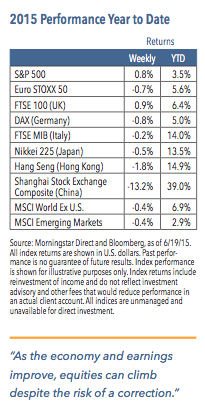

U.S. equities finished higher last week as the S&P 500 increased 0.8%, recording its highest weekly gain since April.1 The dovish message from Wednesday’s FOMC announcement boosted markets. Contagion from Greece appears relatively contained. The sell-off in equities in China did not impact global markets. The health care, consumer staples and utilities sectors rallied. Financials lagged as banking lost momentum and energy underperformed.

Key Points

▪ Leading global economic indicators point to improving signs for growth.

▪ Fed monetary policy decisions remain deliberate and measured.

▪ Corporate profit expectations should gradually strengthen later this year, which should be positive for equities.

Weekly Top Themes

-

The FOMC statement acknowledged several improvements, most notably in labor markets. Consumer spending and housing were also cited as favorable trends. In spite of positive signs, a lingering weakness exists in business fixed investment and exports.2 Projections suggest the Committee continues to debate whether to hike rates once or twice in 2015. In our view, September remains the most likely timeframe for a rate increase liftoff.

-

The struggles in Greece should continue for some time. Greece will likely have issues paying its debts and may engage in ongoing back and forth with creditors. The country will focus on securing a solid deal with the intention of remaining part of the eurozone.

-

A cyclical bounce may be emerging. Recent stronger cyclical reports began with April’s housing data in mid-May.3 According to ISI, 87% of cyclical indicators have been positive since then. Unemployment claims and updates to the Philadelphia Fed Survey support a bounce. The leading economic indicators rose 0.7% in May and suggest healthy growth over the next six to nine months.4

-

The U.S. consumer is key to improved U.S. economic growth and earnings. U.S. consumer spending is being supported by solid employment growth, slow but accelerating wage gains, increases in consumer net worth and rising expectations that real income will improve.5

-

Consumer inflation expectations and actual prices are accelerating slowly. So far this year, core inflation as measured by Consumer Price Index (CPI-U) is climbing at nearly a 2.5% annual rate.6 This is almost enough to move the core Personal Consumption Expenditures (PCE) deflator up to 2.0%,6 which is the key measure for the Federal Reserve.

An Earnings Rebound Could Benefit Equities, Despite Risks

U.S. equities have been resilient while the underlying bull market remains intact. The unwinding of last year’s deflation trade has caused bond yields to spike higher in recent months, which has spurred a rotation from bond-like investments, such as utilities, into financials. The looming start of the Fed rate cycle represents a potential bump in the equity market advance, but the current risk-reward potential supports remaining invested rather than standing aside. Fed policy should remain accommodative even as rates start to rise. Improvement in the economy and earnings growth imply that equities can continue to climb despite the risk of a correction. A Greek default or exit from the Economic and Monetary Union

pose a threat for equities because of the potential for significant contagion, especially in the euro area. We anticipate that Greece’s debts will be rolled over and its membership maintained, thus avoiding a meaningful disruption to capital markets.

Global earnings slumped in the second half of last year but are beginning to rebound and should continue to recover as economic growth improves. The deterioration in earnings reflected the dramatic decline in the energy sector due to falling oil prices, residual weakness in the euro area and emerging markets, weak overall growth in the United States and the surge in the U.S. dollar. Looking ahead, the earnings picture should brighten as those headwinds fade. Forward earnings estimates were downgraded sharply, led by the drop in energy, but profit expectations should gradually strengthen later this year. Earnings for non-energy companies should begin to reflect stimulus from lower oil prices and an ongoing economic recovery. Although equities are not inexpensive in relative terms, we expect earnings will improve and monetary policy will stay reflationary, which should preclude material risks.

1 Source:MorningstarDirect,asof6/21/15

2 Source:FederalReserve

3 Source:CensusBureau

4 Source:TheConferenceBoard

5 Source:BureauofLaborStatisticsandBureauofEconomic Analysis

6 Source:BureauofLaborStatistics

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.