Recovery Rallies, Is Six Years Enough

Recovery Rallies, Is Six Years Enough?

The stock market advance that began early March 2009, recently passed the six year mark. It seems like almost daily some analyst being interviewed on TV or in print proposes that the end of the advance is near. When we listen closely, we do not hear any specific reasons given. Occasionally an analyst will offer statistics such as the average length of previous bull markets, but overall we sense that their reason is simply intuition that six years feels long enough. But is it?

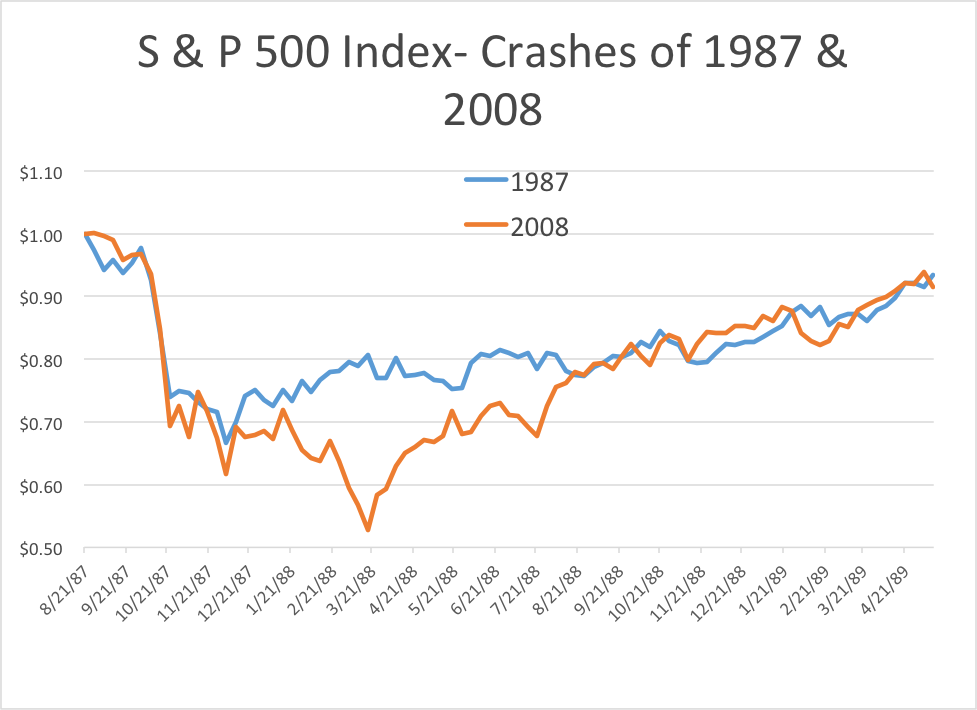

As you may recall, the end of the previous bear market and the transition to the current bull market featured a severe drop one week in early October 2008. As the drop spanned six trading days, it was not labeled a “crash.” When graphed using weekly data, that drop appears similar to the crash of October 1987. The graph below shows the S&P 500 Index (using weekly data) set equal to $1.00 on both September 2, 1987 and September 4, 2008. One of the major differences between the two recoveries is that during the early stages of the 2008 recovery the market was battling a recession and traded lower for a couple of months in 2009 before reaching its bottom. Conversely in 1987 the market was not facing a recession despite many inaccurate predictions of one. Ultimately in 2009 the market rebounded by mid-March and continued on a path similar to the recovery of 1987.

We first showed this graph to audiences in early 2009, suggesting that the market could experience a multi-year post-crash recovery as it had in the late 1980s and early 1990s. On September 18, 2009 we released an article, Was that a Crash?, with a similar graph and stated, “As of September 4, 2009, the ICON valuation readings suggest the market, in general, is priced about 13% below our estimate of intrinsic value. We believe such a reading makes an upward recovery path similar to 1988 and 1989 possible and reasonable.” On April 22, 2010, in a follow up article, Back to the Future, we showed an updated version of the same data and concluded, “[I]n retrospect it seems 1987’s post-crash behavior and recovery is indicative of the recovery we are seeing today. ICON continues to see value in the market and believes that those who remain invested may be able to capture opportunities in the months ahead.”

The data quoted represents past performance, which is no guarantee of future results.

