Weighing the Week Ahead: What Does the Greek Crisis Mean for Financial Markets?

The calendar shows a fair amount of economic data in the coming week, but attention is likely to be focused abroad. After many years (some would say decades) of percolating, the issue of Greece and the Eurozone is coming to a conclusion. I expect this week’s theme to be:

What does the Greek crisis mean for financial markets?

Prior Theme Recap

In my last WTWA I predicted that market participants would be focused on the Fed, wondering if they had heard the message from the markets. Some readers commented that Greece was likely to take center stage. They were right at the start of the week, and also at the end when even the most voluble pundits were running out of comments about a predictable Fed meeting. Doug Short’s excellent five-day summary always captures the story in one great chart.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

The Greece story has been high on the list of worries for several years. Some observers suggest that the underlying problems are better measured in decades.

This week features a solid data calendar, but nothing really dominates. The Greek story is both timely and compelling, with the market effects uncertain. It is a perfect paradise for pundits. I expect market observers to be asking:

What does the Greek Crisis mean for financial markets?

The Viewpoints

There are several basic viewpoints, ranging from best to worst as follows:

- An agreement will be reached at the last possible moment. (A case from the Greek perspective. I rarely cite anonymous posts, but this group of Amsterdam professors have been informative on this document, with well-documented analysis).

- A Greek settlement will encourage other European nations to seek concessions.

- Greece will default on some payments, but the impact will be quite limited. A new Greek currency will emerge and there will be no “contagion.” (Barry Ritholtz)

- Greece will default, leading to a run on banks. (ft.com)

- A Greek default spills over to European banks and other sovereign debt. This weighs seriously on the nascent European economic rebound. (ft.com)

Variations on these themes are possible. Here is a great calendar of the key dates, beginning on Monday. And continuing in-depth coverage from ft.com – a great way to keep up with events.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was plenty of good economic news.

- Initial Jobless claims were only 267K. Here is the look from Bespoke:

- Building permits are now at the highest pace since 2007. Some of this is multi-family building, but from an economic perspective that is OK.

- Core CPI is well-contained. I am mystified by those who regard this as bad news. While the Fed is not hitting its inflation “target” we should be happy to see restrained inflation in the context of better economic growth. CPI per se is not a growth measure.

-

The Fed satisfied the markets. It might not have been a surprise. There were plenty of critics. Despite this, the continuing assurance that the path of rate hikes will be gradual is the key takeaway. Tim Duy, the leading Fed observer, summarized the meeting as follows:

-

Bottom Line: Fed policy unchanged as expected, door still open for a rate hike in September, but the lower rate path indicates a modestly more dovish Fed resigned to a persistent low interest rate environment. It’s the rate path we need to be watching, not the timing of the first hike.

- Leading indicators once again surprised with a gain of 0.7% versus expectations of 0.4%. Steven Hansen at GEI has a complete analysis and critique, including this chart:

- Investor sentiment has turned negative. This is a contrarian indicator, so it is good news. Ryan Detrick analyzes several different indicators and notes the protests from those who previously embraced the same measures. If you are going to be fair about an indicator, you need to accept the result when it changes direction. So many sources trumpet this when bulls seem to be “all in “and then fall silent when it changes.

The Bad

There was also some negative data last week, partly on the policy front.

- Trade legislation is still mired in Congress. The political lines are shifting, but the fate is uncertain. As I have consistently noted, opinions may vary about worker protection, but this legislation meets our “market-friendly” test. (The Hill)

- A new government shutdown looming? Here is the early read. (The Hill).

- Putin. Playing a nuclear card? The contemplated additions to inventory are small, and within the existing agreements, but why? (Brookings).

- Industrial production declined by 0.2%.

- Housing starts registered a big decline. This was mixed news, given the revisions and the prior month gains. Calculated Risk actually called it a “decent report” although the headline number was certainly disappointing.

