Breaking Out of Bondage

The past year has witnessed yet another rally in long-term bonds all around the world. This move has driven long-term bond yields to extremely low levels, in many cases completely unprecedented. The reasons are not particularly mysterious. A combination of low inflation associated with the collapse in commodity prices and quantitative easing has pushed yields ever lower, particularly in Europe, where the list of countries hitting all-time lows in bond yields has hit double digits. Switzerland, whose bond market is admittedly of more academic than market importance, has claimed the distinction of being the first country in history to have its 10-year bond yield turn negative. At current yields, the utility of long-term government bonds in most investment portfolios is questionable at best. To our minds, any investors who are not required to own long-term government bonds in their portfolios should warmly consider getting rid of them, and those tempted to speculate on the future pricing of bonds may want to consider the benefits of betting that European and perhaps Japanese bond yields will be higher in the future. The obvious question this recommendation leads to is what to do with the money that isn’t being put in long duration bonds. We don’t believe that investors should use it as an excuse to buy more equities, but do believe that investors should consider both shortening up the duration of their bond portfolios – the low yields on cash today are a decent trade-off against the possibility of significant losses on bonds in the future – and expanding holdings of alternative investments, such as conservative hedge funds, as well. This makes sense for U.S.-based investors, but is even more essential for investors in Europe and Japan.

It’s been a very good ride

Over the past 30 years, the MSCI World equity index has returned 7.5% above inflation. Readers of GMO Quarterly Letters over the years are probably used to our arguments that the next 30 years are unlikely to be as friendly to equity investors. But this Quarterly will not be making that argument. This is not because we have changed our minds with regards to equities, but because today the equity markets seem to be less oddly priced than the other major asset that most investors have had in their portfolios over the last three decades: government bonds.

Over the same 30-year period that global stocks have delivered their stellar +7.5% real return, a constant maturity portfolio of 30-year U.S. Treasuries has delivered a no less impressive +6.2% real. This has left investors in the happy situation of having pretty much no bad answer to the asset allocation question: stocks or bonds? And lest you think that my cherry-picking the 30-year bond is the key to this point, the Barclay’s U.S. Aggregate Bond index delivered an even higher +6.6% real, and a buy and hold investor in the 30-year Treasury issued in the spring of 1985 would have achieved almost +9.0% real!

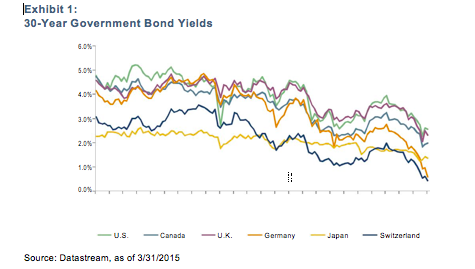

As an asset allocator by profession, there is something rather sobering to the thought that over the last 30 years, any asset allocation at all would have led to pretty much the same (very good) return. But that thought is a triple shot of tequila relative to the thought of what the next 30 years are going to bring to bond investors. For while it is unlikely that stock investors are going to achieve anything like as strong a return over the next 30 years as they did over the last, it is basically impossible for bond investors to duplicate their feat.1 In March of 1985, the U.S. 30-year Treasury Bond yielded 11.57%. In March 2015, it yielded 2.56%. Exhibit 1 shows 30-year bond yields over the past decade across six developed countries.

A buy and hold investor in a U.S. 30-year Treasury Bond can be pretty sure what he is going to get between now and 2045: 2.56%. And 2.56% is about as good as a long-term bond gets these days. The U.K. 30-year Gilt yields 2.31%, the 30-year Canadian Government Bond yields 1.98%, the 30-year Japanese Government Bond yields 1.34%, the 30-year German Bund yields 0.58%, and the Swiss 30-year yields 0.43%. For an investor choosing among the 30-year government bonds available today, I have a lot of sympathy for anyone who chooses that 2.56% yielding U.S. Treasury. Given long-term expected inflation in the U.S. of around 2.1%,2 at least the prospective real yield is positive. The same cannot be said of any of the other markets mentioned, because expected inflation is higher than the 30-year bond yield in each one.

Rational investment reasons to hold long-term bonds?

