worst and most pressing risk we face globally in the future. One of the most dependable features of global warming is increased water vapor in the atmosphere (let us call it certain), which will result, on average, in us having more rainfall (and snow!). Unfortunately, another very reliable feature of climate change is that weather systems are destabilized from their normal patterns and there are more outlier events compared to history. “Climate weirdness” is rapidly becoming an appropriate description. (Please note the two Beacon Hill photos. Yes, I am aware that this does not constitute heavyweight scientific evidence. Not a bad snow pile though!) Thus, the increased rainfall will occur in what is an extremely difficult pattern for farming: a moderate increase in severe droughts (e.g., today’s drought in California, its worst in 1,200 years according to tree rings, and Sao Paulo’s current record-setting drought) and the simultaneous several-fold increase in severe flooding incidents around the world.

I wonder, in particular, how even the most dedicated skeptic can miss the rapid rise in flooding events; some Yorkshire village beats in a single day its 300-year record for a month! Large parts of Australia and Pakistan disappear under feet of water, Phoenix and Denver get flooded. Just this March, 25 people were drowned in extreme floods in the Atacama Desert. The Atacama Desert! It is one of the driest places on Earth. Almost every day, certainly every week, there is an astonishing record-breaking downpour. To make matters much more dangerous, soil erosion turns out to be a power law based on heavy downpours. That is, very little erosion takes place in light, medium, and quite heavy rains, which occur over roughly 350 days a year. However, the remaining handful of very heavy rains account for about three-quarters of all erosion, and the one or two worst downpours every year or two can cause half of that. A recent report4 predicts an up to five-fold increase in the U.K. of just such deluges (of just over one inch in one hour) during the summer over this century. (This is not, trust me, what a British summer needs!) Unfortunately, recent global soil erosion has continued to run around 1% a year, and with more heavy downpours this could rise to 2% a year unless we change our practices quite fast.

Even the lamest mathematician can easily work out that a 1-2% loss of soil each year if sustained would be disastrous. But with our in-built conservatism and effective opposition from vested interests, the required, profound change in our agricultural practices will not be easy. In a strange way, it means adopting many of the best agricultural practices of earlier centuries: an all-around nurturing of the soil and rotational crops that include nitrogen fixers. Most importantly, such nurturing will allow us to end the use of the mined and very finite fertilizers, potassium and phosphorus. Best practices in sustainable farming differ profoundly as you change region and soil type, so sustainable farming will be uncomfortably brain-intensive (and who loves that?) and it will also require a new level of data sharing.

One of the worst problems may be that switching to sustainable agriculture5 is also likely to cause at least a temporary drop in production. Delay may mean we lose our current ability to produce a food surplus. Today we waste nearly 50% of all food, yet the great majority of us seven billion are either well fed or overfed. With few exceptions, only bad distribution – of income as well as food – causes any starvation. In the future, as the population grows and erosion and weather problems increase, our surplus agricultural output will decrease, making it increasingly painful to make the transition to sustainable farming. Yet, failure to move toward sustainable and less resource-intensive agriculture will mean that many poorer countries, particularly those with rapid increases in population, will begin to starve. There are some indications that in some parts of North Africa and Sub-Saharan Africa this process has indeed already begun. The crowds marching into Tahrir Square in the Arab Spring, for example, were apparently chanting, “Bread! Freedom! Justice! Bread! Freedom! Justice!”6 But bread was first.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending April 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

1 The pre-1972 range was about $8 to $32, and the current range around $75 is about $37 to $150. The historical range around trend – just more than a double and less than a half – is far greater than is realized.

2 IMF, World Economic Outlook, April 2015. http://www.imf.org/external/pubs/ft/weo/2015/01/pdf/c2.pdf

3 To be precise, using data from 1871 to today, a two-sigma level on the price series is as low as 2020. Starting in 1925, it is as high as 2400. Starting around 1900, it is 2250 and that, for good or bad, is our choice. (There is no getting away from judgment in this kind of data!)

4 Elizabeth Kendon, et al., Climate Change, Nature, 570-76 (2014).

5 In the interest of full disclosure, let me remind you that I have recently acquired a farm that will attempt to make a profit at farming sustainably.

6 “Years of Living Dangerously,” Episode 7, “Revolt, Rebuild, Renew,” 2014. Available on Showtime and YouTube.com (for a nominal fee). I appear in a 4 minute and 20 second starring role!

© GMO