KEY TAKEAWAYS

Our view remains that the Fed is on track to hike rates for the first time in this cycle in late 2015.

The longer the uncertainty around Greece lingers, the greater the odds that the Fed doesn’t hike rates until early 2016.

A decisive upturn in wage inflation remains key to moving inflation and inflation expectations higher.

The “no” vote in the Greek referendum on July 5, 2015, will potentially raise the level of economic and financial market volatility in the coming weeks as global investors assess the market and economic risks associated with an increasingly likely Greek exit (Grexit) from the Eurozone and from the Eurozone’s common currency, the euro. We don’t view the potential Grexit as another “Lehman moment”; there is relatively little in the way of derivatives tied to Greek debt, and the vast majority of Greece’s debt itself is owned by supranational entities like the European Central Bank (ECB) and the International Monetary Fund (IMF), and not — as was the case with Lehman — by private investors. However, the next several weeks and months may see increased financial market and economic volatility in the Eurozone and across the globe.

From the perspective of the U.S. economy, the uncertainty surrounding the possibility of a Grexit may lead to:

- Slower global economic growth, which, at the margin, may hurt U.S. export growth

- A later liftoff for the Federal Reserve (Fed); and once hikes do begin, a shallower path for rates

- A stronger U.S. dollar for longer, as the ECB will likely speed up its quantitative easing (QE) program

- An increase in economic and market uncertainty in the U.S., which could, in turn, lead to modestly slower growth

The potential for a Grexit comes at a time when the Eurozone’s once-fractured financial transmission mechanism is on the mend, and as the Eurozone economy — aided by lowered expectations and a weaker currency — is accelerating and on track to add to global growth in 2015. Now, regardless of whether Greece stays or goes, the Eurozone’s recovery is threatened by lower consumer and business confidence in the Eurozone and a disruption in, but not the end of, the improvement in the Eurozone’s financial transmission mechanism, which has been healing for more than six months now. Although the financial system disruptions of a Grexit will likely be met by strong action from the ECB, the longer the uncertainty around Greece’s fate lasts, the greater the potential impact on the European and global economies. The net result could be a lower growth path for Eurozone and the globe. The Federal Open Market Committee (FOMC) and Fed Chair Yellen — who is slated to deliver a speech on Friday, July 10, 2015 — will be watching Greece closely. For now, our view remains that the Fed is on track to hike rates for the first time in this cycle in late 2015; but the longer the uncertainty around Greece lingers, the greater the odds that the Fed doesn’t hike rates until early 2016. The next FOMC meeting is July 28 – 29, 2015.

WATCHING WAGE INFLATION

If the situation in Greece can be resolved quickly, markets will return to the fundamentals driving the timing of the first Fed rate hike. With the U.S. labor market on track for another solid year of job growth, and therefore, well on its way to achieving the “full employment” side of the Fed’s dual mandate of full employment and low and stable inflation, the markets (and the FOMC) will watch inflation (and in particular, wage inflation) closely in the coming months. Indeed, the FOMC may face a dilemma later this year if wages (and overall inflation) accelerate even as the situation in Greece and the Eurozone deteriorates. More on that scenario in a future Weekly Economic Commentary.

The June 2015 Employment Situation report (released on Thursday, July 3, 2015) indicated that wage growth — as measured by the year-over-year-percent change in average hourly earnings — remained tepid, up just 2.0% from a year ago, still well below the 4%+ wage gains seen just prior to the 2007 – 09 Great Recession. Wage growth — or lack thereof — remains a concern for Fed policymakers as they continue to debate when they will begin raising rates in this cycle.

As we have written in previous Weekly Economic Commentaries, despite the tepid wage growth economy-wide, signs that wage pressures may be building in segments of the economy have begun to appear in recent months, most recently in the latest Fed Beige Book, released in early June 2015, ahead of the FOMC meeting on June 16 – 17, 2015. As it has over the past year, the June 2015 Beige Book noted that employers were having a difficult time finding qualified workers for certain skilled positions and some reported upward wage pressures for particular industries and occupations. In the past, these characterizations of labor markets have been a precursor to more prevalent economy-wide wage increases. The minutes of the June 16 – 17 FOMC meeting — due out Wednesday, July 8, 2015 — may shed more light on how concerned the Fed is with wages. However, we note that the minutes of the April 28 – 29, 2015, FOMC meeting revealed that Fed officials were not yet worried about rising wages, and indeed, cannot come to a general agreement that wages should even play a part in measuring inflation pressures in the economy.

