Weighing the Week Ahead: Will FedSpeak Interrupt the Lazy, Hazy, Crazy Days of Summer?

In one sense, the week ahead should be a quiet, dull semi-vacation. As Nat King Cole explained, the Lazy-Hazy-Crazy days of summer – pretzels, beer, and bikinis that never got wet.

It is the lull before earnings and includes a light economic calendar. Will the A-Team need to return from the beach because of Greece? Or will it be a quiet week, disturbed only by an avalanche of FedSpeak and consequent punditry?

One way or another, I think we will (finally) put the Greek drama behind us and resume the familiar debate about the Fed.

I expect the pundits to be interrupting our summer with discussions of the FOMC minutes and the record number of Fed speeches.

Will FedSpeak Upset a Quiet Market?

Prior Theme Recap

In my last WTWA I predicted that market participants would concentrate on Greece at the start of the week and then turn to economic reports. This was mostly correct. The Greek story lingered, but the biggest impact was on Monday. The economic news was supportive for most of the week, but the employment report was more of a dud than a firecracker.

Meanwhile we have to deal with Greece again this week. As usual, Doug Short’s excellent five-day summary captures the story in one great chart. Read the full article for more charts and discussion.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

Trying to predict this week’s theme is a real crapshoot. With the Greek referendum on Sunday, and polls showing a tossup, the market story will take one of two quite different courses. By the time you are reading this, the result will be known.

In the absence of that knowledge, I will make some educated guesses. If the referendum passes, it will have a calming influence on markets and a big bounce. If it fails on a close vote, there will still be plenty of pressure for a negotiated solution. In either case, I expect the story to lose traction during the week ahead.

While we have the official start of earnings season with the Alcoa report, that theme will command more attention next week.

As a result, the field will be open for those pundits who are not on vacation to speculate and pontificate. Wednesday’s FOMC minutes will provide fresh information on a favorite topic. In addition we have speeches by at least seven (is this a record?) different Fed Participants in the last three days of the week, including Chair Yellen. That will provide plenty to talk about.

Will FedSpeak Upset a Quiet Market?

The Viewpoints

The media time and space must be filled, but do not expect anything fresh.

Jeff Gundlach says to ignore the bond pundits, especially those on CNBC.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was plenty of good economic news.

- Private employment gains beat expectations according to ADP, which deserves consideration as a strong and different approach from that used by the BLS. Calculated Risk has the story, including Mark Zandi’s observation that the pace of growth is twice that needed to absorb new workers.

- Improving home prices are sustainable according to CoreLogic’s Mark Liu (via Econintersect). Check out the story for the full analysis and also the list of overheated markets.

- ISM manufacturing remained solid and slightly beat expectations.

- Earnings are looking good. Brian Gilmartin’s astute and entertaining update suggests that we expect growth of 6-7%. (Channeling Robert DiNiro?)

- Construction spending growth improved. Steven Hansen at Economic Intersect has the full story, past data, and charts with NSA data. He notes that revisions were also positive.

- Personal income and spending strengthened. “Betting against the US consumer is usually a bad bet” – Ed Yardeni.

The Bad

There was also some negative data last week, partly on the policy front.

- No progress on Greece. Julian Robertson is not worried about a Grexit, but he will keep his eye on Spain. Cullen Roche has multiple reasons to keep your worries contained, including that the total debt is 30 hours of Walmart’s revenue.

- Initial jobless claims rose. The 281K report also moved up the widely-followed four-week moving average. Doug Short has the full story and several helpful charts.

- Employment report. I am scoring this as “bad” despite the mixed nature of the report. Growth in payroll jobs was not bad, and there is expansion in full-time jobs. Labor force participation declined. Wages are not growing. Diane Swonk calls the story one of a “glass half full” noting the lack of growth in construction and also considering the implications for Fed policy. Dissent? Rex Nutting argues that wages are going up if you measure via median income. Scott Grannis, who dependably finds the bright side, calls it “average“.

The Ugly

Puerto Rico. I do not consider this a “domino” in a chain including Greece, but there are many parallels. Did you know that people in San Juan do not have fresh water for a 48-hour period every three days? That any products must be imported on US flag ships, keeping the cost of living at NYC levels while per capita income is only $24,000, two thirds of the poorest state in the U.S.

Read Felix Salmon’s powerful discussion of “America’s very own Greece.”

