Region Insights – Europe – Investment Opportunity in Europe is Compelling

First Quarter 2015

Investment Opportunity in Europe is Compelling

While Europe abounds in world-class companies, macro concerns in 2014 obscured compelling opportunities for price appreciation and earnings power that we believe will surprise to the upside in 2015. Investors have woken up to the opportunity in the first two months of 2015 and many European exchanges are off to a fast start. We think more gains are ahead, particularly in small- to mid-size companies in Europe.

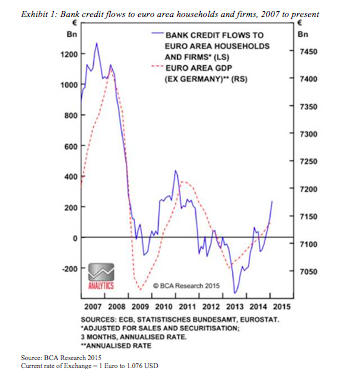

Lagging stock prices last year created a great opportunity for investment in European stocks. Excessive focus on the risks associated with Greece and a potential "Grexit" masked the benefits that accrued to European companies as the euro weakened against other major currencies and signs of sustainable credit growth emerged.

The weaker euro has significantly improved the competitive position of many European countries, most of which have a significant component of GDP growth tied to exports. In addition, the European Central Bank has finally approved quantitative easing, which officially began on March 9 with initial monthly purchases of €60 billion ($65 billion USD). We believe these developments will provide a macro-economic tailwind for European stocks in the coming quarters.

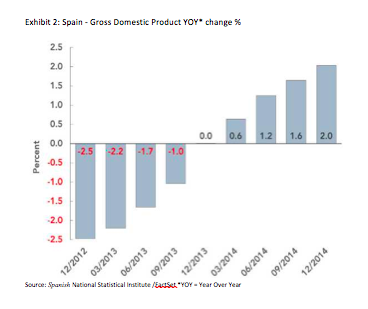

As of the middle of the first quarter of 2015, the Rainier International Discovery Fund held 28% of its assets in Europe, the highest we have held in the last three years. Business confidence has picked up in recent months and share prices have appreciated more than 17% in euro terms. Despite the synchronized run up across European equity markets, we view the region as a heterogeneous market from a bottom up perspective and continue to find pockets of real and sustainable growth in the Nordic countries, Germany, and even Southern Europe, such as Spain, where we have recently added exposure. Top holdings include a globally dominant payment processing company, a France-based operator of nursing homes throughout Europe, and an Italy-based diversified financial firm with a wealth management focus. Likewise, we believe Swiss companies, especially those with operations predominantly outside the country (and therefore less affected by the recent surge in the Swiss Franc) should also benefit. Two notable examples include our investments in two semiconductor companies which have benefitted from a global trend toward connected devices. Both companies have a sizeable revenue and cost base outside Switzerland.

Signs of credit growth can be seen in the results of one of Spain's strongest regional banks; a recent addition to the portfolio. Furthermore, a weaker euro benefits exporters and encourages in-bound tourism. Two investments leveraged to this include a globally dominant auto parts supplier that produces high-performance braking components for global auto original equipment manufacturers, and a hotel operator with a presence throughout Europe.

The earnings growth rates overall in Europe are not as high as Asia or emerging markets on an absolute basis. However, we are beginning to see signs of positive fundamental change within European economies and companies. As a result, we are seeking risk/reward opportunities in Europe where we believe valuations are more attractive.

© Rainier Investment Management, LLC