Strategic Allocaiton to High Yield Corporate Bonds – Why Now?

HIGH YIELD CORPORATE BONDS - WHY NOW?

The demand for higher yielding fixed income investments has never been greater. In the current environment of low yields, from the virtually non-existent rate offered on savings accounts and CDs to the declining, and in some cases negative, yields on global government debt securities, investors are searching for attractive income generating alternatives. While at the same time, the day grows nearer that the Federal Reserve will begin to raise interest rates, which could in the short term negatively impact the return potential of certain fixed income asset classes. As such, investors might want to consider a strategic allocation to the U.S. high yield corporate bonds in an attempt to boost overall yield and total return potential as well as mitigate the potential negative impact on fixed income returns from an interest rate hike.

We believe U.S. high yield corporate bonds are positioned to benefit as the U.S. economy continues to gradually improve. The Federal Reserve forecast for Gross Domestic Product (GDP) is at or above its projected long-term trend rate for 2015 through 2017, supported by strong job creation, a pickup in consumer spending, gains in business fixed investments and improvement in most categories of bank lending. Additionally, after the sell-off in the second half of 2014, high-yield valuations represent an attractive entry point.

WHAT IS HIGH YIELD?

The majority of high yield bond issuance originates in the United States, where they have been trading for decades. The term "high yield" refers to company- issued debt rated below investment grade - typically determined by the three major rating agencies: Moody's, Standard & Poor's and Fitch. These grades, or ratings, are the product of credit analysis that takes into account a variety of factors such as company size, leverage, capital market access and even management tenure. To compensate investors for lower ratings, high yield bonds pay larger coupons in comparison to investment grade corporate and government debt.

However, the risk differences between high yield bonds can vary dramatically. High yield credit ratings can be separated into 11 tiers of quality, ranging from bonds on the cusp of investment grade, down to the most distressed company debt on the verge of default. As expected, higher rated debt has historically experienced significantly lower default rates. Since 1981, the average default rates of the most conservative U.S. high yield corporate bonds, rated BB+, BB and BB- by Standard & Poor's, have been 0.59%, 0.83% and 1.27%, respectively. Those figures are compared to an average default rate of 24.74% for the most speculative debt rated CCC/C.

POTENTIAL BENEFITS OF HIGH YIELD

Total Return Potential

The addition of high yield fixed income to an overall portfolio may provide a number of significant benefits, the most obvious being the possibility for increased income. Yet assuming an issuer maintains capital market access and meets the terms of its borrowing agreements, high yield bonds may also have ample opportunity to appreciate in value. While investment grade bond prices have been significantly impacted by macroeconomic factors that affect interest rates, high yield bonds have been more accurately characterized by their idiosyncratic risk - as their prices have been linked closely to a specific issuer's ability to pay its debt. This relationship makes the high yield credit part of the capital structure where both fixed income and equity investors' interests are aligned. Functioning essentially as a stock and bond hybrid, improvements in an issuer's underlying fundamentals and ability to fulfill its debt obligations has often led to better earnings and a more attractive credit profile - each of which can have a meaningful positive impact on both types of securities' performance.

Reduced Sensitivity to Rising Interest Rates

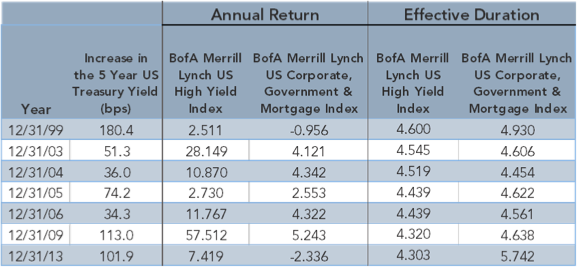

Historically, returns on the high yield asset class have experienced less sensitivity to interest rate changes compared to other "safer" fixed income alternatives. The two primary determinants of fixed income total returns are changes in interest rates and credit spreads. Interest rates moving higher would normally be associated with a strengthening economy. Since high yield bonds are more closely correlated with private sector growth, the combination of greater credit spreads or larger risk premiums versus investment grade corporate bonds or other high quality fixed income alternatives and improving corporate conditions in a typical economic recovery provide the opportunity for improvement in the company's fundamentals or financial strength resulting in declining credit spreads and a corresponding improvement in the price of the bond. As credit spreads compress to Treasury rates they mitigate the negative effect of rising interest rates on fixed income return - ultimately allowing high yield bonds to potentially outperform other types of fixed income assets. Additionally, because of their high coupons and typically shorter maturities, high yield investments have a shorter duration compared to investment grade fixed income asset classes. Duration measures the sensitivity of a fixed income security to changes in interest rates. The lower the effective duration the less sensitive a fixed income instrument will be to the potential negative impact of rising interest rates on its total return. In fact, in the last seven calendar years in which the interest rate on the 5-year Treasury rose, high yield bonds outperformed the broader investment grade fixed income market. (See Exhibit 1.)

