Throughout history of the high yield market there have been various legislative acts that have created and continue to create the market dislocation that allows investors an opportunity to produce what we see as attractive risk-adjusted returns. The Financial Institutions Reform Recovery and Enforcement Act (FIRREA), which passed in 1990, was the first piece of legislation that dramatically altered the landscape for high yield corporate bonds. In the time leading up to this legislation, bank failures were everywhere and Wall Street lost junk bond pioneer Drexel Burnham Lambert. Citibank was almost dead, more than 700 savings and loans/thrifts failed and the controversial California-based insurance company First Executive disappeared. The government sponsored an agency that became known as the Resolution Trust Corporation (RTC) to deal with the savings and loan (S&L) failures. Investments in junk bonds and junk loans to emerging market countries such as Mexico and Brazil were at the center of the storm and were the root cause of all the problems, according to the popular press.

Regardless of the blaming of Drexel and the junk-bond pirates, the real root of the problem developing in the 1980s was actually real estate. William Seidman, former head of both the Federal Deposit Insurance Corporation (FDIC) and the RTC, commented on the 1980s issues, stating:1

The critical catalyst causing the institutional disruption around the world can be almost uniformly described by three words: real estate loans. In the U .S., the problem was made even worse by allowing S&Ls to make commercial real estate loans in areas they knew little about. They were already in trouble because they borrowed “short” and lent “long” in financing the housing market.

How familiar does that sound? Since 2008, we have been working off the biggest hangover in the history of residential real estate.

Apparently, we are slow learners or have selective amnesia. Bill Seidman—one of the most respected regulators of our time—had come to the conclusion that real estate lending was at the core of the meltdown in the ‘90s. But Seidman’s claims were ignored. Instead, politicians decided that the answer was to make sure that going forward, thrifts were almost completely invested in real estate while forcing them to sell their high yield bonds at what was then the bottom of the market. Below were two of the requirements that came out of this ridiculous piece of legislation (FIRREA):2

(7) Required savings and loans to meet a new “qualified thrift lender” test of the 70% of portfolio assets in residential mortgages or mortgage related securities.

(14) Required savings associations to divest their holdings in junk bonds by July 1, 1994, and generally follow the same investment guidelines as commercial banks. Junk bonds and direct investments of saving and loans must be held in separately capitalized subsidiaries.

Around the same time as all of this legislation was being passed, a group known as the Bank for International Settlements (BIS) was passing the first Basel Accord. Known as Basel I, this accord set capital standards for global banks for a variety of very broad asset classes. Corporate bonds and loans were set at 8%, meaning a bank had to have Tier 1 capital (equity capital and reserves) of 8 cents to back each dollar held in a corporate security. Prior to this accord being passed in 1988, banks operated somewhat by the seat of their pants. They reserved what they deemed appropriate for various asset categories and worked with regional or national regulators on these issues.

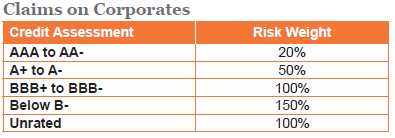

The ink was barely dry on Basel I when pressure from the various banks sowed the seeds of a monumental and ill-understood piece of legislation that led to the meltdown that began during the last quarter of 2008. The argument sounded rational. Why would a loan to General Electric require the same amount of capital as one to Joe’s Liquor Store? So back to the drawing board we went, which led to the second Basel Accord, or Basel II. At the heart of this proposal lies the notion of risk. Regulators wanted to make sure that capital reserves were appropriate for the risk of the assets held by banks. Sounds like good policy, but how does one measure risk? Well enter our friends the credit ratings agencies. What Basel II effectively said was that credit ratings will determine risk and the amount of capital required. Here is what was finalized:3

To translate into simple English, if 8% was the base capital charge, then AAA to AA securities would require only 20% of this, or 1.6% capital backing for each dollar of securities held. Anything below BB- would require 150% of 8%, or 12% capital. This led to banks focusing their attention on the highest-rated securities, which required limited capital and allowed for massive leverage. Let’s do the math. If a bank requires only 1.6% capital, the inverse of this is the amount of leverage they get, which is more than 60:1! So once again, an arcane policy further restricts another group of major institutions from investing in lower-rated securities (regardless of their true investment quality). Ironically, the chase for AAA securities was at the root of the 2008 financial crash as Wall Street created (and the rating agencies were relied upon to rate) many synthetic AAA bonds that turned D (defaulted). In the end, the rating agencies ended up with more stature after proving they did not deserve it and the results were disastrous, as witnessed by the 2008 meltdown of the global markets.

More recently we have seen the impact of the Dodd-Frank Bill and Volker provision within it. Post the financial crisis, various pieces of legislation, including Dodd-Frank and the Volker Rule were put into effect with the goal of reducing risk and increasing the stability of the banking system. While these pieces of legislation may serve to stabilize the banks, they have created unintended consequences for financial markets, including what we see as less stability and higher volatility in fixed income markets. For instance, the Volker Rule effectively limited the ability for banking institutions to engage in proprietary trading of securities for their own accounts. As a result, traditional market makers and liquidity providers (such as the major investment banks) have pulled back on their lending and market making activities due to these regulations and a focus on risk reduction on their balance sheets.

Why is it important to understand such legislation? Mainly because it can shape who ends up owning certain asset classes. In the cases of FIRREA and Basel II, banks became large sellers, creating opportunities for buyers. In the case of Dodd-Frank, it has resulted in greater volatility in today’s high yield market, as many of the market makers that were previously in place to absorb some of the trading volume are no longer there. Yet this volatility can create attractive entry points. Great credit analysis—a pre-requisite for producing returns in this asset class—is aided by the opportunity-set itself, which is a function of the market and the lack of permanent investors created mainly by misinformation and poorly drafted legislation. Over various points in history, we have seen this legislation create opportunity for high yield bond investors.

For more on the history and development of the high yield asset class, a discussion of the legislation and ratings methodologies that have created what we see as opportunities in the marketplace, and comparative historical risk adjusted returns with other asset classes, click here to read our updated piece, “The New Case for High Yield: A Guide to Understanding and Investing in the High Yield Market.”

1 “Panel Lessons of the Eighties: What Does the Evidence Show?” History of the Eighties—Lessons for the Future. Federal Deposit Insurance Corporation, 1997. p. 58.

2 Friedman, Thomas. Dictionary of Business Terms. Barron’s Educational Series, Inc., 2007. “Financial Institution Reform, Recovery and Enforcement Act (FIRREA).”

3 “International Convergence of Capital Measurement and Capital Standards,” Basel Committee on Banking Supervision. Bank for International Settlements June 2006.