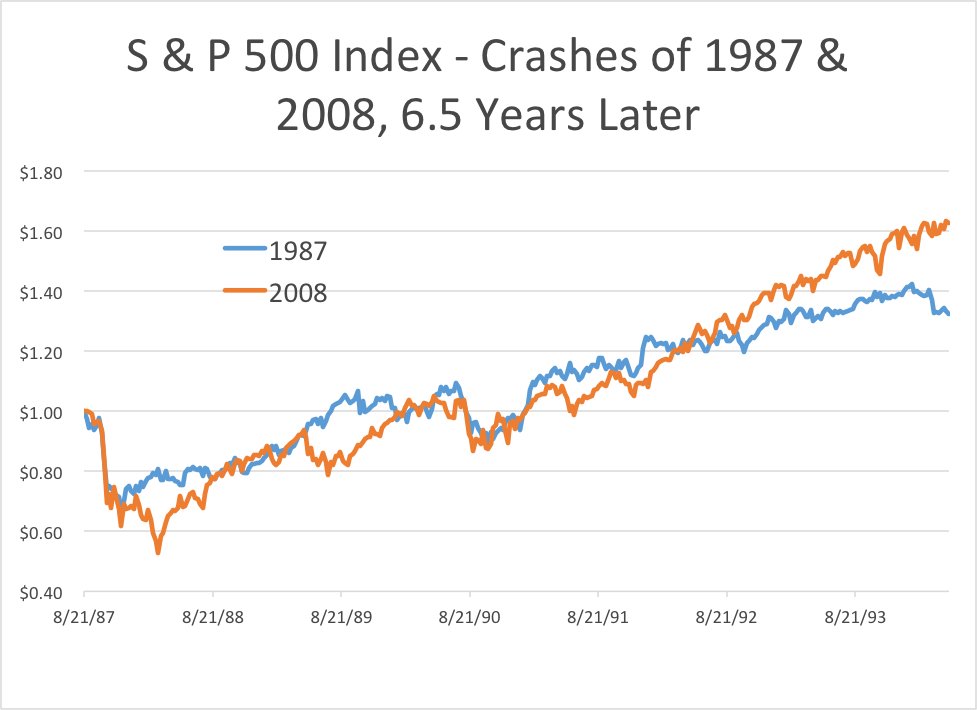

The next graph below shows the same data as the graph above, updated through six and a half years after each crash. Looking at the graph we see that on several occasions the Index reached the same value at the same elapsed time since the respective big drops, making the two post-crash recoveries appear quite similar. In the sixth year of the 1987 recovery, the market lagged the performance of the 2008 recovery over the same time span because in 1993 the Federal Reserve tightened its monetary policy to fight inflation. We think it is important to note that both recoveries have also featured “volatility events,” where the market drops in response to an event but then recovers quickly and resumes its advance. Examples of these volatility events are the European debt crises in 2010 and 2011 and the invasion of Kuwait in 1990.

The data quoted represents past performance, which is no guarantee of future results.

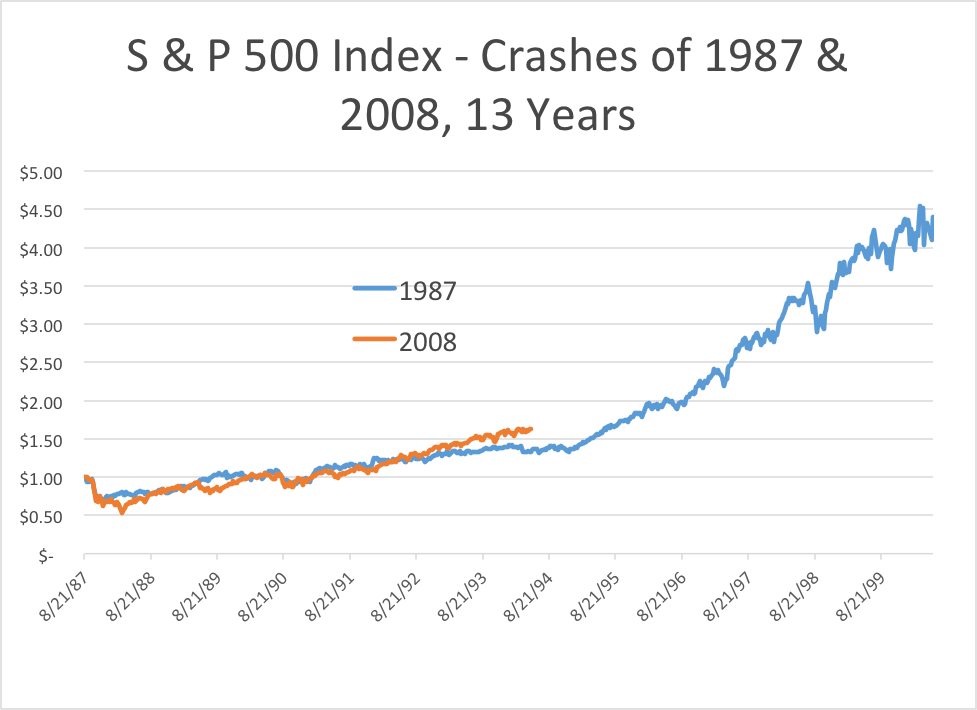

Can a bull market recovery from a crash last longer than six years? The graph below shows that the recovery from the crash of 1987 continued to the market peak of March 2000, a thirteen year run. This graph also illustrates a second volatility event in 1998, which the media labeled the “Asian Contagion” amid fears that the recession in Asia would spread to Europe and then the U.S.