Exhibit 1:

High Yield Returns

(last seven calendar years of rising rates)

Source: Morningstar

Diversification

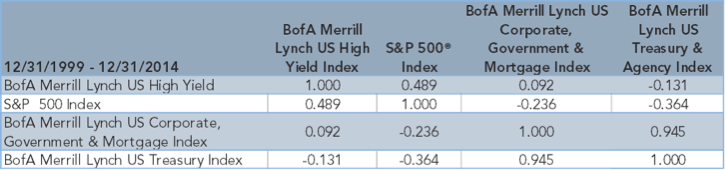

High yield bonds have traditionally shown low or even negative correlations with other asset classes such as commodities, equities and government debt. In fact, the correlation between U.S Treasuries and high yield since 1999 has been -0.13%. (See Exhibit 2.) Reduced correlations may imply diversification benefits. Therefore we believe an allocation to opportunistic credit such as high yield bonds could have a positive impact on a portfolio's overall risk/reward profile potentially resulting in better risk-adjusted returns.

Exhibit 2:

Correlation Matrix

Source: BofA Merrill Lynch

Attractive Risk-Return Profile

The appealing traits of high yield debt have led to a remarkable long-term performance track record. Over the past 25 years, the overall high yield market has produced equity-like returns with significantly less volatility than other asset classes. The income stream from higher coupon payments provides for reduced return volatility, thereby improving performance on a risk-adjusted basis.

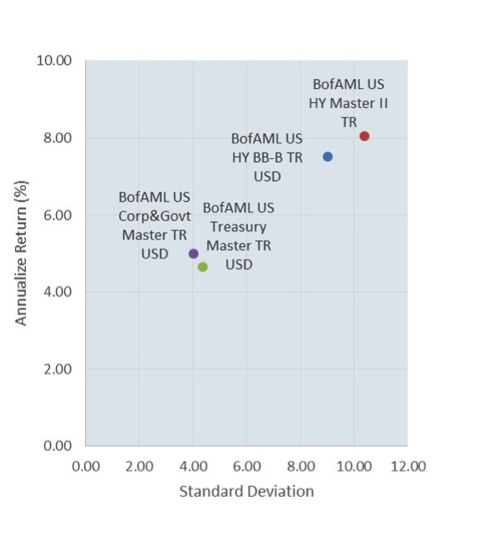

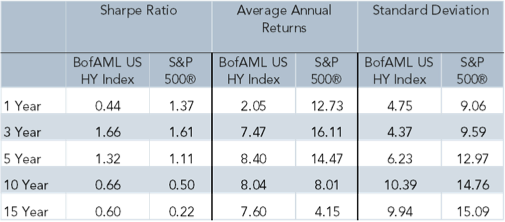

Subsequently, our argument for constructing the Rainier High Yield Fund primarily from BB & B rated debt is that this segment of the high yield market has historically provided the most attractive risk-reward profile. As Exhibit 3 shows, over the past 10 years, bond issuances with BB-B ratings have returned 7.68% on an annualized basis with a standard deviation of 9.26%. Conversely, the overall high yield market (represented by the BofA Merrill Lynch US High Yield Index) has returned 8 .59% with a standard deviation of 11.14%. This trend of superior risk-adjusted returns has been quite consistent as shown by the trailing Sharpe ratios for the same indices. (See Exhibit 4.)

Exhibit 3:

|

Exhibit 4:

10 Year Return vs. Standard Deviation

|

WHY HIGH YIELD TODAY?

Fundamentals

As the economic cycle continues to mature, deleveraging is no longer the priority it once was and leverage has stabilized at levels significantly below the prior peaks. That said, company management teams have been diligently taking advantage of the low interest rate environment to refinance higher coupon debt, pay down revolving credit facilities and extend maturities. These actions have improved their liquidity and enhanced their ability to withstand economic fluctuations.

With economic growth gaining traction in 2014, high yield companies whose fundamental performance is highly correlated with strength of the economy, have been able to generate revenue gains and improve margins and cash flow. Combined with actions taken to improve the balance sheet described above, credit profiles have improved thereby increasing the attractiveness of high yield companies.

