Global Tactical Asset Allocation is More than Just Market Timing

At our research blog GestaltU.com, we recently posted an article discussing how many noteworthy investment commentators either misunderstand or misconstrue the salient qualities of Tactical Asset Allocation strategies. In particular, we hope to clarify that:

- TAA does not require discretionary market calls;

- TAA should not be about market timing; and,

- It’s neither appropriate nor helpful to benchmark Global TAA (GTAA) funds against narrow domestic benchmarks

In Part 1 of this series we explored why quality TAA strategies do not rely on ‘expert’ market calls, noting that the terms ‘discretionary’ and ‘tactical’ ought not to be viewed as two sides of the same coin. Rather, the best tactical managers increasingly use systematic approaches to harvest persistent risk premia from factors such as ‘value’ and ‘momentum.’ This article will show why investors should not equate TAA with market timing.

First, let me be clear: tactical asset allocation is an active strategy. It involves regular shifts in portfolio composition – asset allocation – in response to changes in expected asset class returns, risks, and correlations, usually on an intermediate horizon. Some strategies are ‘binary’ in nature: a strategy will shift from 100% invested in a risky asset, such as a stock market ETF, to 100% invested in a ‘cash-like’ asset, like t-bills or Treasuries. These strategies are clearly ‘market timing’, as the goal is to be fully invested when market expectations are positive, and on the sidelines when expectations are negative.

However, market-timing strategies represent a very small sub-category within the broader TAA space. Most TAA strategies (such as Global Tactical Asset Allocation or GTAA) employ their methodology by choosing the best mix from a much broader and more diverse set of asset classes, with few ‘on-or-off’ type decisions. And there is a very powerful reason for this: market timing between two or three assets is much harder than choosing the best mix of a larger group of assets – in fact, there is reason to believe it’s more than 3x as hard!

