Strong Demand for Chicago Bonds Shows It’s No Detroit

Moody’s Investors Service recently downgraded Chicago’s $8.1 billion of outstanding general obligation (GO) debt two notches to Ba1, officially putting the bonds in the “junk” rating category1, after a May 8 ruling by the Illinois Supreme Court struck down a law overhauling state employee and teacher pensions, narrowing the city’s options for curbing growth in its unfunded pension liabilities.

Moody’s also said the negative outlook for Chicago reflects its expectations that the city’s credit quality will “weaken” as unfunded liabilities of the city’s four pension funds2 grow and exert increased pressure on the city’s operating budget.3

The downgrade and negative outlook caused investors to question whether demand for bonds issued by the nation’s third largest city would slow. In late April Mayor Rahm Emanuel announced a plan to convert $900 million of variable-rate debt to fixed-rate debt, a deal which would soon test the market’s demand for Chicago’s GO bonds.

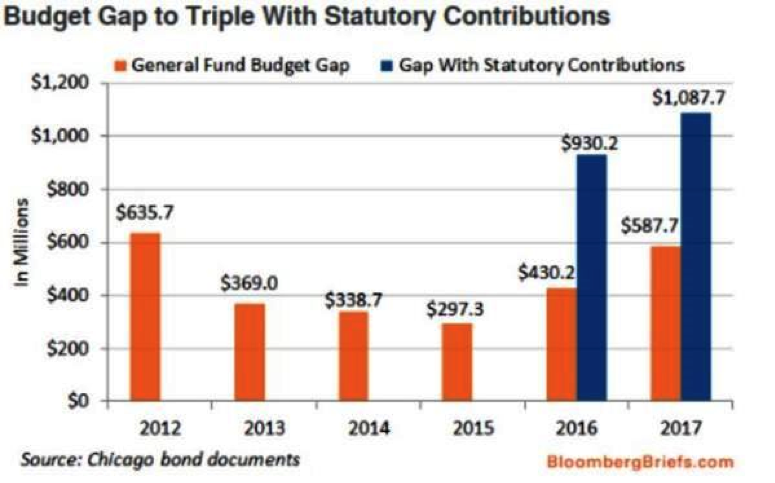

We believe that even if Mayor Emanuel’s plan is successful Chicago will not be out of the woods. The city’s ability to negotiate lower pension payments will be the key to stemming the need for additional borrowing, which is highlighted in the following chart:

Successful new issuance comes at a price

On May 27, the City of Chicago issued $668 million of new general obligation bonds.4 These bonds remarketed and converted variable rate securities into fixed rate debt, removed some of the city’s bank lending positions and terminated various interest rate swap agreements. The four bond issues resulted in $6 billion in market orders, nearly 10 times oversubscribed.4

We believe this exceptionally strong demand shows that investors are still confident in the city’s credit and economic potential. While the downgrade placed Chicago alongside Detroit among the ranks of cities whose bonds are considered to be “junk,” the high demand for the new issue shows that, over the long term, economic sentiment differs between the two cities.

Though successful, Chicago’s new issue comes at a cost. Compared with the Municipal Market Data’s5 AAA-rated benchmark, pricing for the 10-year maturities came at a spread of 293 basis points (bps), and pricing for its longest 27-year maturities came at a spread of 264 bps — extremely attractive for buyers. This is in stark contrast to the 145 bps the city paid when it last priced 10-year GOs in June 2014, and is an even more glaring change from the 84 bps spread it paid in 2013.4

Key takeaway

Overall, we believe the market is lending credence to Chicago’s future reform proposals, including several changes expected to be proposed for the city’s four pension plans, which are underfunded by about $20 billion. Regardless of how the attempted reforms play out in Illinois courts over the next few months, we believe the result of the new financing – plus an additional $200 million in credit from JPMorgan and Morgan Stanley – improves Chicago’s liquidity position as it fights to maintain investment-grade ratings from both S&P and Fitch.

1 The City of Chicago, IL’s general obligation (GO) debt was downgraded from Ba1 from Baa2.

2 Municipal, Laborer, Police, and Fire pension plans

3 Source: Moody’s Investor Service Chicago, IL Rating Action Report May 12, 2015

4 Invesco Fixed Income and BondBuyer, May 27, 2015

5 Thompson Reuters

Important information

A general obligation bond is backed by the credit and taxing authority of the issuer. It is not backed by revenue from a given project.

Variable rate securities have interest rates that fluctuate. The interest rate on fixed rate debt does not change.

An interest rate swap agreement is an exchange of interest payments between counterparties. The interest payments are based on a specified principal amount.

A basis point is one hundredth of a percentage point.

A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice. NR indicates the debtor was not rated, and should not be interpreted as indicating low quality. For more information on rating methodologies, please visit the following NRSRO websites: standardandpoors.com and select `Understanding Ratings’ under Rating Resources on the homepage; moodys.com and select `Rating Methodologies’ under Research and Ratings on the homepage; fitchratings.com and select `Ratings Definitions’ on the homepage.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.All data provided by Invesco unless otherwise noted.

©2015 Invesco Ltd. All rights reserved. Strong Demand for Chicago Bonds Shows It’s No Detroit by Invesco Blog