Economic Growth

The U.S. is currently one of the few countries globally that has a materially positive GDP outlook. Although it's not the rate of growth normally associated with a typical U.S. economic recovery, it has been sufficient to drive the unemployment rate down toward 5% and for the Federal Reserve to end its quantitative easing program and focus on when it will raise the federal funds rate for the first time since June 2006. Moderate economic growth is ideal for high yield corporate bonds. Moderate growth keeps management and focused disciplined as revenue and profitability gains are not a given and the fear of an economic slowdown remains front and center. Faster economic growth leads to increased debt issuance to finance capital expansion, potentially overvalued merger and acquisition transactions and possible stock buybacks which potentially increases operational risks and deteriorates credit fundamentals. The majority of the high yield issuers are predominantly U.S. centric. In the current environment this is an advantage given the U.S. economy is better positioned and has a better outlook for growth compared to other countries globally.

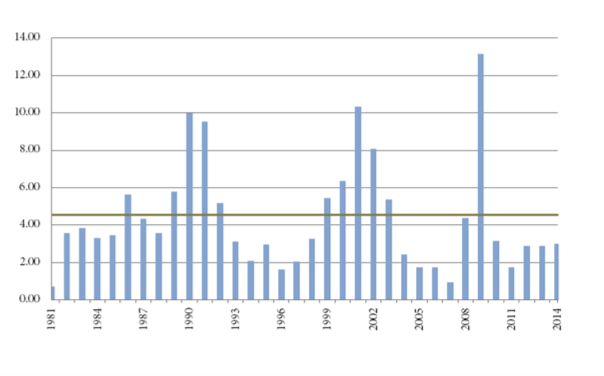

Low Default Rates

We believe the combination of solid credit fundamentals, improved liquidity and moderate economic growth provides a favorable backdrop for high yield bond performance. As such, US high yield default rates, which have improved significantly since the financial crisis, were 1.6% in 2014 and are expected to remain near their lows over the medium term.

Valuation

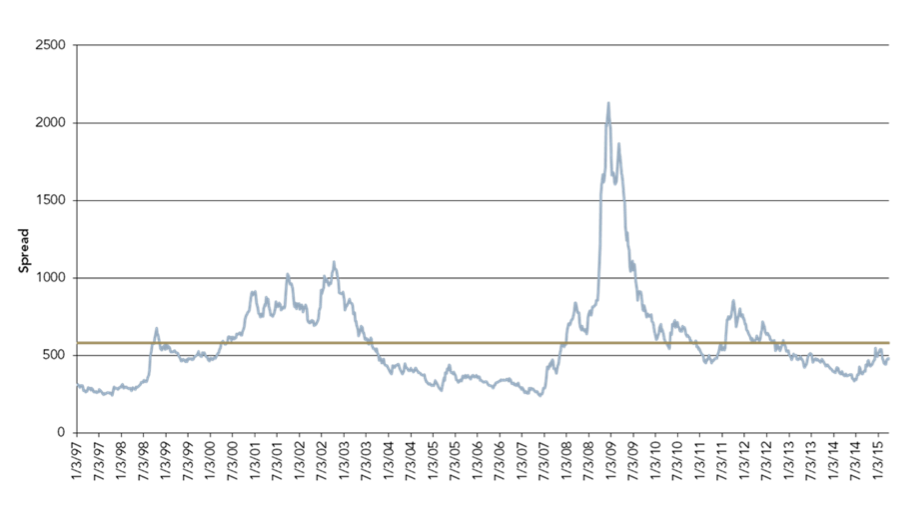

High yield valuations are attractive as we enter 2015, especially after the sell-off in the second half of 2014. In the context of historical credit spread levels, the current high yield credit spread of 481 basis points ("bps") is just inside the long average of 581 bps and significantly more attractive than the recent low of 353 bps in June 2014. Relative to investment grade corporate bonds whose current credit spread is just 138 bps, high yield bonds looks attractive when considering the additional credit spread and its potential to mitigate the impact of rising interest rates compared to investment grade bonds which are significantly more exposed to interest rate risk than high yield. With the positive outlook for the economy, and current credit fundamentals and default rates, we believe there is significant opportunity for spreads to tighten further resulting in potential capital appreciation and attractive total returns.

Exhibit 5:

High Yield Bond Default Rates - Percent of Issuers

Source: Moody's

Demand for Income

Investors are desperate for higher yielding alternatives for their fixed income allocations. Interest rates are near their historic lows and investors are having difficulty meeting their income objectives. The common misconception is that instead of allocating a portion of their "safe" fixed income portfolio to high yield bonds they should increase their allocation to equities to increase portfolio returns. The belief is that making an allocation to high yield is increasing the risk of the fixed income portfolio when in fact what is being done is increasing the potential risk of capital loss by increasing the allocation to equities. As we've illustrated in Exhibit 6, high yield bonds are less risky than equities and have also outperformed "safer" fixed income assets during periods of rising interest rates. And when the fear is that the Federal Reserve's easy monetary policies have been supporting valuations, this becomes an even riskier proposition. Over the long term, we believe high yield has the potential to deliver equity-like returns with less variability thereby increasing their attractiveness as part of a diversified asset allocation portfolio.

