In our February commentary Identifying Global Growth Opportunities Through A Thematic Lens, we shared our constructive view on growth stocks. We continue to believe investors should favor growth over value, given fundamentals, valuations and secular opportunities.

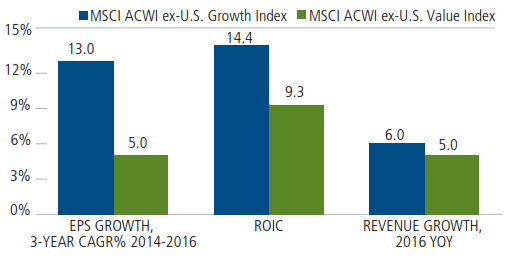

FIGURE 1. GROWTH FUNDAMENTALS ARE CONSIDERABLY BETTER

International growth equities have generated higher revenue and earnings growth and delivered better capital efficiency, as reflected in a higher return on invested capital (ROIC) relative to value.

Source: Bloomberg. May 2015

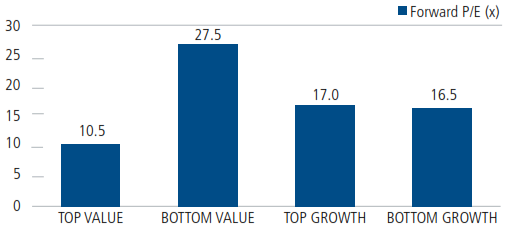

FIGURE 2A, 2B. GROWTH IS INEXPENSIVE VS. VALUE

When growth is scarce, we believe the market should award a premium for growth. However, this is not the case in today’s market environment as there is very low differentiation in high and low growth valuations. In our view, international markets are not adequately rewarding higher growth versus lower growth. The top and bottom growth companies by decile have almost the same P/E valuation, while the top versus bottom value companies by decile show major differentiation.

Source: BofA Merrill Lynch, using data from BofA Merrill Lynch research and FactSet. April 2015. Data represents European equities.

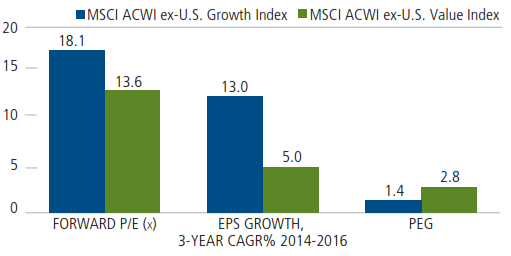

International growth trades at a higher P/E, but this is reflective of a significantly higher earnings growth profile. On a growth adjusted basis (PEG ratio), the growth index’s PEG ratio is half that of value.

Source: Bloomberg. May 2015.

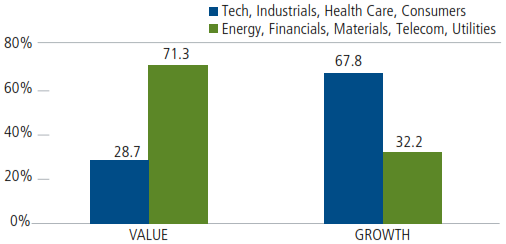

FIGURE 3. GROWTH COMPANIES ARE POSITIONED TO BENEFIT FROM SECULAR TAILWINDS

We believe growth equities offer much higher exposure to more dynamic parts of the global economy, including technology, industrials, health care and consumer sectors.

Source: S&P Capital IQ. April 2015. Value represented by the MSCI ACWI ex-U.S. Value Index. Growth is represented by the MSCI ACWI ex-U.S. Growth Index.

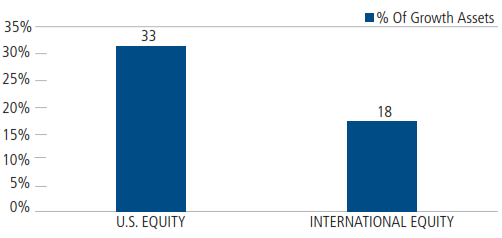

FIGURE 4. INTERNATIONAL GROWTH IS UNDERREPRESENTED

Only 18% of international stock assets are currently invested in growth. In an asset class that is mostly defined by core and value offerings, investors may be missing out on compelling growth opportunities driven by secular growth trends, including a burgeoning global middle class.

Source: Morningstar. April 2015. The percentages are based on Morningstar U.S. mutual fund category assets in the International Stock and U.S. Stock broad asset classes. In the U.S. stock asset class, the growth category in the graphic is represented by Growth Morningstar category (small, mid, and large cap combined). In the International Stock asset class, growth represents the combined assets of Foreign Large Growth and Foreign Small/Mid Growth categories. Morningstar defines growth companies as those that have high price ratios and higher growth rates for earnings, sales, book value and cash flow. Morningstar defines value companies as those that have low price ratios and slower growth rates in earnings, sales, book value and cash flow.

--

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice. The information in this report should not be considered a recommendation to purchase or sell any particular security. The views and strategies described may not be suitable for all investors.

As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

The MSCI ACWI ex-U.S. Value Index captures large and mid cap securities exhibiting overall value style characteristics across 22 developed and 23 emerging markets countries. The MSCI ACWI ex-U.S. Growth Index captures large and mid cap securities exhibiting overall growth style characteristics across 22 developed markets countries and 23 emerging markets countries. Price-toearnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Earnings-per-share (EPS) is the portion of a company’s profit allocated to each share of common stock. CAGR, or compounded annual growth rate measures year-over-year growth. ROIC (return on invested capital) measures how effectively a company uses the money invested in its operations, calculated as a company’s net income minus any dividends divided by the company’s total capital. PEG is a stock’s price/earnings ratio divided by estimated earnings growth rate; a lower PEG indicates that less is being paid for each unit of earnings growth.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© 2015 Calamos Investments LLC. All Rights Reserved. Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC. IGVALCOM 2407 0515O C