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes to Jordan Ellenberg, a math prof at one of my old schools, the University of Wisconsin-Madison. His WSJ articleprovides a number of entertaining and enlightening examples of misleading uses of data. I enjoyed his conclusion:

All these mistakes have one thing in common: They don’t involve any actual falsehoods. Still, despite their literal truth, they manage to mislead. It is as if you said, “Geraldo Rivera has been married twice.” Yes—but this statistic leaves out 60% of his wives.

In the era of data journalism, truth is not enough. We need people in the newsroom who can check not only a number’s value but also its meaning. Unless we can ensure that, we’re going to be reading a lot of data-driven stories that are true in every particular—but still wrong.

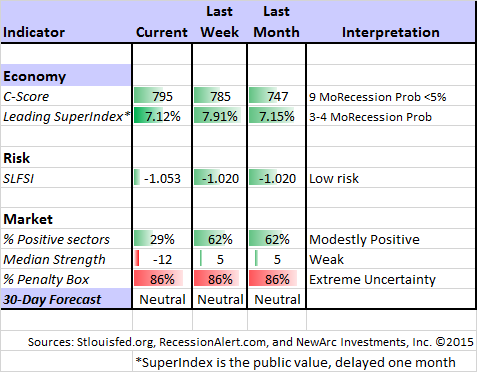

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (3½ years after their recession call), you should be reading this carefully. Recently the ECRI finally admitted to the error in their forecast, but still claims the best overall record. This is simply not true. I rejected their approach in real time during 2011 and also highlighted competing methods that were stronger. Until we know what is inside the black box (I suspect excessive reliance on commodity prices and insistence on unrevised data) we will be unable to evaluate their approach. Doug is more sympathetic in his last update. While I disagree, it will require a longer post to elaborate.

The best concurrent economic pulse comes from Doug’s Big Four summary of key indicators, those watched by the NBER’s recession dating committee. There is no evidence of a business cycle peak.

Michael Harris at the Price Action Lab Blog debunks the power of the 200-day moving average. You can make your own call about whether the improvement in drawdown is worth the reduced performance versus buy-and-hold over the twelve years tracked. He has a compelling argument that 200 days is “sub-optimal” and shows the 100 day MA as an example.

The Week Ahead

This is a relatively light week for economic data.

The “A List” includes the following:

- ISM Services (M). Less history than manufacturing data, but a larger economic sector.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- FOMC Minutes (W). Will be parsed carefully for any hints of rate-hike timing.

The “B List” includes the following:

- JOLTS Report (T). Still misunderstood by most, the Fed uses this for insight into employment structural issues.

- Trade Balance (T). May data, relevant to Q2 GDP.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

- Wholesale Inventories (F). May data relevant to GDP.

Anything fresh about Greece will command attention.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix continued a neutral stance for the three-week market forecast. The confidence in the forecast remains very low with the continuing extremely high percentage of sectors in the penalty box. Despite the overall market verdict Felix has generally been fully invested in three top sectors.

Traders should always check out Brett Steenbarger’s site. This week he explains the need to take risks.

- Resilience – Successful traders take risk. Successful traders are sometimes wrong. Successful traders take hits. Successful traders learn from the hits, get up, and move on. They are resilient. They succeed, as Churchill observes, by moving from failure to failure with enthusiasm.

It reminded me of my first days in the business. My boss wanted me to play in the local high-stakes rubber bridge game. I pointed out that he knew my salary, and it was more than I could afford. He explained, “That is the point. You will be making many big decisions. I don’t want you thinking about the dollars – just the risk and reward.”

The next day he asked how I did. I replied that I had won $165 (not bad in those days). “Too bad,” he replied.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking. Please also check out part one of my new series on risk. Early reactions were good, and more comments are welcome. At least three more installments are planned.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important post, it would be an excellent article by Robert Huebscher, Founder and CEO of Advisor Perspectives. He often takes an important topic and gives it his own analysis. This source is widely followed by professionals, but not as well known among individual investors.

This week Robert analyzes the current stance of David Rosenberg, as described at the recent Mauldin Conference. While I have often disagreed with Rosenberg in the past, I congratulate him on his willingness to change his conclusions with the evidence. We should all respect this. In particular, he sees the market as too negative on the economy and on stocks. He emphasizes that the current business cycle could last for a long time – maybe two or three more years. He emphasizes the importance of recessions.

Giving the same answer to a question that WTWA readers already know from Bob Dieli’s commentary, he had this to say about the US getting dragged into a recession:

The U.S. was never brought into a recession by another country, Rosenberg said, in response to a question about whether weakness in China could halt the recovery. China has an output gap and is rebalancing, he said. But consumer spending there is growing, and he predicted that “a new bull market on consumer services” will unfold in China. Although the commodity boom is over, Rosenberg said, China can slow down and it will not have a deleterious impact on the US.