In our view, a decisive upturn in wage inflation remains key to moving inflation and inflation expectations higher. As noted above, at just 2.0% year over year in June 2015, wages remain stubbornly weak [Figure 1], despite a private sector economy that has created nearly 13 million jobs since early 2010, pushing total employment well past its prior peak (in 2007) and the unemployment rate from 10.0% in late 2009 to 5.3% in June 2015. In the past, a drop in the unemployment rate of that magnitude over that time period has been accompanied by acceleration in wages.

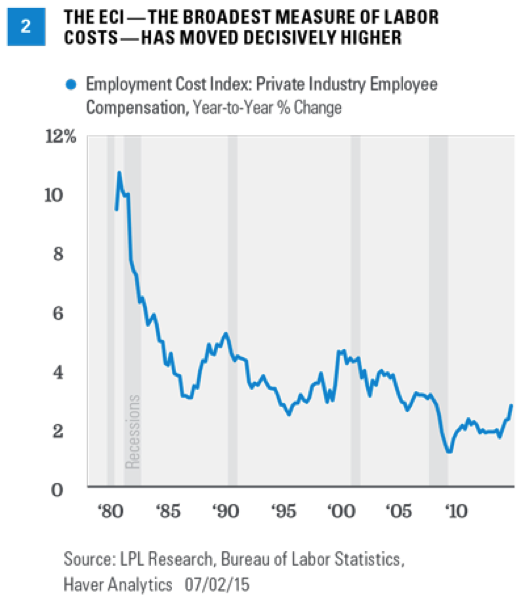

Average hourly earnings are not the only gauge of wage inflation the Fed is watching. The Employment Cost Index (ECI), the broadest measure of labor market compensation available, has been mentioned by Janet Yellen and other Fed officials in recent months. Although the ECI has clearly bottomed and is moving higher [Figure 2], it does not necessarily mean the Fed is poised to raise rates. Looking back over time, we’ve found that each Fed rate hike cycle is unique (economic and policy backdrop, labor market, inflation, external conditions, etc.), making it difficult to draw a specific conclusion such as: “The Fed always begins to hike rates when economic data point x crosses level y.” Instead, we can only draw very broad conclusions about when the Fed begins to hike rates. Looking at wages and ECI [Figures 1 and 2], the Fed generally does not begin to hike rates until after a definitive bottom in measures of wages has been made, although there are some exceptions to this. Currently, while average hourly earnings have not yet put in a definitive bottom, the ECI looks to have bottomed out. The ECI for Q2 2015 is due out in late July 2015.

On balance, the market and economic disruption ahead of a potential Greek exit from the Eurozone may modestly slow economic growth in the United States, further slow progress in the Eurozone economy, and could push the first Fed rate hike into early 2016. But ultimately, the Fed will make the decision on when — and by how much — to raise rates, based on the U.S. economy’s progress toward the Fed’s dual mandate.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Derivatives involve additional risks, including interest rate risk, credit risk, the risk of improper valuation, and the risk of non-correlation to the relevant instruments they are designed to hedge or to closely track.

DEFINTIONS

Quantitative easing (QE) refers to a central bank’s current and/or past programs whereby the bank purchases a set amount of Treasury and/or mortgage-backed securities each month from private banks. This inserts more money in the economy (known as easing), which is intended to encourage economic growth.

The monthly jobs report (known as the Employment Situation report) is a set of labor market indicators based on two separate surveys distributed in one monthly report by the U.S. Bureau of Labor Statistics (BLS). The report includes the unemployment rate, non-farm payroll employment, the average number of hours per week worked in the non-farm sector, and the average basic hourly rate for major industries.

The Bureau of Labor Statistics’ (BLS) Employment Cost Index (ECI) is a quarterly release that gives information on the costs of labor for businesses in the United States.

The Beige Book is a commonly used name for the Fed report called the Summary of Commentary on Current Economic Conditions by Federal Reserve District. It is published just before the FOMC meeting on interest rates and is used to inform the members on changes in the economy since the last meeting.