"In spite of the cost of living, it's still popular." Kathleen Norris

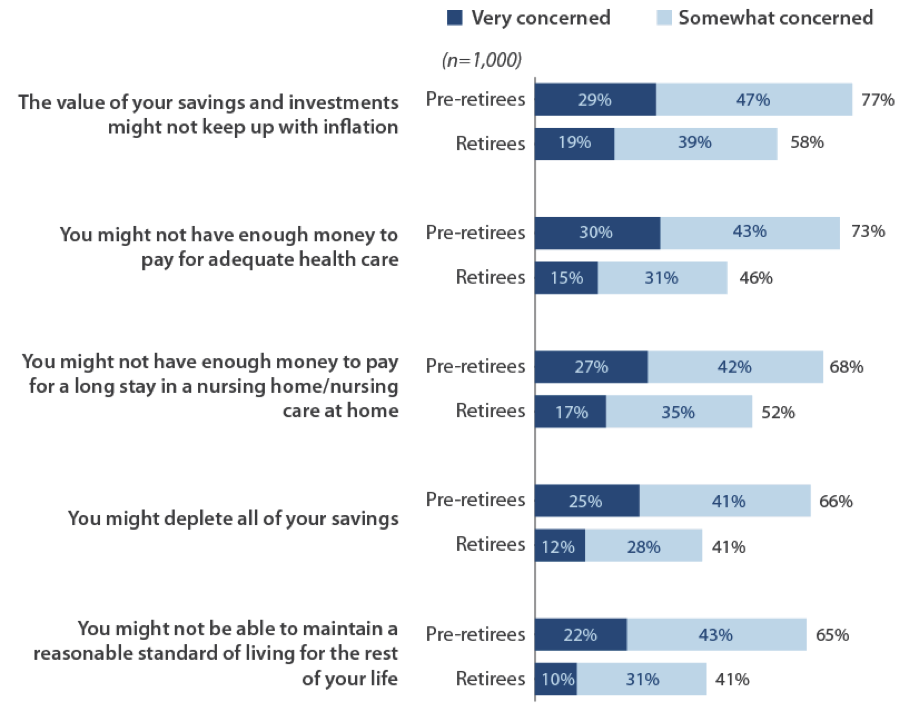

These words offered by Kathleen Norris decades ago carry more weight than ever before, particularly within the realm of financial planning and saving for retirement. The evolution of medical technology and advancement of life-extending therapies once referenced only in science fiction movies have significantly magnified the implications of longevity for today's investors. The Society of Actuaries' 2013 investor retirement planning survey reports that 66% of pre-retirees and 41% of retirees surveyed expressed concerns of having enough in savings to adequately support them throughout their retirement years.¹ Other highly ranked concerns include keeping up with inflation and having enough in savings to pay for adequate health care.

Their concerns are valid, especially when we consider that global interest rates are hitting previously unimaginable lows. Some regions now offer negative interest rates (not a typo) accompanied by higher market volatility, geopolitical uncertainty, and continued increases in the cost of living that together create vexing challenges.

Considering our current market environment, financial planning for longevity ought to consider not only the preservation of assets but also liability management. An unexpected and significant liability can impair your investments and savings and prevent you from adequately funding your retirement. While beyond the scope of this article, active review of insurance policies that address property losses, long-term insurance coverage, and longevity funding through use of annuities can fill a gap in hedging these undesired risks.

How concerned are you about each of the following (in retirement)?

Source: Society of Actuaries, Matthew Greenwald & Associates, Inc.

From an asset management perspective, withdrawal rates rank near the top of concerns regarding adequate retirement funding. In the not-so-distant past, investors confidently employed a rule-of-thumb withdrawal rate of 5% to 6% so as not to impair their portfolio principal while providing sufficient funding throughout retirement. However these long-held withdrawal rate assumptions are being questioned within professional and academic financial circles as being potentially too high, inadvertently causing investors to experience a shortfall in their savings.

It is incumbent on pre-retirees and retirees to revisit their budgeting and spending assumptions with regard to updated life expectancy rates to determine whether they are realistic and/or adequate. Larry Zimpleman, chairman and chief executive officer of Principal Financial Group, recently cautioned, "The biggest misconception I see about retirement accounts is that what might seem like a large amount (say $500,000) may well turn out to be insufficient when you take account of increasing life expectancies and the current low level of interest rates."² Given that there is a 50% chance that one or both of members of a couple age 65 today will live to age 90 (meaning they'll spend 25 years in retirement), Zimpleman believes new rules of thumb dictate a combination of lower withdrawal rates (3.5% to 4%) and higher retirement savings balances (in the range of $800,000 to $1 million).

For investors with multiple accounts, the objective is to delay withdrawal from qualified retirement investment accounts as long as possible to retain the benefits of tax deferral as those accounts continue to compound. Retirees should focus on withdrawing from taxable accounts prior to qualified retirement accounts. Of course, this is not always possible. Required minimum distribution rules, otherwise known as RMDs, dictate the timing and amounts of qualified account withdrawals. With the exception of Roth IRAs, account holders must begin receiving distributions at the age of 70½. Ideally one would want to draw from other taxable investment accounts to fund living expenses while withdrawing only the required minimum from qualified accounts. It is extremely important that the RMD withdrawals are met as scheduled else you may face potential tax penalties of 50%. Under such circumstances it is advisable to seek individual tax guidance.