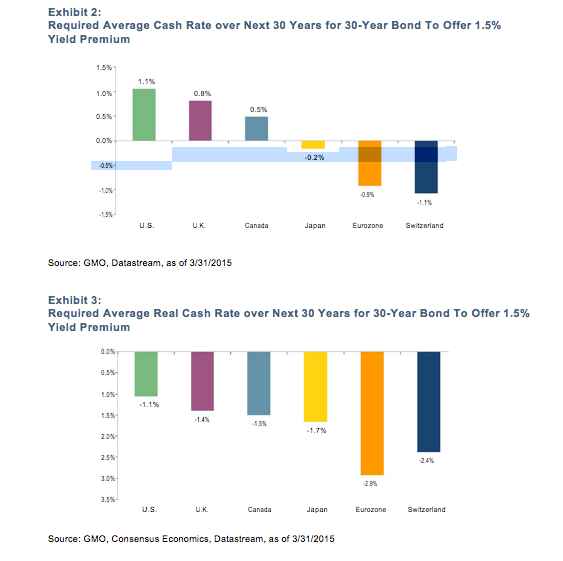

Holding aside regulatory requirements and greater-fool speculation, why would an investor sign up to lose money after inflation over a 30-year period? Two possibilities come to mind. The first possibility would be if the asset in question was such a wonderful hedge against bad economic events that it allowed the investor to hold enough additional risky assets to make up for the losses on the loss-making asset. The second possibility is even simpler: that plausible alternative investments are even worse. Let’s take the second possibility first. At first blush, this idea seems to have a fair bit of merit today. If the alternative investment to holding a 30-year bond is holding a shorter-term bond, shorter-term bonds do indeed look “worse” in all of the markets mentioned. Cash rates and shorter-term bond rates are lower than the 30-year rate in each market. Historically, 30-year bonds have tended to offer a yield premium of at least 1.5% over cash rates in most markets; in the U.S., the average has been 2.4% over the last 30 years. If we imagine that investors demand 1.5% more from a 30-year bond today than they do from cash, we can calculate what investors would have to think cash rates will average over the next 30 years in order for the 30-year bond to be “fair.” Exhibit 2 shows those rates in absolute terms, and Exhibit 3 shows them in inflation-adjusted terms.

In each case, real cash rates would have to be significantly below zero to offer a historically normal premium for the 30-year bond, and for Japan, Germany, and Switzerland, the rates would actually have to be negative on average in absolute terms for the next 30 years. Current cash rates are negative in both Switzerland and Germany, although this has yet to be fully passed through by the banking systems, where managers seem to be hoping that the negative rates will be temporary. But perhaps the banks are wrong and negative cash yields are here to stay in Europe. Let’s think about what that would mean. Central banks in Europe have taken cash rates through the zero level in an effort to pull inflation up to their target of close to 2% per year and weaken their currencies. Judging from economists’ inflation forecasts and the inflation swap markets, investors believe they will succeed on the inflation front. But implicit negative cash rates for the next 30 years strongly implies that their efforts will fail.

That is a fairly stunning thought. If bond prices in Europe and Japan are pricing in a normal premium for long-term bonds, it is because investors believe that governments and central banks will not be able to control inflation, but given that lack of control, somehow the investors still believe inflation will be exceptionally low. That seems a very odd belief given the history of paper money systems. History seems to show two possible outcomes from fiat currencies. In the first, well-managed currencies have experienced price stability or controlled inflation driven by sensible monetary and fiscal policy. In the second, inflation has exploded to high levels as bad government policies, bad luck, or both led to uncontrolled price rises.3 At the very least, if central banks cannot control inflation, the expected volatility of inflation should be higher, and higher volatility of inflation would seem to argue for a higher than normal yield premium for long-term bonds.

So the odds that investors are buying 30-year bonds because they have a higher expected return than rolling shorter-term bonds seems pretty unlikely. Now, how about the first scenario – that investors own the bonds because of their exceptional hedging properties? This idea implies that while the expected return to the bonds is low, the expected return contingent on a bad economic environment is so good that a portfolio that holds the bonds alongside risky assets has a better expected return than one that holds a lower duration low-risk asset, such as cash. How plausible is this? If judged by the history of where bond yields have gotten to in previous crises, it makes no sense because today’s bond yields in many markets are significantly lower than any historic precedent and could therefore be judged to be already pricing in a worse economic outcome than previous crises. Insurance for portfolios is a trickier proposition than for, say, houses. The insurance on your house will pay off only if the hurricane hits, and once the hurricane has destroyed your house there is really no more damage it can do. In a portfolio context, the process is less straightforward. As the hurricane comes closer, your insurance company would offer larger and larger sums in exchange for cancelling your insurance and you would have to choose whether and when to take the offer. Complicating matters further, even after the hurricane hit, it would still be possible for another hurricane to come by and destroy whatever was left of your portfolio. The upshot is that an absolutely crucial part of successfully insuring a portfolio is understanding when to call in the insurance. With bond yields approaching or through all-time lows all around the world, now would seem to be a pretty good time.