Exhibit 6:

High Yield Spread History

|

Source: BofA Merrill Lynch |

CONCLUSION

When taking these observations in aggregate, we consider high yield debt to be the market's quintessential "sweet spot" - nestled between the meager yields of "risk-free debt" (U.S. Treasuries) and the subdued, but potentially volatile, returns of equities. By striking a balance for investors looking to fulfill their income or capital appreciation needs while simultaneously managing for the possibility of shocks to the global economy, we are of the opinion that high yield corporate bonds, particularly BB and B rated issues, should continue to be an attractive asset class on a risk-adjusted basis.

Mutual fund investing involves risk. Principal loss is possible. Stocks are generally perceived to have more financial risk than bonds in that bond holders have a claim on firm operations or assets that is senior to that of equity holders. In addition, stock prices are generally more volatile than bond prices. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. A stock may trade with more or less liquidity than a bond depending on the number of shares and bonds outstanding, the size of the company, and the demand for the securities. Similarly, the transaction costs involved in trading a stock may be more or less than a particular bond depending on the factors mentioned above and whether the stock or bond trades upon an exchange. Depending on the entity issuing the bond, it may or may or may not afford additional protections to the investor, such as a guarantee of return of principal by a government or bond insurance company. There is typically no guarantee of any kind associated with the purchase of an individual stock. Bonds are often owned by individuals interested in current income while stocks are generally owned by individuals seeking price appreciation with income a secondary concern. The tax treatment of returns of bonds and stocks also differs given differential tax treatment of income versus capital gain.

Diversification does not guarantee a profit or protect from loss in a declining market.

Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. Investments in asset-backed and mortgage- backed securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods.

© 2015 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in the distribution percentages.) The Overall Morningstar Rating for a fund is derived from a weighted average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. Rainier High Yield Institutional was rated against the following numbers of U.S.-domiciled High Yield Bond funds over the following time periods: 595 funds in the last three years and 501 funds in the last five years. With respect to these High Yield Bond funds, Rainier High Yield Institutional received a Morningstar Rating of three stars and four stars for the three- and five-year periods, respectively. Past performance is no guarantee of future results. Ratings for other share classes may differ.

The BofA Merrill Lynch U.S. High Yield Index tracks the performance of below investment grade, but not in default, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market, and includes issues with a credit rating of BBB or below, as rated by Moody's and S&P The BofA Merrill Lynch US Corporate, Government and Mortgage Index is a broad-based measure of the total rate of return performance of the US investment grade bond markets. The Index is a capitalization weighted aggregation of outstanding US treasury, agency and supranational, mortgage pass-through, and investment grade corporate bonds meeting specified selection criteria. The BofA Merrill Lynch US Treasury & Agency Index tracks the performance of US dollar denominated US Treasury and nonsubordinated US agency debt issued in the US domestic market. The S&P 500® Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

Credit Quality weights by rating are derived from the highest bond rating as determined by Standard & Poor's ("S&P"), Moody's or Fitch. Bond ratings are grades given to bonds that indicate their credit quality as determined by private independent rating services such as S&P, Moody's and Fitch. These firms evaluate a bond issuer's financial strength, or its ability to pay a bond's principal and interest in a timely fashion. Ratings are expressed as letters ranging from 'AAA', which is the highest grade, to 'D', which is the lowest grade. In limited situations when none of the three rating agencies have issued a formal rating, the Advisor will classify the security as nonrated.

High yield bonds have a lower credit rating than investment-grade corporate bonds, Treasury bonds and municipal bonds. Due to the higher risk of default, these bonds pay a higher yield than investment grade bonds. Fixed income refers to any type of investment under which the borrower/issuer is obliged to make payments of a fixed amount on a fixed schedule. Equities, or stocks, represent an ownership of the company some pay dividends but do not offer interest.

Definitions: Correlation is a statistical measure of how two securities move in relation to each other. The Sharpe ratio measures the excess return per unit of deviation in an investment asset or a trading strategy. Basis point is one-hundredth of one percent, or 0.01%. For example, 20 basis points equal 0.20%. Cash flow represents earnings before depreciation, amortization, and non-cash charges. Standard Deviation is a measure of how much an investment's returns can vary from its average return.