The first quarter 2015 earnings season is virtually over and the results relative to lowered expectations were quite good. Investors were braced for an earnings decline and the possible start of an “earnings recession,” but it looks like they will end up with a better than feared, year-over-year earnings growth rate of about 2%, according to Thomson Reuters data. This pace is impressive considering the significant drags from the oil downturn and strong U.S. dollar. Here we recap the first quarter 2015 earnings season and share our earnings outlook for the rest of 2015.

STEEP UPHILL CLIMB

With 90% of S&P 500 companies having reported, the S&P 500 is on track to produce a year-over-year earnings growth rate of about 2% in the first quarter of 2015. That doesn’t sound like much — and it isn’t. But given the steep uphill climb that corporate America faced due to the twin drags of the oil downturn and strong U.S. dollar, this is actually a good result. Consensus estimates were calling for a nearly 3% drop in earnings when reporting season began, which means that should remaining reporting companies meet estimates, S&P 500 companies would deliver an upside surprise of about 5%, better than the four-quarter average of 4% upside and the long-term average upside of about 3% (since Thomson began tracking this data in 1994).

Keep in mind earnings figures may vary depending on the source (Thomson, FactSet, Bloomberg, etc.). Data providers have different methodologies for calculating S&P 500 earnings, and different interpretations of what constitutes operating earnings as compared with reported (GAAP) earnings. But in general, we favor the Thomson data series’ long history.

So, which sectors drove the upside?

· Healthcare (10% upside surprise). Biotech remains the biggest driver of the sector’s earnings gains. Not only has the sector registered the biggest earnings upside surprise thus far, but its earnings growth rate (17.5%) tops all sectors. Demand from the Affordable Care Act, evident in the strong earnings growth for healthcare facilities companies, and drug innovation are helping drive broad-based growth for the sector.

· Energy (6% upside). Strength in refining, effective cost management, and less currency drag than analysts expected are among the factors that contributed to the energy sector’s better than expected performance this earnings season as oil prices fell during the first quarter. Services and equipment companies within the sector suffered smaller losses, although the broad sector is still tracking to a massive 58% decline.

· Technology (5% upside). The biggest market cap company in the S&P 500 is also the most profitable (Apple, of course), giving it an outsized influence over the technology sector earnings performance. Apple, with its 34% increase in earnings in the first quarter of 2015, contributed 1.3% to overall S&P 500 earnings growth.

· Financials (5% upside). Financials are on track to produce double-digit earnings growth after solidly outpacing initial earnings expectations, driven in part by an improved trading environment, strong equity capital markets activity, an active merger and acquisition environment, a shrinking — although still onerous — regulatory and legal burden, and a relatively healthy credit environment. These factors helped offset the drag from lower interest rates that reduce bank and insurers’ profitability.

INDUSTRIALS STRUGGLE

The industrials sector was the only 1 of the 10 equity sectors to miss expectations. The sector faced a very steep uphill climb from the strong U.S. dollar and heavy overseas exposure. A strong dollar makes U.S. industrial equipment more expensive for overseas buyers and negatively impacts foreign-sourced earnings through currency translation. The sector’s energy equipment manufacturers and transportation providers were hurt by the oil downturn, as they build energy infrastructure and transport oil and other commodities. Energy is the biggest sector in terms of capital spending, which has been cut dramatically and has reduced industrial sector revenue.

Many industrial companies were also impacted by the West Coast port strikes and adverse weather that hurt the U.S. economy during the first quarter of 2015. Considering these challenges, we think the 5% earnings gain the sector is on track to deliver in Q1 2015 is respectable. We believe the sector’s current (and we think temporary) softness is priced in — the sector trades at a 4% discount to the S&P 500 on a forward price-to-earnings basis (as of May 8, 2015). This compares with the 20-year average relative valuation of a 3% premium. We expect better economic growth to help drive improved sector performance over the rest of the year. The S&P industrials sector has returned just under 1% year to date, compared with the 3.5% return for the S&P 500, but has outperformed the S&P 500 so far in May, despite the earnings shortfall.

BROADER EARNINGS THEMES

Several broad themes have emerged during earnings season:

· Slower U.S. economic growth. Slower growth was evident in the revenue decline during the quarter and in commentary from management teams across multiple industries. Although the energy decline and strong dollar were a big part of the revenue softness, it is clear that the slowdown in U.S. economic growth was a factor in 56% of S&P 500 companies missing consensus revenue forecasts thus far. Revenue is more directly correlated with economic growth than earnings.

· Better growth in Europe. A better growth environment in Europe has been helpful to U.S. multinationals. While currency impacts hurt foreign-earned revenue, a currency drag on the U.S. is a currency benefit for Europe. European companies are enjoying one of their strongest earnings seasons relative to expectations in several years.

· Stellar cost management. Profit margins remain near record highs for S&P 500 companies despite the drags from the energy sector and strong dollar. Some of the profit margin story is low borrowing costs and low input costs from commodities price weakness. But slow wage gains — evident in Friday’s jobs report — and the impressive efficiency of corporate America are also factors.

LOOKING AHEAD

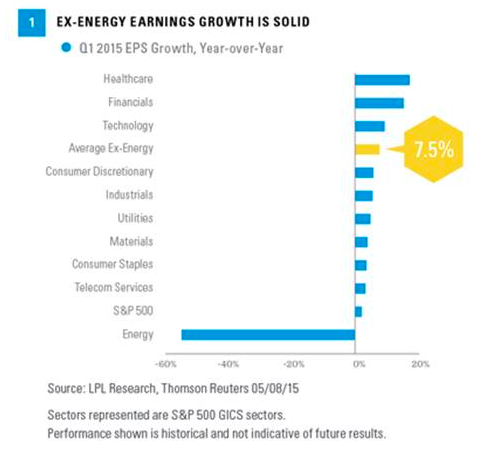

These factors all contributed to the solid overall results, which are quite evident when breaking out energy, as we did in Figure 1. If the energy sector is excluded, the average S&P sector is on track to produce an average earnings gain of 7.5%.

The first quarter 2015 earnings season hasn’t been great, but the picture brightens as we look ahead. We expect U.S. economic growth may pick up in subsequent quarters — aided by better weather and fully operational ports — and we were encouraged by the rebound in jobs in April 2015 after March weakness. Oil prices have rebounded, which should help the energy sector return to earnings growth over the next several quarters. The dollar rally has already begun to slow. We see no reason that corporate America cannot potentially keep profit margins high given our outlook for wages, interest rates, and even commodity prices. Although the benefits of lower gas prices have started to wane, the consumer remains in good shape overall. Hitting our 5 – 10% S&P 500 earnings growth target for 2015 may be difficult, but we see upside to current Thomson-tracked consensus estimates for a 1.5% increase.

CONCLUSION

Relative to lowered expectations, first quarter earnings results were quite good. An “earnings recession” may still occur (though not our view), but the S&P 500 produced positive earnings growth during the first quarter despite the stiff headwinds from the oil downturn and the strong dollar. The modest first quarter earnings increase, combined with our increased confidence in better earnings growth through year-end, leave us comfortable with our 5 – 9% total return forecast for the S&P 500 in 2015.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

DEFINITION

Forward price-to-earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. While the earnings used are just an estimate and are not as reliable as current earnings data, there is still benefit in estimated PE analysis. The forecasted earnings used in the formula can either be for the next 12 months or for the next full-year fiscal period.