GTAA Delivers Solid Returns at Lower Risk. Period.

We recently came across a couple of articles making the sensational claim that TAA is nothing more than a repackaged and dressed-up version of market timing. Both articles – and others, we’ve subsequently learned – point to a Morningstar study showing that TAA has underperformed the Vanguard U.S. 60/40 balanced fund over the past few years. We have several problems with the original study and the referencing posts, but it all boils down to these points of difference:

- TAA is still widely misunderstood by many investors and advisors;

- TAA does not require discretionary market calls, and is best implemented by harnessing timeless and pervasive market factors like value and momentum;

- It is silly to benchmark most TAA strategies against a domestically focused stock/bond benchmark, such as a balanced fund.

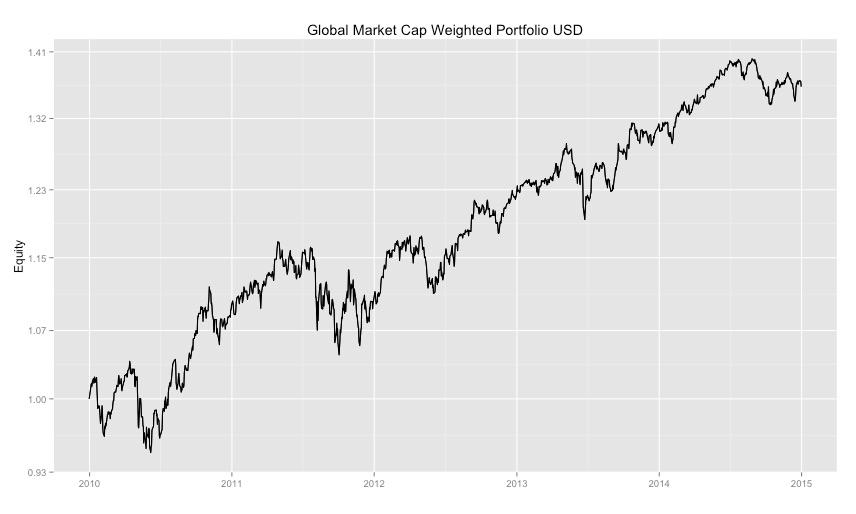

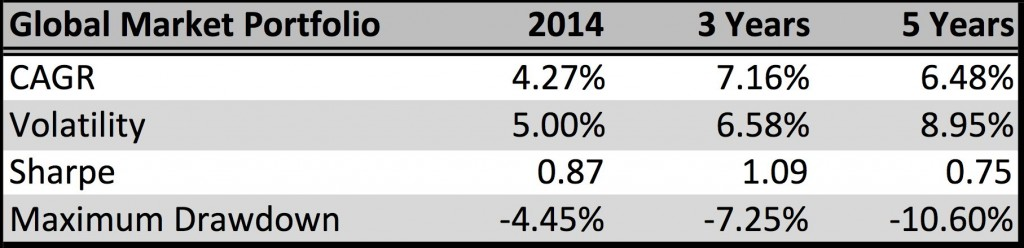

At the end of the day, however, we understand every aspect of this discussion circles back to one simple concept: performance. When we left off in Part 3 we had established that the most appropriate benchmark for GTAA strategies was the Global Market Portfolio (GMP). To recap, this is because it is passive, it is investible and it reflects the investing opportunity set of the manager. In other words, it is the aggregate portfolio of all global investment managers. Here is what the benchmark has done since 2010:

Figure 1. Performance of the Global Market Portfolio

Source: CSI Data

Now that we have specified the most appropriate benchmark, we can get down to the business of evaluating how well GTAA strategies have performed. How should we judge success? We submit that for GTAA strategies in particular we should judge results on both an absolute and a relative basis. When judging absolute results, it is our core belief that there is no way to properly evaluate performance without observing both rewards and risk. It’s like describing all the features of a product without any discussion of the cost.

- Do I want a private jet so that I can travel whenever and wherever I want without the hassle of airport lineups? Sure. Do I want it for $6 million plus $250k per year in maintenance costs? No.

- Do I want to invest in a strategy that might make 10% per year? Sure. Do I still want it if the strategy experiences a drawdown of 40% or more about one year in 5? Probably not.

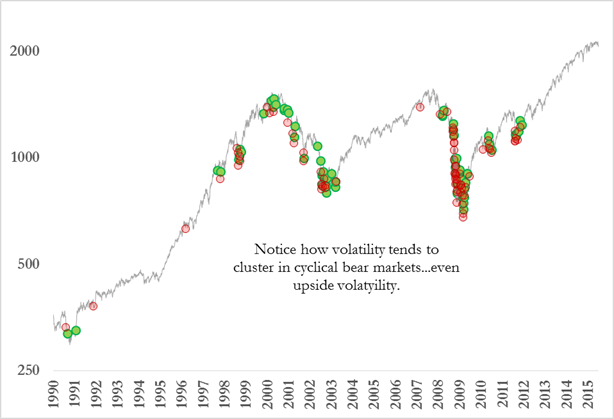

While many managers would debate our preferences, we first look to a strategy’s Sharpe ratio when evaluating GTAA approaches. Many thoughtful consultants and advisors object to the Sharpe ratio because they assert that investors are unconcerned with upside volatility, and focus exclusively on downside risk. While it’s true that the Sharpe ratio does not differentiate between upside and downside volatility, it is important to note that volatility clusters in markets. In other words, the largest down days are often adjacent in time to the largest up days. One needs to only look back to 2008/9 as proof of this. The chart below highlights all the days the S&P 500 either lost or gained more than 3% in a single day since 1990. It is interesting to note that over the last 25 years, the upside volatility tended to cluster during cyclical bear markets. This might come as a surprise to many investors, and as such, we perceive the symmetrical character of volatility as a better way to capture the true risk of a strategy than, say downside deviation.