This is especially true when you realize that bonds are far from the be-all and end-all of portfolio insurance. Of the four forms of “deep risk” for investors that William Bernstein has so ably chronicled– inflation, deflation, confiscation, and devastation4 – long-term bonds really insure against only one, deflation. Against inflation, they are the most vulnerable asset around, and against confiscation and devastation, they typically fare no better than other assets.

Price-insensitive buyers of long-term bonds

But this may all seem beside the point. We know there are price-insensitive buyers for long-term bonds in Europe and Japan today. Pension funds and insurers are forced to buy long duration high quality assets by regulators, and the ECB and BOJ are avid buyers of long-term bonds in their quest to help generate some inflation in the medium term. Why expect them to operate with the same thought process as other investors? My point is not to disparage their reasons or discount their power in the market. It is merely to suggest that they have reasons quite different from those of unconstrained, profit-oriented investors, and if they are the ones driving the prices of these securities today, leave the bonds to them. Any investor that is not forced to own these securities has no obvious reason for owning them, as their benefits as a deflation hedge seem far outweighed by their downside in the face of any other scenario.

So what should we do?

The case for long-term government bonds today as an investment is a very thin one. The case for them as a speculation is perhaps better. After all, if there are price-insensitive buyers for a security who have already stated that they will be continuing to buy large amounts of it in the coming months, it may make sense to front run them by buying the asset ahead of time to sell to them. It is possible that this will be a good money maker in the coming months. Much of the time, markets price in events that are known (or thought to be known) ahead of time. But sometimes the market seems to be taken by surprise by events that have actually been well-telegraphed. Today’s all-time low bond yields may very well be eclipsed by tomorrow’s even lower ones.5

But let me suggest another course of action for the speculator with a somewhat longer time horizon. While the telegraphed behavior of central banks over the coming year or two might easily drive these bond yields lower, the central banks have no intention of continuing their policies forever. Their goal is to generate sustainable inflation and economic growth, and when that has been achieved – whether through their policies or despite them – the buying will stop. This should leave the pricing of bonds in the hands of profit-minded investors. And both history and common sense suggest the yields such investors will demand will be a good deal higher.

Admittedly, it is a tough ask to an investment committee to replace their holdings in “safe” long-term government bonds with a short in those same bonds.6 But no one should be under the illusion that long-term bonds trading at these yields are truly safe investments. In all probability they are safe against a loss of value under deflation, but in just about any other circumstance their expected real returns are somewhere between approximately zero to strongly negative.

In our multi-asset portfolios our net duration today is approximately zero. While we do have some long positions in a few of the least unappealing government bond markets, those are matched by shorts in markets where we find long-term bond yields to be far too low. We are trying to resist the temptation to therefore load up more heavily on equities or corporate credit. Our concerns about equities should be well-known by now. As for corporate credit, while today’s spreads over Treasuries look okay, the liquidity in these markets has become shockingly poor, and we believe it is appropriate to demand an extra margin of safety when operating in markets where it has become very difficult to transact. This leaves us owning more conservative “alternative” strategies as a superior anchor to the portfolio in tough economic times compared to government bonds, whose yields make little sense.

Disclaimer: The views expressed are the views of Ben Inker through the period ending April 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be con-strued as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

1 In nominal terms, it really is impossible, but should inflation run at negative 4% or less per year over the next 30 years, it would be possible to achieve a similar real return. To the best of my knowledge, that kind of prolonged deflation has occurred nowhere on Earth in recorded history, but that doesn’t actually make it impossible.

2 March release of the Federal Reserve Board of Philadelphia Survey of Professional Forecasters, 10-year CPI forecast.

3 Some readers may wish to claim Japan as a third possibility with “deflation for 20 years.” Annualized inflation since the peak in Japanese CPI in 1998 has been -0.1%. Even if we chose to use the pre-Abenomics CPI low point, the figure was -0.3% at its worst from 1998 to 2012. Officially, you can call that deflation, but it seems a lot more like price stability to me.

4 William J. Bernstein, Deep Risk: How History Informs Portfolio Design, 2013.

5 While it is only the European Central Bank and Bank of Japan that are actively implementing quantitative easing policies, it is easy to imagine how their actions drag down bond yields in other markets as well. Investors unable to resist selling their Bunds to the ECB at yields approaching (or through!) zero may look around and see the higher rates in the U.K., Canada, Australia, and the U.S. as irresistible in contrast.

6 To be clear on this, an investment committee is a lousy candidate to try to run any sort of short position. Running a short requires timely oversight, which cannot be handled via quarterly meetings. An investment committee could plausibly empower staff or an external manager to put on and manage such a short, but should definitely not attempt to do it themselves.

© GMO