The economy

GDP revised to negative for Q1

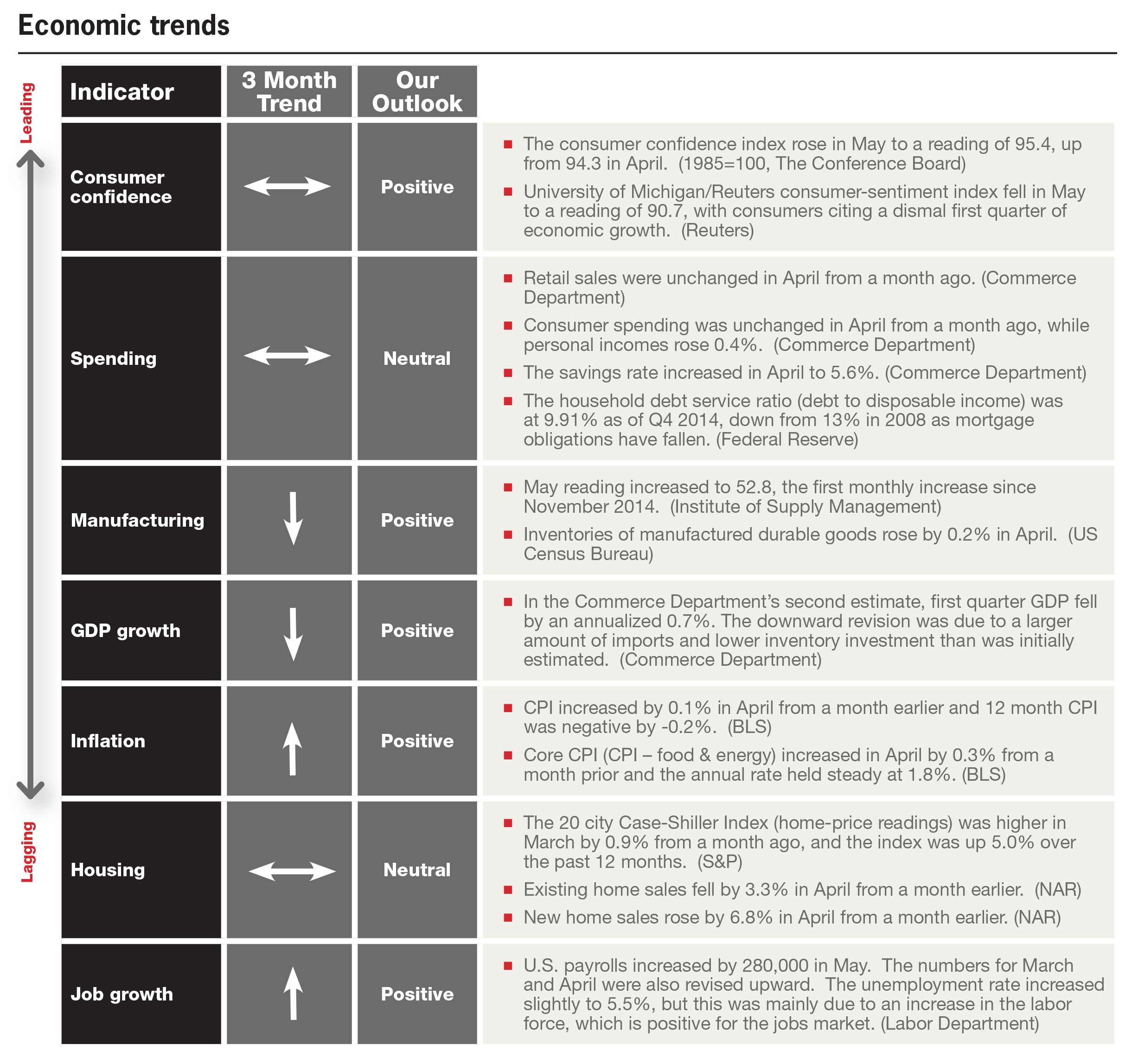

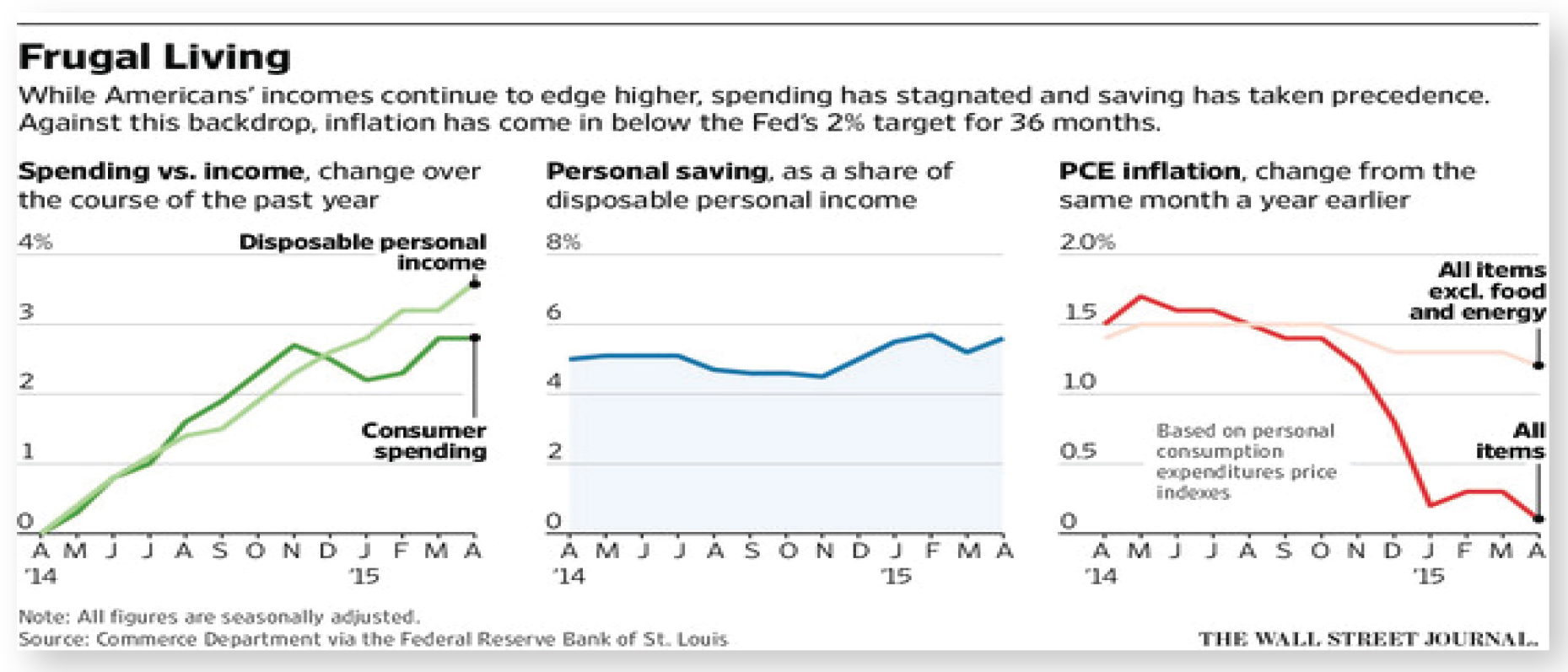

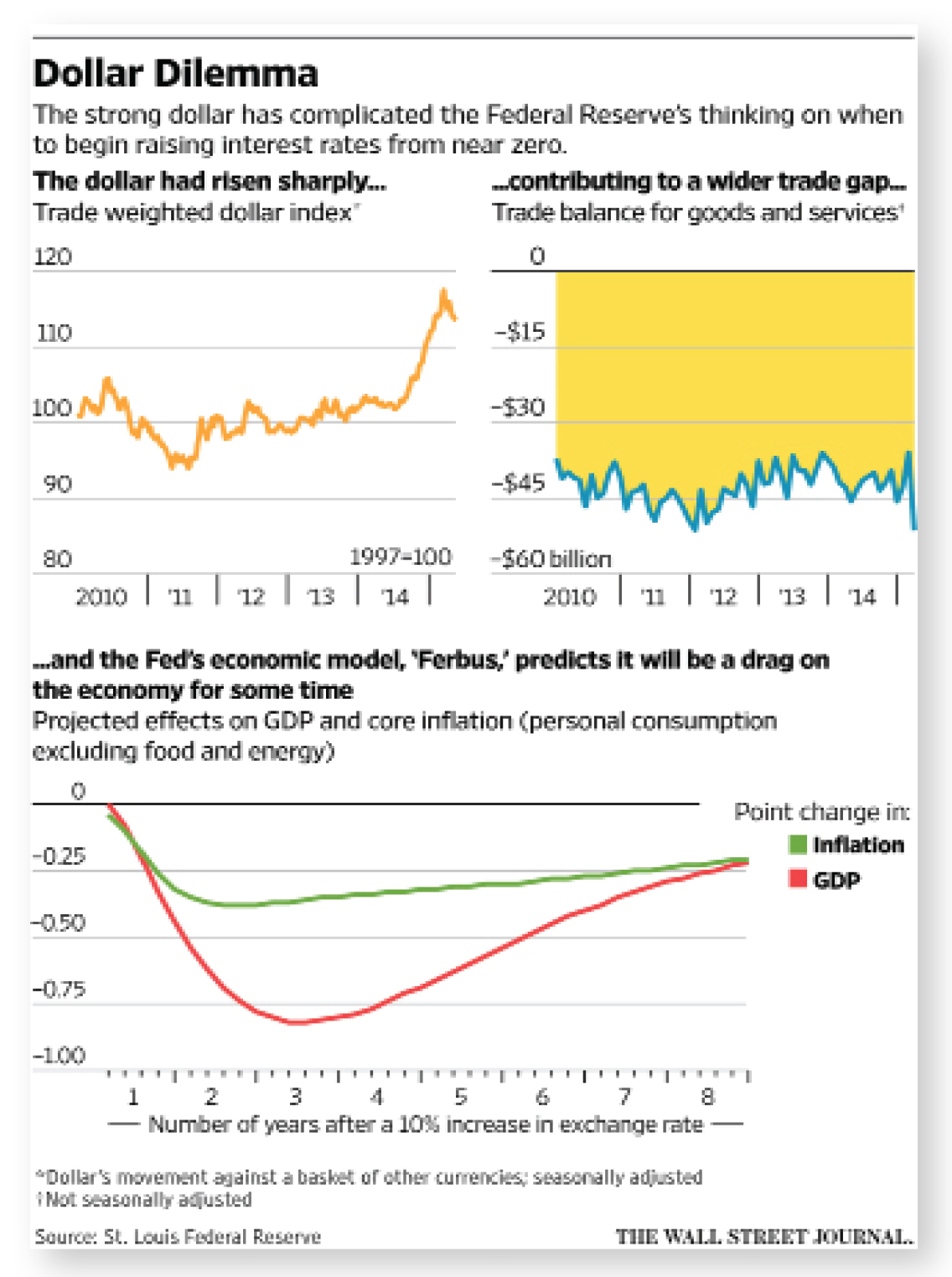

A drop in exports, poor weather, and shipping yard difficulties led the U.S. economy back into negative territory after GDP was revised downward to -0.7%. Many economists believe this is a similar situation to what we saw in 2014 with a drop in GDP during the first quarter, and a subsequent rebound in the following quarters. However, the strong dollar effect has continued into April and May and will continue to provide a headwind for GDP. The preference by consumers to save additional earnings instead of spend is also putting downward pressure on growth. Other areas of the U.S. economy are trending upward, however, with home price increases more than double the core inflation rate, and manufacturing activity picking up after several months of slowdown. The back half of 2015 looks more promising for economic growth after a weak start to the year.

