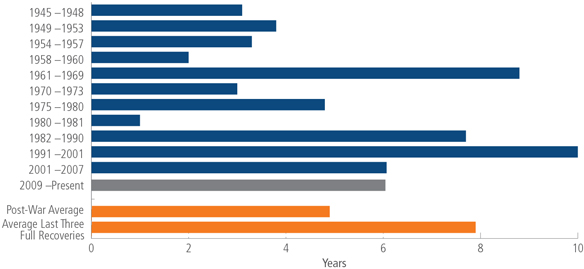

When it comes to the duration of the business cycle, 50 is the new 40. Much the way that better diet, health care and exercise have helped double life expectancy over the past century, central banks have prolonged the current expansion using new elixirs such as zero interest rates and quantitative easing. At 72 months, the business cycle has well surpassed the 58.4-month average of the modern era and is now more than twice the length of the pre-WWII average.1

When the Asset Allocation Committee met recently to update our views for the coming 12 months, we concluded that this “generational extension” of the business cycle is likely to sustain an environment in which investors are compensated for holding riskier assets–at least while this cycle continues.

Three rounds of quantitative easing in the U.S. and similar asset repurchase programs in other developed economies have given the expansion a second life. But these programs may have side effects that are creating challenges for investors. Longer-term return outlooks for traditional assets have moderated and will likely remain challenged. Microbursts of volatility are roiling different corners of the capital markets. Some assets are being treated like hot potatoes and held for only brief periods of time.

Still, investors have learned not to fight central banks. This age-old mantra is now being extended to the European Central Bank and the Bank of Japan amid evidence that their policies are starting to stoke growth. Even the People’s Bank of China is pursuing aggressive monetary stimulus to stabilize growth in the world’s second largest economy. Barring some shock to the system, we believe monetary policy support is likely to prolong the cycle and, by extension, should continue to make risk assets more attractive from a risk-return standpoint than less risky assets. In light of this, the Committee members’ views were largely consistent with those expressed last quarter, with a couple of notable exceptions.

Six Years and Counting: The Current Business Cycle Could Prove Lengthy by Post-War Standards

Post-War U.S. Business Cycle Recovery Durations

Source: The National Bureau of Economic Research. As of May 31, 2015. Contractions (recessions) start at the peak of a business cycle and end at the trough. Expansion (recoveries) start at the trough of a business cycle and end at the peak.

Overall Bias toward Risk Assets Maintained

We continue to prefer global stocks over global bonds at this point in the business cycle. No major central bank has begun to raise rates yet, margins are expanding at a healthy clip, inflation remains benign and recent economic data suggest better growth prospects ahead. Many market observers believe stock and bond valuations are stretched, but past tightening episodes have demonstrated the attractive upside potential of risk assets even when rates start to normalize. Within bonds, we prefer credit over core developed market sovereign debt on expectations that defaults will remain low and that rock-bottom (even negative) core sovereign bond yields may encourage investors to explore riskier options.

Move to Neutral on U.S. Large Cap Equities

The Committee moved to neutral on U.S. large cap equities as multinationals face headwinds from a stronger dollar and tepid growth overseas. We believe the current macroeconomic environment favors smaller companies in the U.S. as they benefit more from falling unemployment and the potential for rising wages and consumer spending. More broadly, we continue to prefer developed markets over emerging markets as monetary policy in Europe and economic reforms in Japan are producing results and overshadowing concerns related to structural challenges. We remain neutral on emerging markets equities where many countries are being challenged by low commodity prices and weak demand for manufactured exports. We continue to view China and India favorably, but acknowledge that their markets have both risen dramatically in the last 12 months and their respective governments face important hurdles to continue their pro-growth reform processes.

Investment Grade Fixed Income Upgraded

The Committee is now slightly more positive on investment grade fixed income as yields have risen modestly in the short term, corporate balance sheets are strong, fundamentals remain sound and maturities have generally been pushed off in the distance. As a result, we believe investors are being adequately compensated for owning investment grade credit relative to very low yields available in sovereign safe assets. That same logic applies to high yield fixed income and hard currency emerging markets debt, which remain our two standouts in fixed income. High yield’s ability to shake off the energy-related challenges of last year was impressive, and we believe default rates are likely to remain low. Likewise, emerging markets seem to be stabilizing, making their attractive yields worth the associated risk.

Attractive Opportunities in Alternatives

Finally, in markets where traditional assets are not offering the potential for attractive absolute returns, we believe hedged and private market strategies may offer more appealing opportunities.

Lower volatility hedge funds, which have performed well so far this year, remain our preference among real and alternative assets, given our attractive return outlook for them in an environment of rising interest rates. Despite stabilization in crude oil prices, we don’t believe commodities stand to rally much from here.

Risks to the Outlook

The Committee continues to view a negative shock on the growth side as the key risk to the outlook. Business cycles never just peter out: Every downturn since 1980 has been preceded by a major financial event. Absent something unforeseen, though, we believe this expansion has room to run, and any pick-up in inflation will be viewed by central banks and even many investors as a positive.

When this business cycle’s time is up, we may well learn that longer term trends—such as lower productivity growth, globalization and structural inefficiencies—portend a permanent shift to a low-growth, low-inflation global economy. But in the interim, our asset allocation outlook will continue to be tethered to the view that the expansion isn’t so much on borrowed time as it is enjoying the benefits of extended health.

About the Asset Allocation Committee

Neuberger Berman’s Asset Allocation Committee meets every quarter to poll its members on their outlook for the next 12 months on each of the asset classes noted. The panel covers the gamut of investments and markets, bringing together diverse industry knowledge, with an average of 24 years of experience.