The data quoted represents past performance, which is no guarantee of future results.

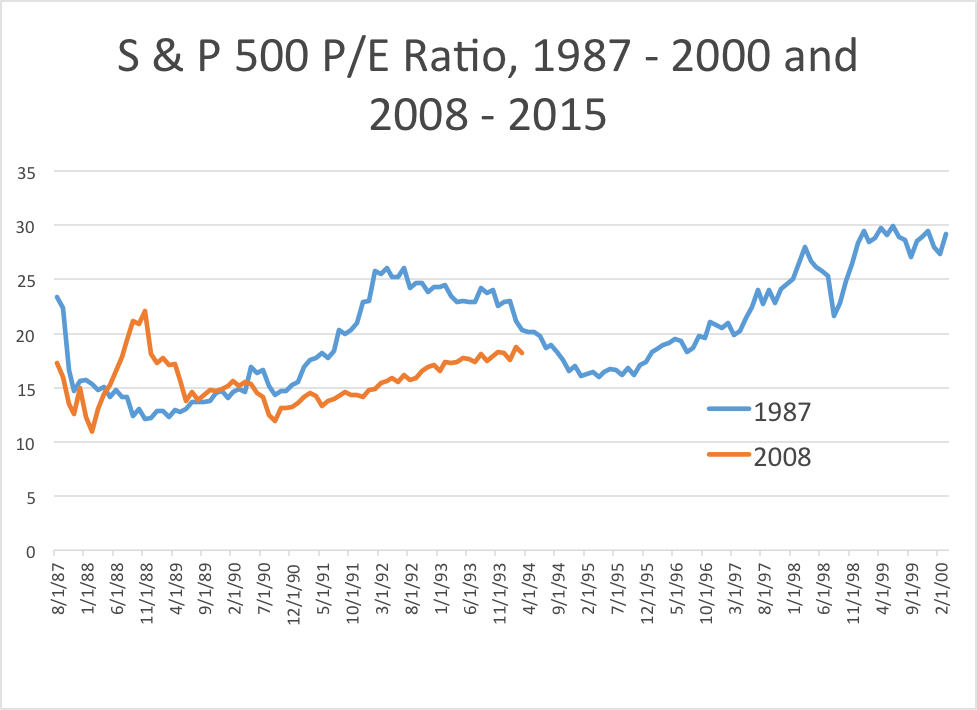

What were conditions like in the mid and late 1990s while the stock market continued its upward march? The U.S. Dollar strengthened, the price of oil was fairly stable, interest rates were declining, corporate earnings were growing, inflation was low and P/E multiples rose. All else being equal, the P/E ratio* on the S&P 500 Index can be seen as a proxy for investors’ optimism for earnings growth. The more growth investors expect in earnings, the higher multiple they will pay. The last graph below shows the P/E ratio for the S & P 500 from August 1987 through March 2000 and from August 2008 through April 2015. During both periods the P/E ratio generally increased as memories of the crashes became more distant, although the P/E path in the late 1980s and 1990s may have been more volatile. It also appears that the P/E multiple expansion in the late 1990s was a big contributor to the stock market’s advance. Can P/E ratios continue to increase this decade like they did in the late 1990s? Although expansion like we saw in the late 1990s would be simply a continuation of the gradual increase underway lately, we cannot predict investors’ behavior. We just know that one post-crash bull market lasted longer than six years and conditions and behaviors change over time.

The data quoted represents past performance, which is no guarantee of future results.

In conclusion, contrary to the bearish headlines, we at ICON believe that we are in the midst of a long-term recovery. With our valuation methodology as our guide, we believe there is enough value in the market to sustain a continued recovery. Furthermore, as we saw with the post 1987 market recovery, bull markets can last longer than 6 years. We believe there is still room for market growth in the current environment.

*ICON Advisers does not use P/E ratios for evaluating and selecting investments. Instead, we use our proprietary intrinsic value equation which incorporates earnings, expected growth in earnings, risk and corporate bond yields.

The data quoted represents past performance, which is no guarantee of future results.

Opinions and forecasts are subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry, or sector.

Investing in securities involves risks, including the risk that you can lose the value of your investment. There is no assurance that the investment process will consistently lead to successful results.

Price/Earnings Ratio is the price of a stock divided by its earnings per share.

The unmanaged Standard & Poor’s (S&P) 500 Index is a market value-weighted index of large-cap common stocks considered representative of the broad market. Total return figures for the index assume change in security prices and the reinvestment of any dividends or distributions but do not reflect deductions for commissions, management fees, and expenses.

Individuals cannot invest directly in an index.

© 2015 ICON AdvisersSM All Rights Reserved.