If you currently hold your former employer's publicly traded stock in your qualified retirement account, you'll want to examine the rules associated with net unrealized appreciation (NUA) as an alternative means of reducing your tax on withdrawals. The benefit of an NUA is that proceeds from the sale of such stock are treated as a long-term taxable gain rather than a withdrawal taxed at your (typically) higher income tax rate.

Suppose, for example, that you worked at a company that offered stock currently valued at $100,000. Further suppose that your cost basis is $25,000 based on purchases made many years ago and that your current taxable income rate is 35%. Lastly, under this hypothetical example you decide to withdraw the entire $100,000 from your account. Under an NUA-specified withdrawal your taxable liability would be $15,000, a 20% long-term tax assessed against the long-term gain of $75,000, versus a $26,250 tax based on your current tax rate of 35%. This, too, may require the assistance of a qualified tax advisor, because if done incorrectly it cannot be reversed.

In addition to tax management, it is also important to consider when to tap your Social Security benefits. The longer you can defer benefits the better, because each year you delay your benefits Uncle Sam will increase your annual payments by approximately 8%. When you consider the current low interest rate environment, an 8% annual increase guaranteed by the US government warrants merit.

Let's examine a hypothetical scenario. If you were born in 1960, your full retirement age (FRA) is 67, with partial retirement benefits available as early as 62 (at 70% of your monthly FRA benefit). If, however, you defer your Social Security benefit payments until age 71, you could expect to receive approximately 130% of your FRA monthly benefit.³ Alternatively, you could begin taking Social Security payments earlier and invest them, thereby creating an additional savings pool. Ultimately, circumstances regarding your health, family longevity characteristics, retirement plans, gift planning, and other personal factors will determine whether and/or how long you can defer benefits. Professional services offered by a Certified Financial Planner® along with resources provided by the Social Security Administration can assist the decision process.

Another area that can affect your retirement savings pool is asset allocation, which refers to your proportional exposure to bonds, stocks, real estate, and other investment assets. If done appropriately, your asset allocation reflects your risk tolerance and is structured to accomodate your individual investment time horizon, liquidity needs, tax considerations, and desired long-term rate of return. Historically, investors employed a simple meme to assist in their asset allocation by subtracting their age from 100 and using this as a proxy for stock allocation. For example, a 65-year-old male investor would allocate 35% of his investments to stocks (100 – 65 = 35). The problem is that according to Social Security life expectancy tables, that same 65-year-old man with an average health profile can be expected to live to age 84. This leaves him with another 20 years predominantly exposed to fixed income investments that are not structured to grow income during his retirement years. It is important to point out that these are just averages. About one out of every four 65-year-olds today will live past age 90, and one out of 10 will live past age 95.4

A Forbes Magazine article catchily titled "Americans Clueless About Life Expectancy, Bungling Retirement Planning" adeptly points out "once folks get the notion that half of the people will outlive the average life expectancy of their age group...they need to revisit their financial planning time horizon."5 Ultimately this may be another instance of conventional wisdom gone obsolete. The combination of a lower interest rate environment and longer life expectancies leading to longer investment time horizons may require higher exposure to investment assets that offer greater income potential through growth than fixed income-producing assets. Such a substitution may include dividend-paying stocks with the potential to increase income over time.

Retirement planning is a continuous process that does not end on the date of your retirement. The earlier you can begin, the better chance you have of achieving the retirement lifestyle you hope for. Active planning and careful, regular reviews of your asset allocation, tax considerations, and Social Security strategy can improve the likelihood that that your proverbial golden years are enjoyed to the fullest extent.

Footnotes

¹ 2013 Risks and Process of Retirement Survey Report of Findings. Society of Actuaries, December 2013. Figure 163: Issues of Concern, page 94. https://www.soa.org/files/research/projects/research-2013-retirement-survey.pdf

² Common Retirement-Account Misconceptions. At A Glance Blog, January 1, 2015. WSJ.com. http://blogs.wsj.com/briefly/2015/01/01/common-retirement-account-misconceptions-at-a-glance

³ Social Security Administration. When To Start Receiving Retirement Benefits. http://www.socialsecurity.gov/pubs/EN-05-10147.pdf

4 Social Security Administration Life Expectancy Calculator. http://www.ssa.gov/planners/lifeexpectancy.html

5 Ebeling, Ashlea. Americans Clueless About Life Expectancy, Bungling Retirement Planning. Forbes, August 10, 2012. http://www.forbes.com/sites/ashleaebeling/2012/08/10/americans-clueless-about-life-expectancy-bungling-retirement-planning/

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held US stocks. The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Index is comprised of US small cap stocks and measures the performance of the 2,000 smallest US companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than 5,000 US and non-US companies traded "over the counter" through the National Association of Securities Dealers Automated Quotation system. The MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay's Capital US Aggregate Bond Index measures the performance of the US bond market.

All indices shown are widely recognized, unmanaged indices of common stock and bond prices that reflect no deductions for fees, expenses, or taxes. Investors cannot invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.

Copyright 2015 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 9 · No. 3