Figure 2: Volatility Clustering (3% Gain/Loss Days in S&P 500 Since 1990)

Source: Morningstar, CSI Data

That said, we are also interested in non-parametric measures or risk such as drawdown and ulcer index, as these capture the true risk of a strategy when markets become non-normal, as they often do during crises, and the linearity of the return experience.

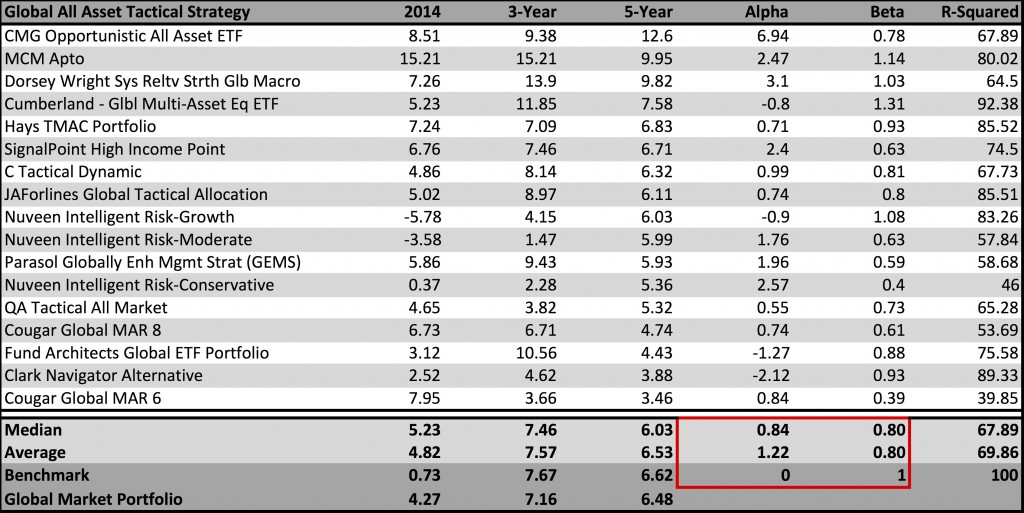

Unfortunately, the Morningstar report we’ve so often referred to does not provide absolute risk information, so on an absolute basis we can only observe the benefits (returns) of the strategies, not the costs (risk). However, we can evaluate the relative performance of GTAA strategies by comparing them to our two benchmarks. Morningstar has also blessed us with relative risk-adjusted metrics, so that we can judge the relative merits of a strategy vis-a-vis the benchmark in terms of both relative benefits (alpha) and costs (beta). We extracted the results of the Global All Assets – Tactical strategies with at least 5 year track records in Figure 3:

Figure 3. GTAA performance vs. appropriate benchmarks

Source: Morningstar, CSI Data

A comparison of just the annualized returns for the GTAA strategies relative to the benchmarks shows that they track each other very closely at each horizon, though the average GTAA strategy tracks the GMP more closely than the Morningstar benchmark, especially in 2014. In fact, this is a sign that the benchmarks are well specified. It is also, perhaps, to be expected; the GMP is, after all, the average of all active asset class bets!

On average, the GTAA strategies soundly beat Morningstar’s improper benchmark and even edged out the GMP over the 2014 calendar year, and were even with benchmarks over 3 and 5 year periods. It is interesting to note that while the average GTAA annualized returns appear to track closely to benchmark annualized returns, the Morningstar benchmark explains less than 70% of GTAA returns, as measured by average R-Squared values. We can therefore conclude that, while the benchmark is relatively well specified, GTAA strategies are harvesting returns from sources other than passive global beta exposures.

In other words, their active bets appear to be paying off.

And the story is more interesting once we observe the risk-adjusted characteristics. Note that the GTAA strategies tracked or exceeded their benchmark with less risk, as GTAA betas averaged just 0.8 over the past 5 years. Since GTAA strategies provided similar returns with less systematic risk, they delivered alpha of about 1% per year above their passive, globally diversified benchmark.

The fact is, the past 5 years have been an extraordinary period for global markets, characterized by a massive recovery in global risky assets coincident with a huge compression in global volatility. Many markets have experienced record consecutive periods without the meaningful corrections we typically observe, even during bull market cycles. As a result, GTAA strategies, which are typically constructed to really shine during crises, have yet to see their day in the sun. In fact, I’m mildly surprised to see that GTAA strategies have competed so well during this bull market phase of the cycle.

Which brings us to the real kicker, here: We won’t get to see just how resilient these strategies are until they stand tall above the detritus of the next bear market.