And this about bonds…

Despite the supply-demand dynamics in the Treasury market, Rosenberg doesn’t recommend that investors hold any bonds, unless one has a “proven view of deflation.”

But deflation is unlikely, he said. Core inflation is running close to 2% and is “more than meets the eye.” Inflation will be in our future, he said, but not in the next 12-24 months. “The central banks will ultimately get what they want,” he predicted, at which point a hard-asset cycle will be upon us.

Bonds are for speculators, he said, not for income.

According to Rosenberg, for 10-year Treasury to generate a 14% return (what the S&P returned in 2014), it would have to go to 50 basis points.

The review covers a list of all of the points that are currently most important for investors. There are also some good stock suggestions.

Stock Ideas

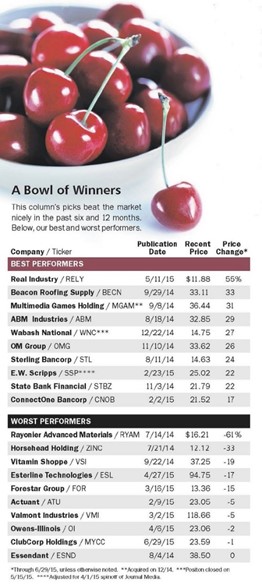

Biotech has been a great source of profits in a flat year for the market. In our “High Octane” stock program we seek out stocks with exceptional potential and we accept a higher level of volatility. Biotech is an important theme, and the Medical Technology Stock Letter is a source we follow closely. It has helped us into some big winners, including Novavax, Inc. (NVAX), which I wrote about in November. Thanks to John McCamant for giving us permission to share this name and also Ziopharm Oncology (ZIOP).

NVAX will be announcing results on several trials during the third quarter, including data showing that it is safe to immunize pregnant women. John believes that some are waiting to buy until they see the data, and the risk is already reflected in the stock price.

ZIOP popped recently on the news of the collaboration between CELG and JUNO. It remains below John’s buy price.

Small Cap Stocks also provided opportunity in 2015. Barron’s David Englander, who writes Sizing Up Small-Caps, provides some good general investment advice and a review of his ideas. Read the column for the full story, including this statement of philosophy and the report card for 2015.

We don’t worry about stock-market forecasts, or small-cap stocks as a group, or about the performance of small-cap exchange-traded funds. Nor do we care about “golden cross” or “death cross” patterns or other tools of technical analysis. It’s really pretty simple: We examine businesses and try to figure out whether they are undervalued by investors.

Greece? Sticking with the theme of aggressive picks, how about Greece? While the Greek stock market has been closed, the US-based ETF (GREK) has been trading. This is not for the faint-of-heart, but it might be worth a look. Here is the rationale for “spectacular gains.”

Disagreement? Harley-Davidson (HOG) is a comeback pick in this week’s Barron’s. I am waiting for comments from Scott Rothbort at Scutify, who made a timely exit in March.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. I especially liked this story about baby boomers and retirement.

Chuck Carnevale continues his series on past stock picks and how they worked out. You can learn a lot by looking over his shoulder and also find some excellent ideas. He notes the lack of accountability in most pundit advice, particularly those who speak in generalities. We never buy a stock without first checking it out using Chuck’s fine tools.

Economic Outlook

The economic outlook remains good and is improving over the next two years according to the Chicago Fed’s annual Automotive Outlook Symposium. This group of 75 economists and analysts were pretty good last year – better than the Fed and other surveys. Interesting reading.

Final Thought

You cannot think about the week ahead without considering Greece. I have written about this topic for several weeks, so this is just a summary.

-

In the intermediate term, this will not matter to US equity investors.

- The overall size and the impact on banks is modest.

- The pain of this process does not make it attractive for other European countries – no dominoes.

- The trends in the US economy have been positive, but erratic. We follow this closely on WTWA, trying to separate the noise.

- There is little threat of a US recession, despite some weakness abroad.

- Economic cycles and bull markets do not die of old age.

The quarter ended with a lot of knee-jerk “risk off” mentality. The investor dichotomy remains:

- Bonds and bond substitutes are not safe assets – they are risky.

- Stocks that benefit from rising long-term rates and a strengthening economy (banks, technology, industrials, and consumer discretionary) remain attractive.

- Whatever your “normal” allocation of stocks and bonds, it is a time to maintain or favor stocks.

And finally, this is an important time – the next two or three years. If you do not understand this and need help, I am available for a consultation at no cost. (email main at newarc dot com).