The stock market

U.S. stocks trend higher, foreign markets sell off

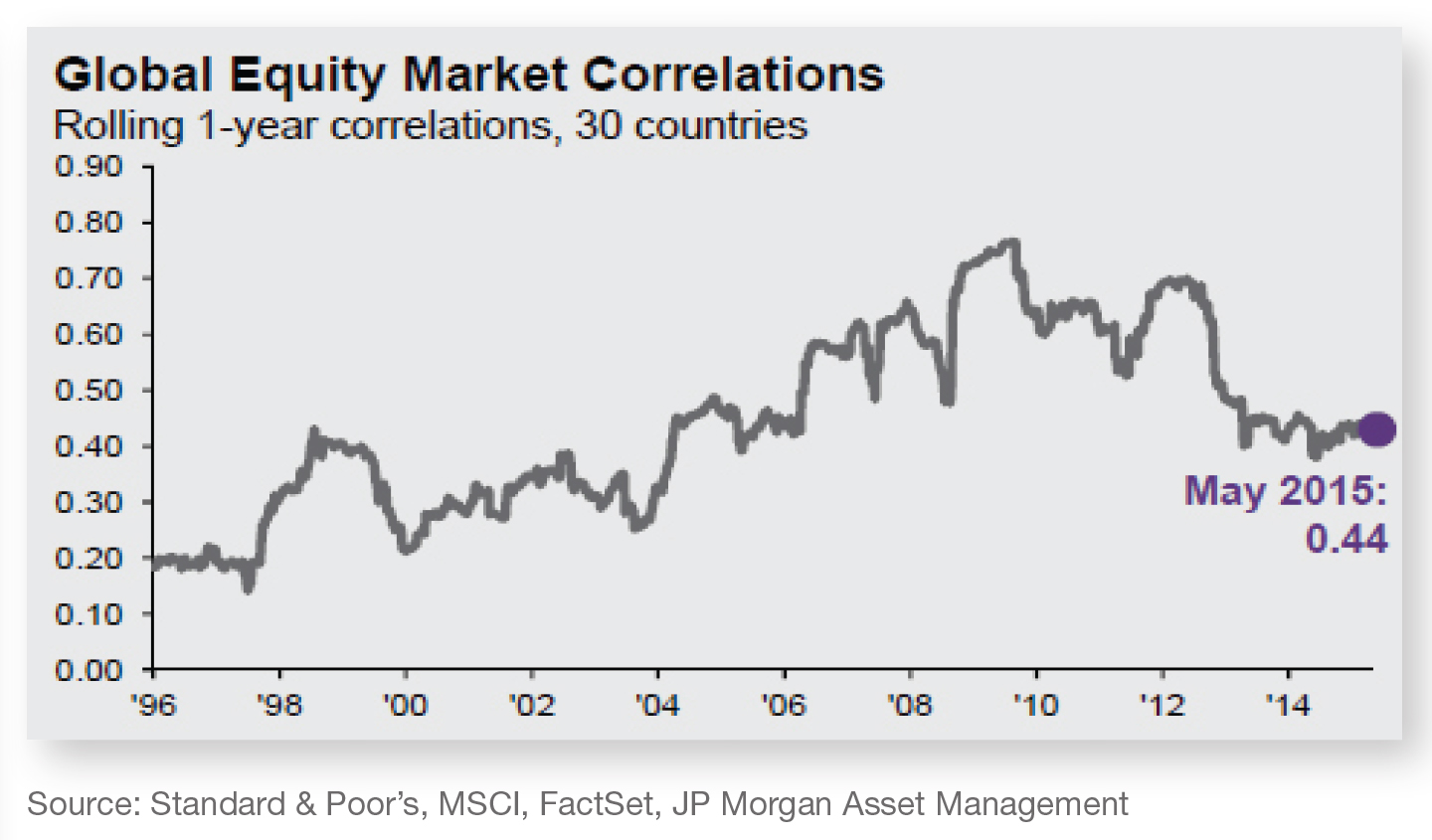

Stock markets in general moved higher in the month of May, but Emerging Market equities sold off by 4% and drove down what has been a strong start to the year for international investments. We included a chart in our stock market page that shows a decreasing level of correlation between global stocks. This factor, along with the recent increase in volatility, only emphasizes the importance to having strong foreign fund managers. With some investors questioning valuation levels in the U.S., the international markets seem to be favorable for new money. The strong dollar has continued to provide a headwind for returns, but foreign stocks have still managed to outperform in 2015.