The Ugly

Charleston. So bad, so sad, in so many different ways, overshadowing other issues. I expect the story to dominate the Sunday news shows while everyone tries to sort out the implications.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes to Pierre Lapointe, who takes on the crowd that has been worrying about profit margins. (Via BI) This concern has been expensive for many investors. This chart summarizes the argument that it can take many years for declining margins to impact stock prices.

Noteworthy

This is an amazing list, particularly when we note that they are business passwords. Even the relatively modern requirement to include some numbers and symbols cannot slow down the creatively lazy! (Statista via GEI)

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators. He recently noted an increase in his combined measure of economic stress, although the levels are still not yet worrisome.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator (featured below). Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (3½ years after their recession call), you should be reading this carefully. Recently the ECRI finally admitted to the error in their forecast, but still claims the best overall record. This is simply not true. I rejected their approach in real time during 2011 and also highlighted competing methods that were stronger. Until we know what is inside the black box (I suspect excessive reliance on commodity prices and insistence on unrevised data) we will be unable to evaluate their approach. Doug is more sympathetic in his last update. While I disagree, it will require a longer post to elaborate.

In this week’s update Doug notes the ECRI claim of lower growth and more frequent recessions. The two do not necessarily coincide. Recessions do not generally begin with “stalls” but rather with business cycle peaks. Some readers have suggested that I retire this line of discussion from WTWA. I would happily do so if more media sources did a better job with the recession discussion. Until then it provides an important reminder.

Doug’s Big Four summary of key indicators watched by the NBER in recession dating shows no evidence of a business cycle peak. Only industrial production shows some weakness.

Some economic activity is not effectively measured. Economic growth is under-estimated as a result. Here are some ideas for estimating the effect, starting with examining the differences between spending and income. I suspect that all of us have contributed some cash to the underground economy….

The Week Ahead

We have a modest week for new data.

The “A List” includes the following:

- New home sales (T). An important read on an important sector.

- Durable goods (T). Volatile May data, but important for a good read on GDP.

- Personal Income and spending (Th). Key read on overall economic strength.

- Michigan sentiment (F). Great concurrent indicator on spending and employment, with some leading character.

- PCE prices (Th). This is the Fed’s favorite inflation indicator, with less emphasis on housing. Well worth watching!

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

The “B List” includes the following:

- Existing home sales (M). Less important than new sales (above) but still an interesting read on the sector.

- FHFA home prices (T). Covering a wide range of homes, but not followed as widely as other measures.

- GDP Q1 third estimate (W). Old news, but it provides a baseline.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

There is a smidgen of FedSpeak, but it is not very important this week. Anything about Greece will command attention.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

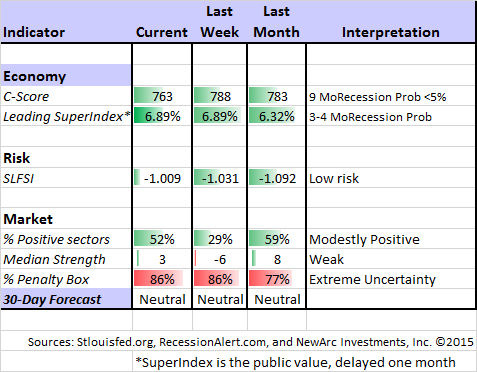

Felix continued a neutral stance for the three-week market forecast. The confidence in the forecast is very low with the continuing extremely high percentage of sectors in the penalty box. Despite the overall market verdict Felix has generally been fully invested in three top sectors, including some foreign exposure.

While trading is not gambling, there are some valid lessons. Trade Ciety consults a top gambler and identifies some common amateur mistakes. Have you ever engaged in “revenge trading?”

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important post, it would be this assessment of market prospects by Jeff Reeves. He is bullish on the summer prospects for stocks, mostly because of errors in a list of nine popular worries that have weighed on the market. I especially like this one:

9. A market correction is not ‘due': Perhaps the most important data point of all for the bears to remember is that rallies do not end simply because they’ve gone on for a few years and are “due” to correct. Consider the bull market of 1987 to 2000, which lasted 4,494 days and saw a roughly 585% increase in the S&P 500 SPX, -0.53% I would never discourage investors from thinking critically or skeptically about the numbers, and it’s human nature to wonder when the party is going to end. But predicting the end just because we’ve had a long runup, especially in the face of this encouraging data? That’s just self-defeating.

