U.S. equities were up fractionally last week, with the S&P 500 Index up 0.1% as seven out of ten sectors traded higher.1 Strong retail sales figures kept the focus on the Federal Reserve and the prospect of higher interest rates. Concerns over Greece’s debt problems pushed volatility levels higher. The banking industry performed well, while cyclical areas of the market such as transportation lagged. 1

Weekly Top Themes

1. Improving retail sales bode well for future economic growth. Sales in May surged 1.2% and previous months’ figures were revised higher.2 After declining by a 4.0% quarter-over-quarter annualized rate in the first quarter, retail sales are now on track to increase 7.0% in the second quarter.2 Our view is this turnaround is being driven by the strong labor market and rising income. These trends suggest growth should accelerate in the second half of the year.

2. We are not expecting any interest rate decisions at this week’s Fed meeting. Given that economic growth appears to be improving, we think September’s meeting remains the most likely time for a rate increase liftoff.

3. There are hurdles, but we expect trade legislation to be passed. Both the House and Senate passed trade bills last week, but they still need to be reconciled before legislation can be signed by President Obama. Our best guess is that new Trade Promotion Authority will be enacted. Should legislation fail to pass, we think it would be a negative for economic growth and financial markets.

4. The Greek drama is likely to continue against a complicated political backdrop. Simply put, Greece has too much debt relative to its ability to repay it. If Greece were a company, it could declare bankruptcy and reorganize its debt. Similarly, the obvious solution would be for its creditors to restructure Greece’s debt in exchange for some much-needed reforms. Since decisions are being driven by political rather than economic motivations, however, a long-term solution remains elusive.

5. So far, 2015 has been a good year for active U.S. large cap equity managers. According to an analysis by Fundstrat Global Advisors, the majority of active managers are beating their benchmarks on a year-to-date basis, and 2015 marks the best pace of active management performance since 2009.3 This may be partially a result of climbing volatility, and we expect this outperformance trend to persist.

Rising Rates May Pressure Equities, but the Long-Term Outlook Remains Solid

The collapse in bond yields that dominated 2014 has been unwinding over the past month and in some cases the rise in yields has been quite rapid, especially in Europe. Although bond yields remain low by historic levels, the rate of change has been dramatic. This is causing many investors to wonder whether rising yields may put equity markets at risk.

If yields continue to rise at the same pace as the past several weeks, that could cause problems for equities. While European equities may be facing some risks, we think U.S. stocks should remain more resilient. U.S. bond yields have risen more modestly than they have in Europe, but a pending shift in Fed policy could trigger some sort of equity market consolidation, especially since equity valuations have become a bit stretched. As such, we think investors should expect continued turbulence over the coming months.

Nevertheless, we advocate keeping overweight positions in equities and suggest investors with long-term horizons should look past any near-term volatility. Economic growth appears to be improving, driven by a healthier consumer sector. We expect corporate earnings will follow suit in the second half of this year and would point out that the earnings picture is already brightening, outside of the energy sector. The Fed has made it clear that it does not want to derail the economic expansion and will move very slowly if and when it does shift its stance. Together, all of these factors should help equities push higher.

Beyond a few short-term problems that may coincide with Fed action, we think the prospects for equities are solid. We expect U.S. equity prices will be higher than where they are today on a six- and twelve-month time horizon.

1 Source: Morningstar Direct, as of 6/12/15

2 Source: Commerce Department

3 Source: Fundstrat Global Advisors

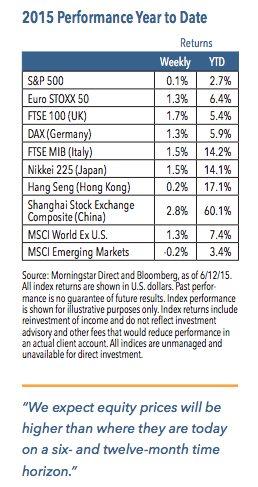

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.