The bond market

All eyes remain on the Federal Reserve

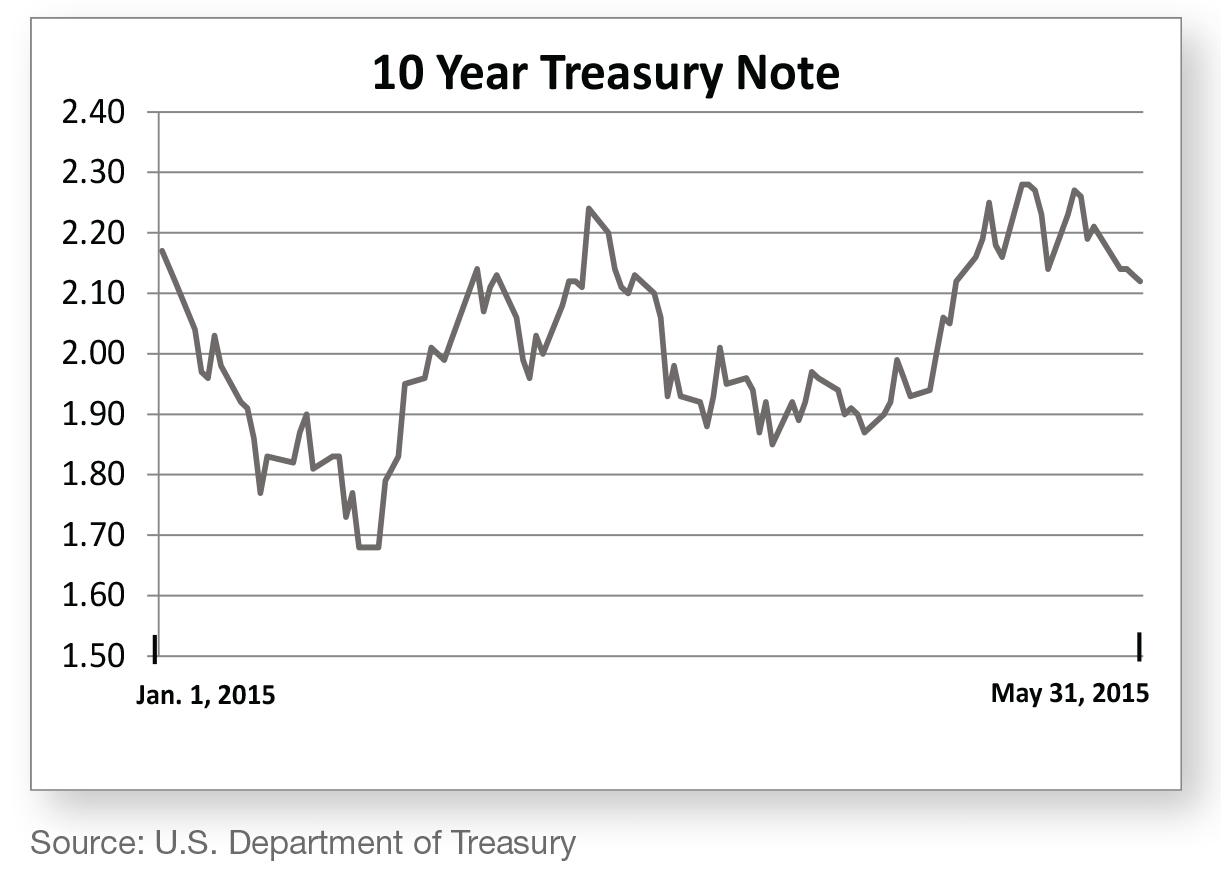

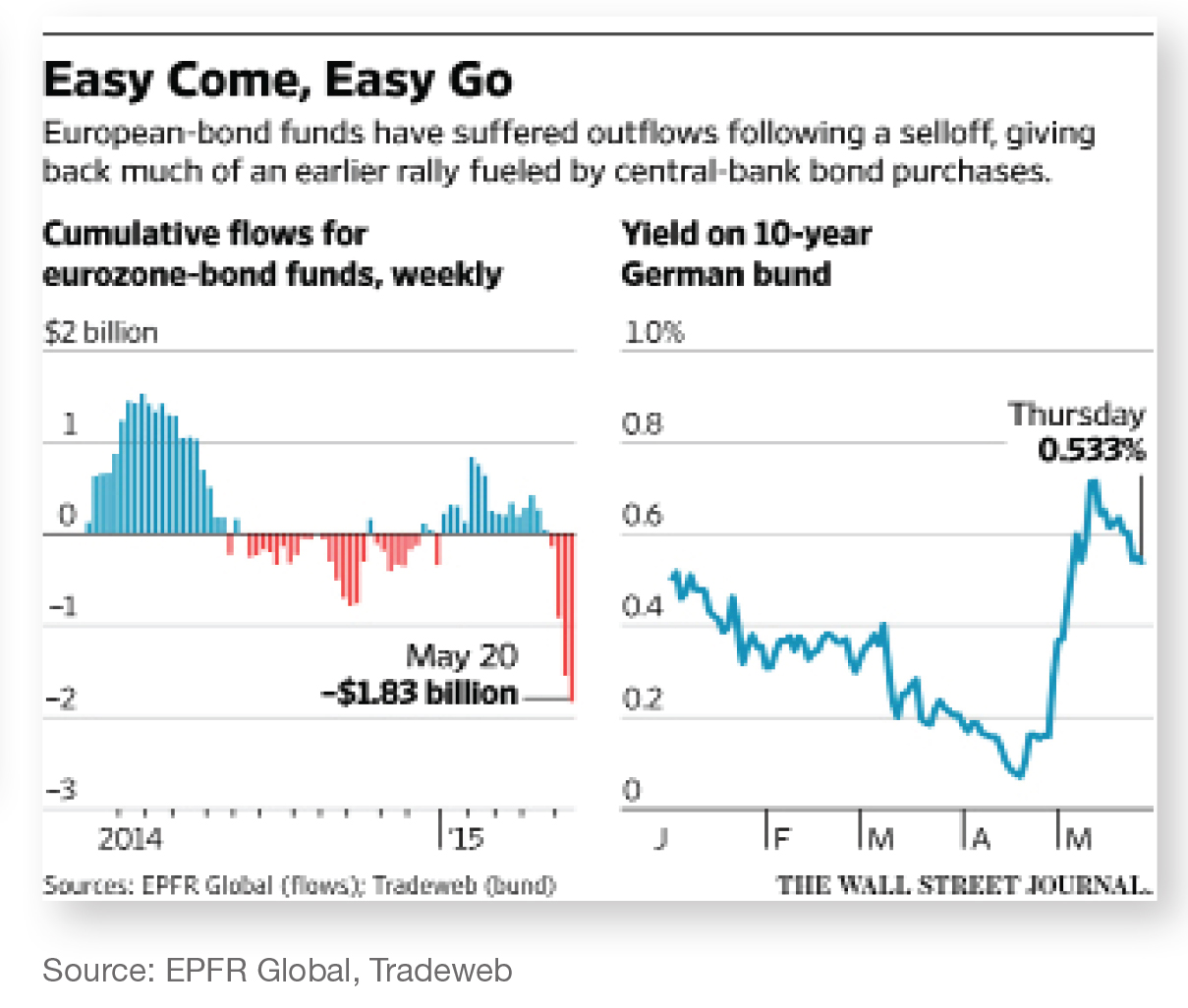

Interest rates continued their steady rise through May and closed the month back at similar levels to what we saw to start the year. The moves have been gradual enough to allow fund managers to stay positive on the year, but we did see the volatility on rate moves pick up toward the end of May. International bonds also saw rates rise in May, with the German 10 year bund back up to around 0.50%, after bottoming out at 0.05% in April. With minimal inflation and a negative GDP rate for Q1, it will be difficult for the Federal Reserve to make a rate move in 2015. While some economists are still targeting a fall rate increase, others are shifting their thinking towards early 2016. The overall flattening effect of the yield curve will likely continue through the back half of 2015 as the Fed determines its course of action on the short end and the longer end of the curve deals with an economic growth slowdown.