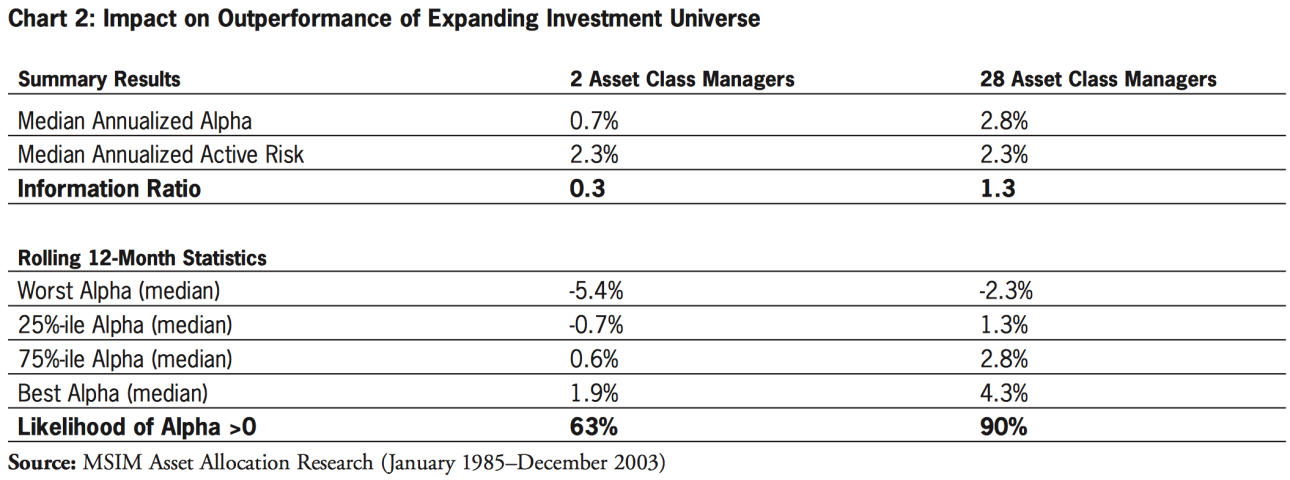

A few years ago Que Nguyen (now Director of Portfolio Strategy and Analytics at Willett Advisors, NY Mayor Michael Bloomberg’s personal investment firm) studied the expected performance from market timing between stocks and bonds (or cash) versus selecting a mix from 28 global asset classes (18 stock markets and 10 bond markets). In essence, she simulated the performance of 75 different managers, each of whom selected assets once a month at random from his eligible universe over the period 1985 – 2003, with 55% accuracy. Chart 2 from her findings, copied below, describes the results of her experiment.

Note that when the performance of market timing managers and GTAA managers was standardized for active risk, the GTAA managers delivered 4x the alpha and 4x the Information Ratio (it’s easiest to think of the Information Ratio like you would a Sharpe ratio, but where the returns are adjusted for active risk rather than standard deviation). In addition, the likelihood of achieving positive alpha was 90% for the GTAA strategies, vs. just 63% for the market timers.

The point is, a small number of TAA strategies are truly market timers who are trying to call stock market tops and bottoms, but these types of strategies are rare. Furthermore, given how hard it is to succeed as a market timer, we would expect the proportion of market timing strategies within the TAA category to decline substantially over time.

However, the vast majority of TAA strategies do not fall into the market timing camp. Rather, the best TAA strategies harness value and/or momentum effects across a much more diverse global asset universe. And since the probability of achieving strong performance is a function of the breadth and diversity of one’s investment universe, we expect these more diverse Global TAA strategies to produce the best results going forward.

Disclaimer

Butler Philbrick Gordillo and Associates is part of Dundee Goodman Private Wealth, a division of Dundee Securities Ltd.

This opinions expressed are solely the work of Butler|Philbrick|Gordillo and Associates and although the authors are registered Portfolio Managers with Dundee Goodman Private Wealth, a division of Dundee Securities Ltd., this is not an official publication of Dundee Securities Ltd. and the authors are not Dundee Securities Ltd. research analysts. The views (including any recommendations) expressed in this material are those of the authors alone, and they have not been approved by, and are not necessarily those of, Dundee Securities Ltd. Assumptions, opinions and estimates constitute the authors’ judgment as of the date of this material and are subject to change without notice. The information contained in this presentation has been compiled from sources believed to be reliable, however, we make no guarantee, representation or warranty, expressed or implied, as to such information’s accuracy or completeness.

Before acting on any recommendation, you should review the detail disclosure in this presentation and consider whether it is suitable for your particular circumstances. As no regard has been made as to the specific investment objectives, financial situation, and other particular circumstances of any person who may receive this presentation, clients should seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies discussed in this presentation. Past performance is not indicative of future results and no returns are guaranteed. Investment return and principal value may fluctuate so that an investor’s shares may be worth more or less than their original cost when sold.

This presentation is for information purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. This presentation is intended only for persons resident and located in the provinces and territories of Canada, where Dundee Goodman Private Wealth ‘s services and products may lawfully be offered for sale, and therein only to clients of Dundee Goodman Private Wealth. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country including the United States, where such distribution or use would be contrary to law or regulation or which would subject Dundee Goodman Private Wealth to any registration requirement within such jurisdiction or country. Please note that, the individuals responsible for this presentation or their associates may hold securities, directly or through derivatives, in issuers that may now or in the future be selected through the Darwin Core Diversified Strategy.

No part of this publication may be reproduced without the express written consent of Dundee Goodman Private Wealth. Dundee Goodman Private Wealth, a division of Dundee Securities Ltd, is a Member-Canadian Investor Protection Fund. Dundee Goodman Private Wealth respects your time and your privacy. If you no longer wish us to retain and use your personal information for the purposes of distributing reports, please let your Dundee Goodman Private Wealth Advisor know. For more information on our Privacy Policy please visit our website at www.dundeegoodman.com

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements.