Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

At least some large money managers have been seriously concerned about possible Greece implications for global asset dynamics. We briefly present one counterintuitive and contrarian point of view on possible Greece implications for Global Carry and possible hedges and tail-hedges based on recently emerged link of Global Carry and Dollar.

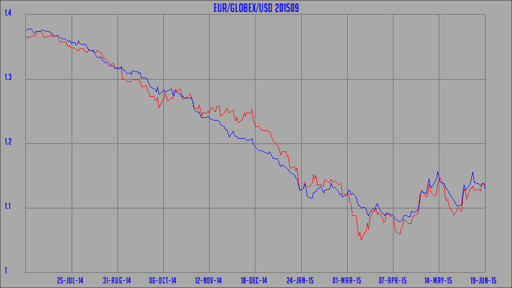

Below we depict Global Carry1 (with a minus sign) vs EUR/USD exchange rate:

There is no precise day-to-day co-movement here but there appears to be some undeniable link which we assume works though asset hedging.

What this also appears to imply is that weak dollar (strong euro) is the possible source of trouble for Global Carry, not the other way around, at least for now. How long this relationship would last we of course do not know.

What this also implies is that scenarios of Greece outcome where strong Euro is projected are the ones to be most afraid off. Also long Euro calls and deep otm Euro calls are possible cheap hedges.

This is quite counterintuitive as mildly strong Euro scenarios are actually base case scenarios with short term Q2 resolutions until the next debt rollover in coming years.

JPM outlines three scenarios:

(1) resolution in Q2 until the next rollover hump in coming years;

(2) intensification through Q2 then resolution in Q3 or Q4;

(3) intensification with a path towards EMU exit.

They have the following implication for EUR/USD pair:

- (1) Euro rises 2-3%;

- (2) Euro falls 2-3%;

- (3) Euro falls 10%.

So should US asset managers be afraid of Euro default or actually prompt resolution?

Fair Winds and Following Seas

1 Dynamika Commentary, “Global Macro Framework”, 11 March 2015