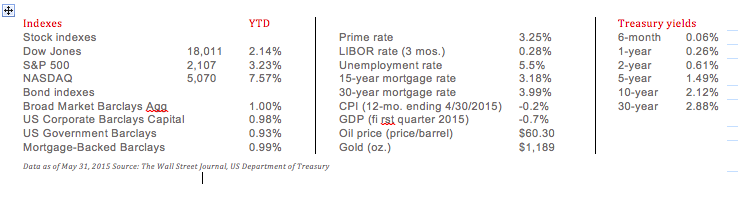

Source: The Wall Street Journal

Headlines

Source: The Wall Street Journal

Source: The Wall Street Journal

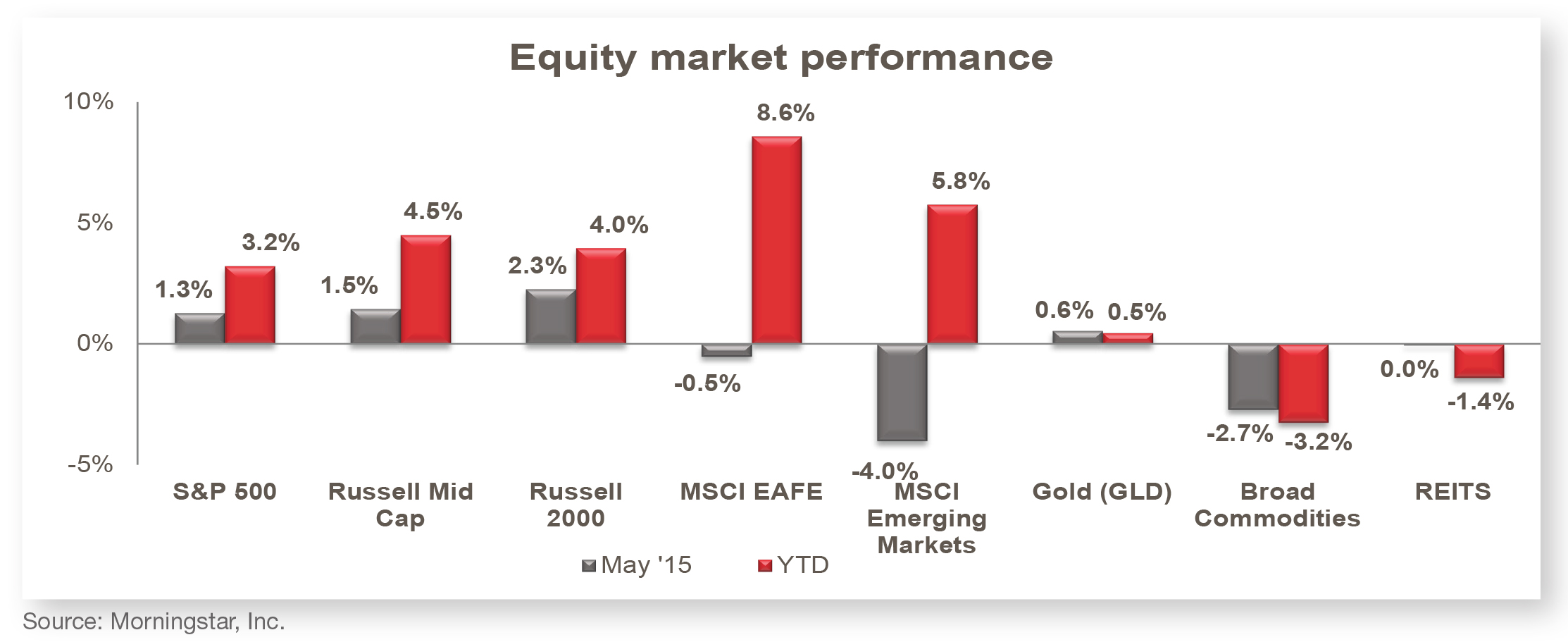

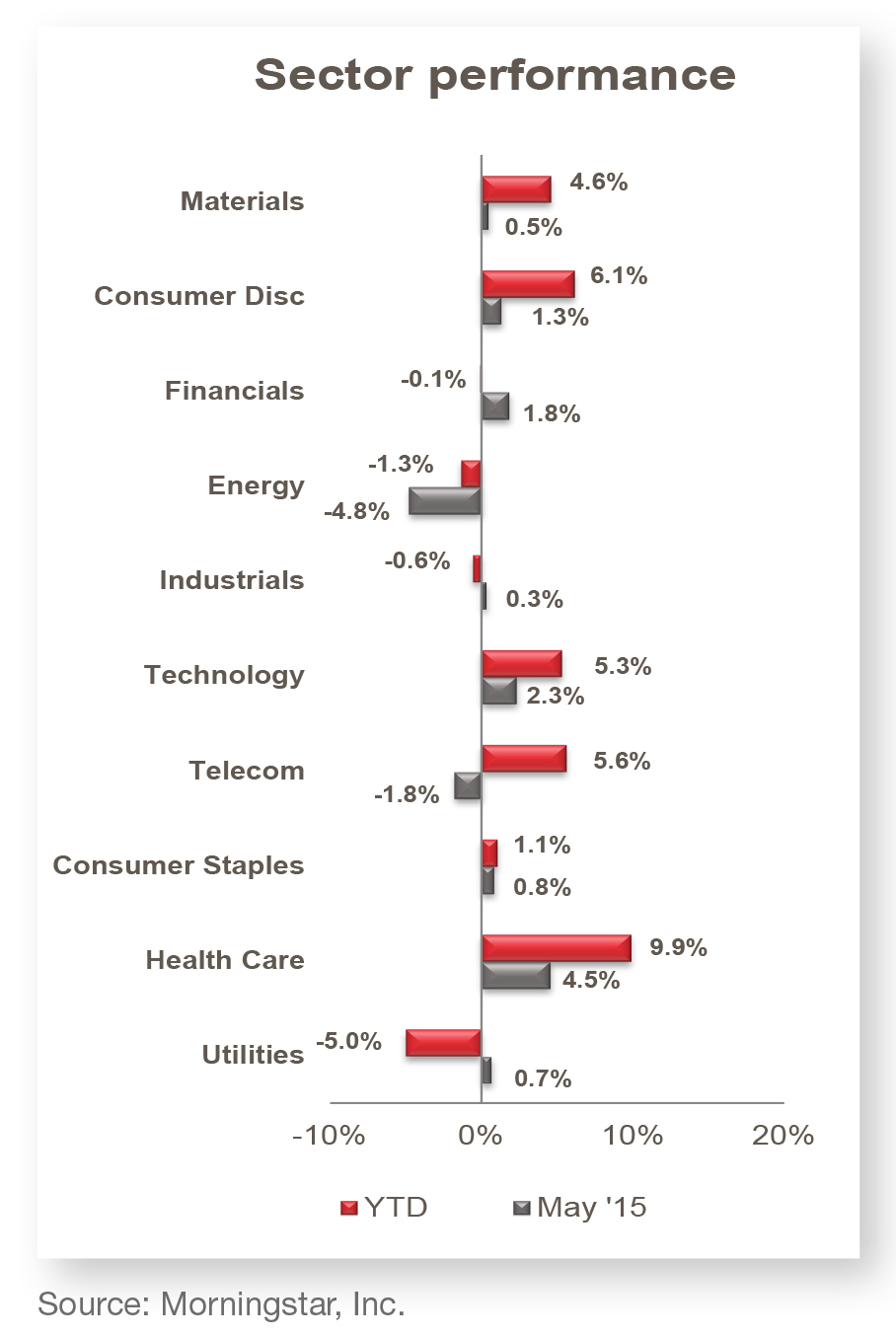

Equity Markets

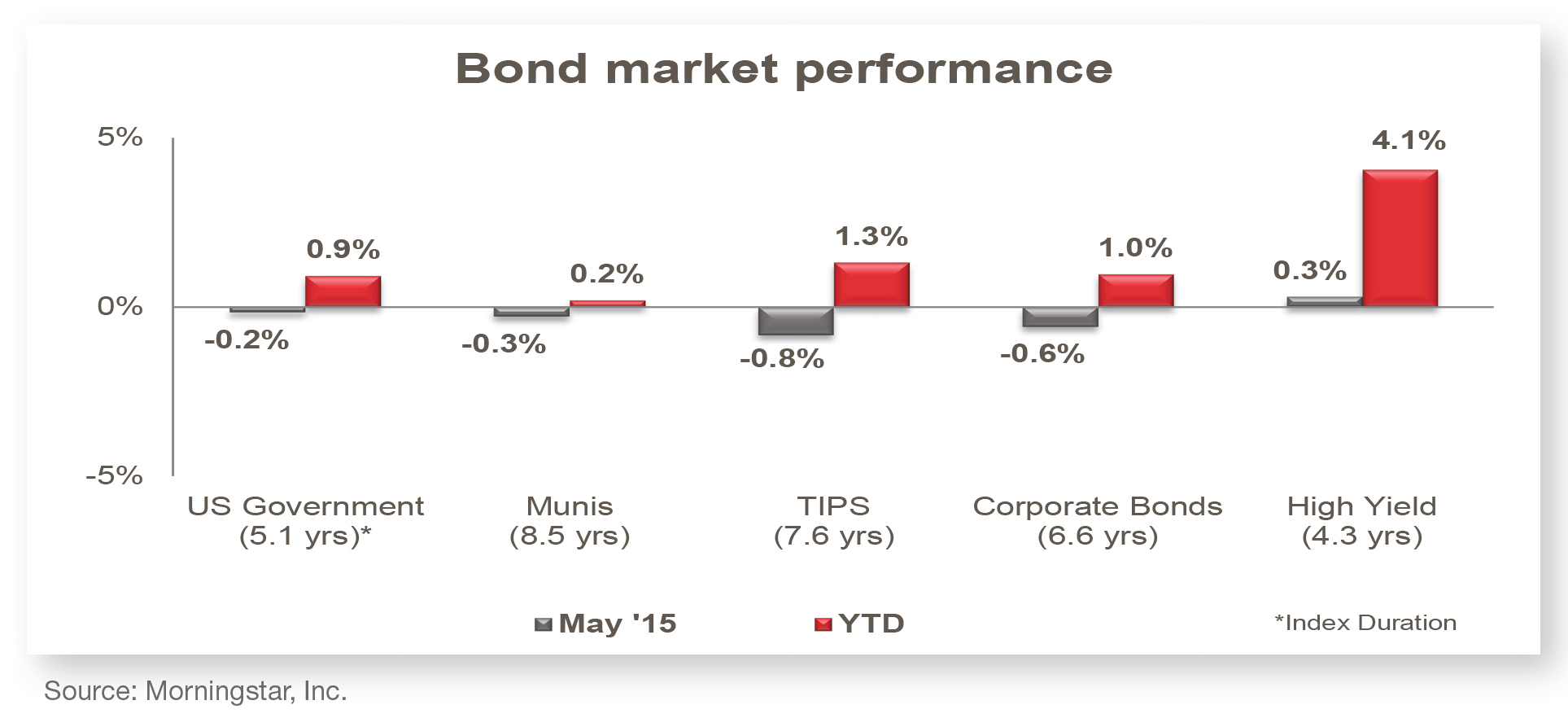

Source: Morningstar, Inc.

Source: Morningstar, Inc.

Source: Standard & Poor’s, MSCI, FactSet, JP Morgan Asset Management

International markets see less correlation in 2015, leaving room for fund managers to add value.

Foreign stocks fall back in May after strong start to the year.

Oil price rebound cools, challenging commodities investments and energy stocks.

Fixed income markets

Source: Morningstar, Inc.

Source: U.S. Department of Treasury

Source: EPFR Global, Tradeweb

Interest rates push higher, bonds continue sell-off in May.

European bonds see major swing in May after bottoming out in April.

Disclosure:

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2015 Bronfman E.L. Rothschild, LP