Stock Ideas

Barron’s has a cover story on airlines, suggesting that some could rise by 50% in the coming year. The basic argument is that expansion of capacity has been controlled and RASM (revenue per available seat mile) strong. While several of the big names are cheap, their favorite is American.

Brian Gilmartin provides a great lesson in how to use cash flow to compare dividend stocks. Merck Vs. Pfizer: From A Dividend And Free-Cash-Flow Perspective analyzes two popular stocks, provides ideas about the sector, and helps investors to learn a key element of stock picking.

The six best sectors for the rest of the year. Mark Hulbert makes the case for manufacturing and finance. Good here!

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. I especially liked this WSJ link about emotions and investing – a topic at the top of the list in conferences with new clients.

Energy

Is Exxon Mobil the best dividend stock? Tim McAleenan Jr. makes an interesting case with a good list of reasons, including noting “all weather flexibility” as the company makes profits in a tough environment.

Thinking about Bonds

Watch out for bond ETFs that sound good, but have a high bid-ask spread. The most liquid ETFs are fine, but some spreads are in the 0.8% range writes Chris Dieterich in Barron’s.http://online.barrons.com/articles/the-hidden-costs-of-bond-etfs-1434759831?tesla=y&mod=djemb_mag_h

Market Outlook

Has there been a “sideways correction?” (Ben Levisohn in the popular Barron’s Streetwise column).

In fact, stocks have performed quite well after a quiet start to the year. Paul Hickey of Bespoke Investment Group, looked at the 10 years during which the S&P 500 stayed closest to where it had started during the first 117 trading days. He found that it had risen 6.6%, on average, in the rest of those 10 years. Says Hickey: “A sideways market can be a correction in time, not price. Expect things to drift higher from here.”

Final Thought

This section is where I share my own conclusion. I try to add some insight to the evidence. Last week there was some discussion, starting with a complaint from a reader (who obviously had only recently tuned it) that I did not offer specific advice. I hope that the regular audience for WTWA knows that the series is designed with several objectives:

- Identify the most important issues

- Focus attention on those most relevant for the week ahead

- Provide interesting arguments for various perspectives

- Explain how your analysis might differ depending upon your time frame

- Share my own conclusions, often different for traders and investors — -and I have programs doing both!

Anyone expecting a one-size-fits-all, spoon-fed approach has come to the wrong place!

How does this apply to Greece? The Greek crisis is a good example of a type of market risk. It is an example of something viewed as a binary outcome with a known and certain date for the conclusion. The framework for analysis includes three topics:

- The probability of each outcome.

- The likely consequences of each outcome.

- Market expectations (what is already reflected in market prices).

There is always the chance that the deadline will somehow be extended. Outcomes may also be less binary than they seem. The negotiating parties frequently find creative avenues for compromise as well as delay.

With that background, here is how I am using the framework to think about this risk. My conclusions are based upon a wide variety of sources. In WTWA I do not make an argument for my own viewpoint, but I usually share it.

- I rate the chance of a default as quite high. The Greek leadership, encouraged by its constituency, seems unwilling to make concessions. European leaders seem to have reached their limit. Reports from those close to the negotiations have not been encouraging.

- I expect the ultimate consequences to be limited, but only after a period of uncertainty. While contagion is unlikely, markets hate uncertainty.

- It is always difficult to know what is reflected in current market prices. My conclusion is based upon nearly thirty years of observation of daily trading. My sense is that the Greece effect has (so far) been pretty minor. Most market participants have been trained to expect an eleventh-hour resolution. (Dr. Brett).

The average investor should not over-react to this, going “all out” of the market for a temporary effect. A trader might try to capture the reaction. We did a little of this in our accounts.

As always, the right trade depends upon your time frame and your agility.